Small-Cap Pendulum

Small-Cap Pendulum

As we transition to darker nights and colder temperatures, a more subtle shift has been unfolding in recent years, rewriting a historic investment theory. The debate between value and growth investing is perennial, but it takes on a distinct flavour when focused on small-cap companies - those with smaller market capitalisations. This segment of the market is typically more volatile and sensitive to economic cycles, making the style choice challenging for investors. Small-cap stocks are generally defined as those that fall at the lower end of the market capitalisation range, but, being listed on stock exchanges, they are typically still reasonably sized businesses. Within this group, a company is categorised as either value or growth stocks.

Defining the Styles

Value stocks typically have a lower price-to-earnings (P/E) ratio, which is the current share price divided by the company's earnings. These are often established companies in mature industries or those temporarily out of favour.

Growth stocks tend to trade at a high price-to-earnings ratio, with investors expecting high rates of future earnings and revenue growth. These companies often operate in rapidly expanding or innovative industries.

The Historical Edge: Value's Long-Term Premium

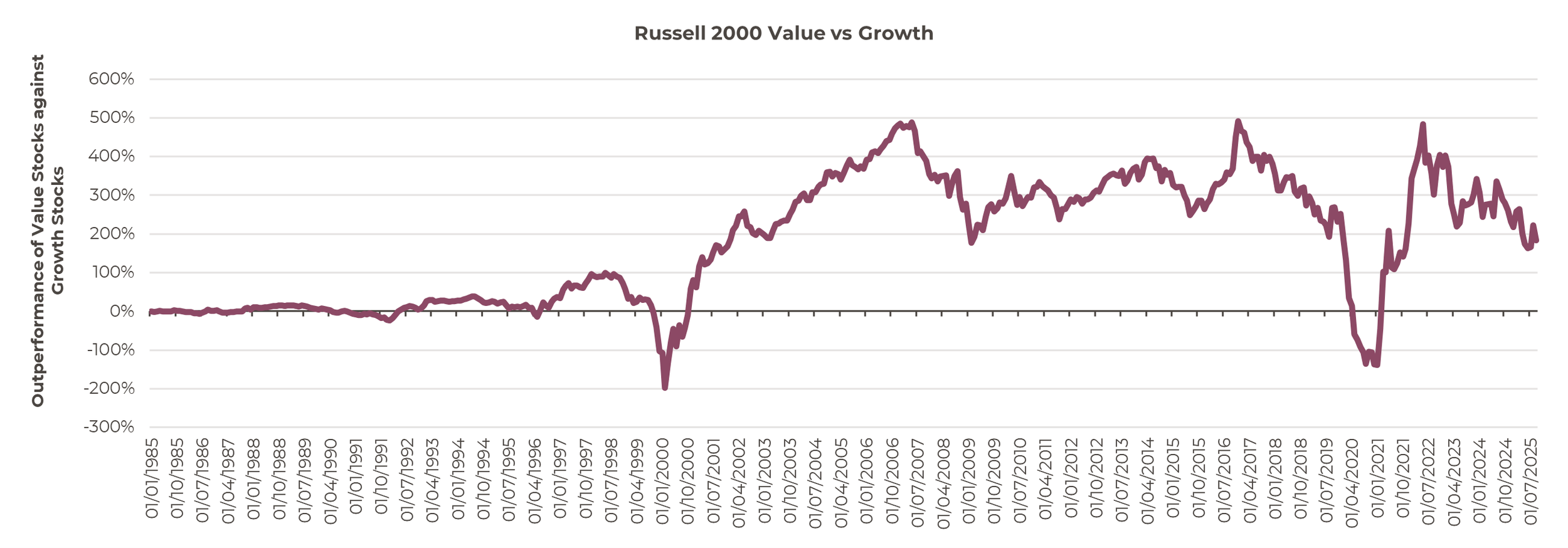

Historically, the performance data has favoured small-cap value over the long term in the US (as Europe is different), a phenomenon often referred to as the "value premium". While the long-term trend favours value, it is not constant. Outperformance tends be followed by relatively short, intense bursts of underperformance. For instance, the late 1990s saw massive growth outperformance (the 'tech bubble'), which was followed by a sustained period of strong value outperformance in the early 2000s. The driver of performance between value and growth appears highly variable.

Value outperformed growth until 2006 but since then has swung between the different styles

Source: Artorius, Bloomberg

A Prolonged Growth Run

In recent years, the value trend has largely been reversed with markets dominated by US growth stocks, especially those in the mega-cap technology space. This trend has heavily influenced small-cap performance as well.

Combined with prolonged low interest rates in the pre-Covid-19 era, small-cap growth was favoured by investors resulting in a premium in price to earnings compared to small-cap value stocks.

In today's environment, small caps in general have faced headwinds. Smaller firms tend to carry higher levels of debt relative to their earnings. In a period of high interest rates, this sensitivity to the cost of capital can put significant pressure on their profitability. However, other than a brief rally following a return to normal life after Covid-19, the trend to favour growth stocks has continued.

In the last decade, bar a short rally around Covid-19, growth has significantly outperformed value

Source: Artorius, Bloomberg

The last decade of growth stock dominance, driven by low rates and technology fascination, has pushed small-cap growth valuations to high levels. However, it remains to be seen if this trajectory continues, or if markets will revert to the long-term trend, allowing value stocks to once again return to favour in the future.

Flying Blind

Despite the ongoing US shutdown and the resulting lack of official economic data, the Federal Reserve delivered an expected 0.25 percentage point rate cut this week. However, market hopes for a further cut in December were clouded after Fed Chair Jerome Powell stated, "What do you do if you're driving in the fog? You slow down," and told reporters that "there were strongly differing views about how to proceed" among members of the Fed's committee. He added that the decision will ultimately depend on incoming economic data, which "We're going to collect every scrap of data we can find." Odds of a cut in December are now hovering just above 50%, having been in the low 90s earlier in the week.

Earnings in Full Swing

Investors are in the midst of digesting the quarterly updates. With the US equity market dominated by the big seven technology giants, this week has been on watch as five of the seven have provided their update.

Alphabet reported record revenue and Amazon reported strong Q3 earnings, both seeing large share price jumps. Apple projected strong sales over the coming holiday period, which aided its share price. Meta, on the other hand, despite reporting record revenues, missed analysts' targets and consequently saw its share price drop. Microsoft also saw strong results, but rising AI spending weighed on investor sentiment.

With Nvidia's earnings a few weeks away, there is still plenty of news expected from this earnings period.

Josh Young de Ferrer

Portfolio Manager

*Any feedback provided can be anonymous

Important Information

All expressions of opinion reflect the judgment of Artorius at 31st October 2025 and are subject to change, without notice. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete; we do not accept any liability for any errors or omissions, nor for any actions taken based on its content. The value of an investment and the income from it could go down as well as up. The return at the end of the investment period is not guaranteed and you may get back less than you originally invested. Past performance is not a reliable indicator of future results. Nothing in this document is intended to be, or should be construed as, regulated advice. Artorius provides this document in good faith and for information purposes only. Reliance should not be placed on the information contained within this document when taking individual investments or strategic decisions.

Artorius Wealth Management Limited is authorised and regulated by the Financial Conduct Authority. Artorius is a trading name of Artorius Wealth Management Limited.

FP20251031001