Uncertainty headwinds continue

Uncertainty headwinds continue

The global economic environment continues to be engulfed by uncertainty. President Donald Trump’s aggressive tariff position and policy updates, both scheduled and unscheduled, have resulted in high levels of financial market volatility. Now that we are mid-way through the Q1 2025 US company reporting season, what is notable is how the market uncertainty is now being reflected in reductions in future profit expectations. This is not hugely surprising given the likely adverse impact that tariffs wars will have. The textbook expectation is resulting stagflation. The International Monetary Fund (IMF) has taken a similar view this week when it issued its global economic forecasts, showing reductions to its global growth estimates.

News flow driving market volatility

The equity and bond markets have been highly reactive to news flow from all sources in recent weeks. This has not been limited to the news flow on tariffs, but also in relation to the White House’s position on other factors, such as the position of Federal Reserve Chair Jerome Powell. The National Economic Council Director Kevin Hassett announced last week that the Government was assessing whether it was possible to remove Powell. This came after the President’s public comments and social media posts criticising the Federal Reserve. This was because, in the view of Trump, the Fed hasn’t cut interest rates which would be viewed as supportive of equity markets. Trump’s position was then seemingly reversed when he answered a reporter’s question by saying he had no intention of firing Powell, bringing some market relief.

The US’s position on tariffs still remains highly uncertain. No significant deals with any country have been announced yet and all eyes are on China. US tariffs on China currently stand at 145%, which would significantly increase prices on Chinese imports in the US and therefore impact demand and margins. China has reciprocated and seems to be positioning itself for a long trade war. There was some market relief in recent days, however, when US Treasury Secretary Scott Bessent seemed to soften the US position by saying there was the opportunity for a “big deal” between the US and China. This was maybe as a result of reports that companies such as Target and Walmart (US retail giants) were highlighting the risks of empty shelves within weeks to the White House.

Earnings expectations reduced

As we move through the Q1 earnings season we note the caution in the outlook statements from the reporting companies. For example, both JP Morgan Chairman & CEO, Jamie Dimon, and Citi CEO, Jane Fraser, reference that their respective businesses are prepared for a wide range of scenarios going forward.

