Amara’s Law and the AI Reality Check

Amara’s Law and the AI Reality Check

The surge in AI-related stocks over the past few years has captured headlines and imagination alike. From record valuations to breakthroughs in large language models, investor enthusiasm has drawn comparisons with some of history’s most notable bubbles. Past examples include the South Sea Company in the early 1700s, the 1920s US stock market boom, and Japan’s 1980 real estate surge, when Tokyo’s Imperial Palace briefly held a higher valuation than all property in California. Technology-driven cases were no less extreme; the 1840s railway expansion laid track far ahead of demand, and the 1990s telecom boom produced over 70 million miles of fibre that went unused. Even the 17th-century Dutch tulip craze saw bulbs traded for the modern equivalent of half a million dollars each. Today, the question is whether the rapid rise of AI stocks represents a bubble, a boom, or something in between.

Since ChatGPT launched in November 2022, large language models have been adopted at remarkable speed. More than one in ten people worldwide have used OpenAI’s chatbot, sending over 18 billion messages each week—a rate the internet did not reach until more than a decade after its launch. Yet for most, AI remains a subtle part of daily life, often serving as a search-engine replacement or a tool for simple text generation.

Roy Amara, a noted futurist and former president of the Institute for the Future, articulated what later became known as Amara’s Law:

“We tend to overestimate the effect of a technology in the short run and underestimate it in the long run.”

This principle captures a familiar pattern. In the short term, AI developments—including new models from DeepSeek, Google, and Alibaba—could reflect the short-term overestimation side of Amara’s Law. Early deployments are impressive but remain constrained by limitations such as accuracy, bias, running costs, and the fact that many AI startups are pre-revenue or running only pilot projects. Headlines highlight soaring valuations and capital expenditure, yet tangible integration into daily life is still emerging.

As we enter the fourth year of the AI rally, capital expenditure by the five largest hyperscalers - companies operating cloud computing and data centres - will exceed $400 billion this year and approach half a trillion dollars next year. This scale of investment resembles a playful arms race, with firms betting on early market share and future dominance, even amid uncertainty about near-term returns.

A scenario assessment of the capital allocation strategies pursued by the largest AI players helps explain the scale of investment. From a game-theory perspective, underinvesting in a potentially transformative technology could be existential; loss of competitive edge, disruption of core business, or obsolescence. The downside of overinvesting - overcapacity or temporarily depressed returns - is manageable, particularly for large tech firms with strong balance sheets. If the cycle mirrors past technology build-outs, periods of overcapacity or corrections could occur, even as long-term gains in productivity and economic value continue to materialise.

History shows that attention often peaks before structural change becomes evident. Blockchain, largely dismissed in 2022 after the crypto surge that included NFTs and meme coins, quietly matured into foundational infrastructure for payments, tokenised assets, and enterprise finance. The internet itself transformed commerce, media, and communication long after the dot-com crash. AI may be at the opposite point in the cycle today: investment and interest are high, while the full real-world impact is still unfolding.