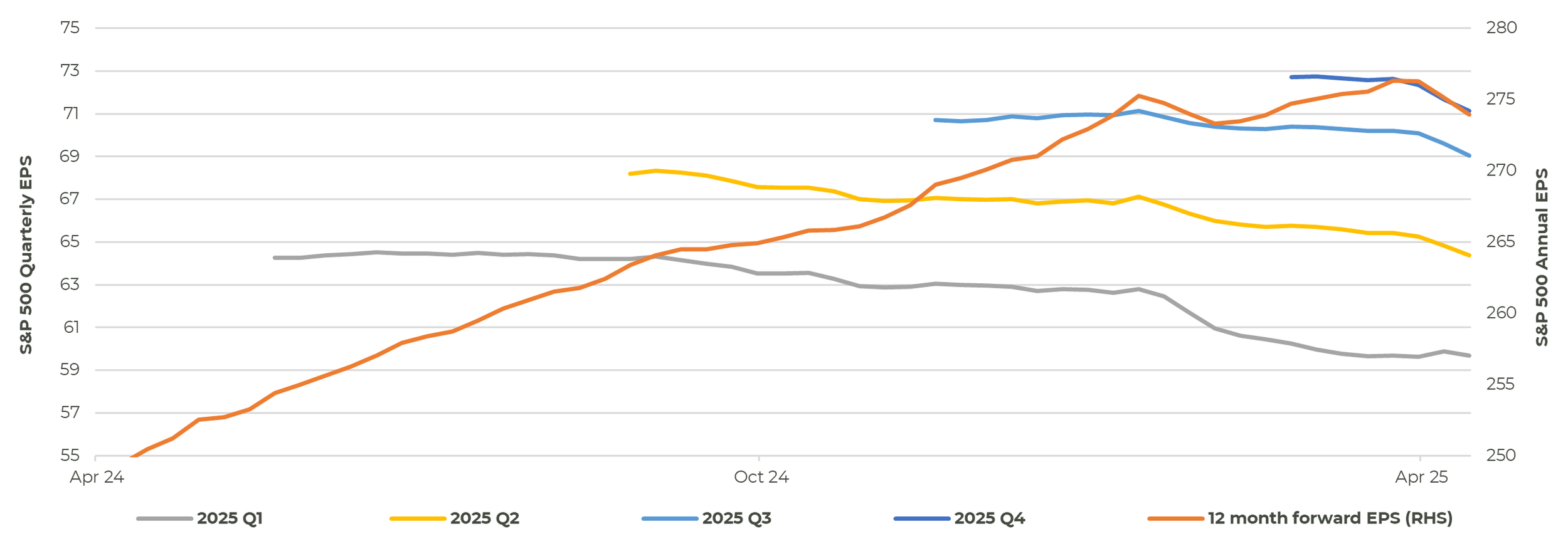

This level of caution now appears to be showing in analyst forecasts collated by Bloomberg. Notably, they are now being downgraded. We expect downgrades to continue in the short term as more companies err on the side of caution in uncertain times and guide towards lower expectations.

Whether the downgraded forecasts become reality is dependent on many factors, but the tariff situation is the key driver at this point, and it can change at any moment. What is likely though is that businesses become defensive in the short term, so reducing capital investment, pausing hiring plans and tightening budgets generally. All of which can have a dampening effect on economic growth.

S&P 500 Quarterly and Annual Earning Per Share (EPS) forecast (RHS = Right Hand Side)

Source: Artorius, Bloomberg

IMF downgrades global growth due to tariffs

The IMF is an institution that looks to promote financial stability and monetary cooperation and regularly issues publications, including its global growth expectations. Its most recent release this week downgraded its global growth forecast from just 3 months ago from 3.3% to 2.8%. In its words “due to effective tariff rates at levels not seen in a century and a highly unpredictable environment”. Of note, the largest reduction in expected growth within developed counties is for the US, which is now expected to see Gross Domestic Product (GDP) grow by 1.8% in 2025, down from 2.7%. Clearly, these are just forecasts and may not become reality, but we believe directionally the logic makes sense as tariffs are not generally positive for economic growth. The IMF report can be accessed via this link: World Economic Outlook, April 2025: A Critical Juncture amid Policy Shifts.

The dollar has weakened but so has the Yuan

As highlighted in our recent Outlook note, the Dollar has weakened by circa 10% against most major currencies since early January. This increases the US’s competitiveness as an exporter which might be the aim for President Trump. However, looking at the US Dollar versus the Chinese Yuan, the Dollar has strengthened since 9th April when the 145% tariff rate came into effect. Therefore, the competitiveness of the US versus China, who it would perceive as a major competitor, has reduced.

US Dollar versus Chinese Yuan Exchange rate

Source: Artorius, Bloomberg

There will be a cost even with a 180 degree about turn on tariffs

The potential impact of tariffs, trade conflicts, and geopolitical tensions now appears to be coming through in the market’s future profit expectations with downgrades being implemented. As it stands, these may be prudent cuts given the expectation of stagflation in the US and potential for a recession. Unlike, the 2008 Financial Crisis or the COVID pandemic, it is within Trump’s power to completely reverse his tariff position and there have been some signs of potential concessions. The issue for markets is that it is hard to see how Trump can show himself as victorious in his deal making without some element of tariff implementation. Furthermore, given the uncertainty for business and the time it takes for goods to move through global supply chains, even a complete U-turn would still result in lost trade in the period since the initial tariff announcement. For the time being patience is required along with the hope that the uncertainty cloud lifts sooner rather than later.

Phill Carroll

Head of Alternatives

*Any feedback provided can be anonymous

Important Information

All expressions of opinion reflect the judgment of Artorius at 25th April 2025 and are subject to change, without notice. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete; we do not accept any liability for any errors or omissions, nor for any actions taken based on its content. The value of an investment and the income from it could go down as well as up. The return at the end of the investment period is not guaranteed and you may get back less than you originally invested. Past performance is not a reliable indicator of future results. Nothing in this document is intended to be, or should be construed as, regulated advice. Artorius provides this document in good faith and for information purposes only. Reliance should not be placed on the information contained within this document when taking individual investments or strategic decisions.

Artorius Wealth Management Limited is authorised and regulated by the Financial Conduct Authority. Artorius is a trading name of Artorius Wealth Management Limited.

FP20250425001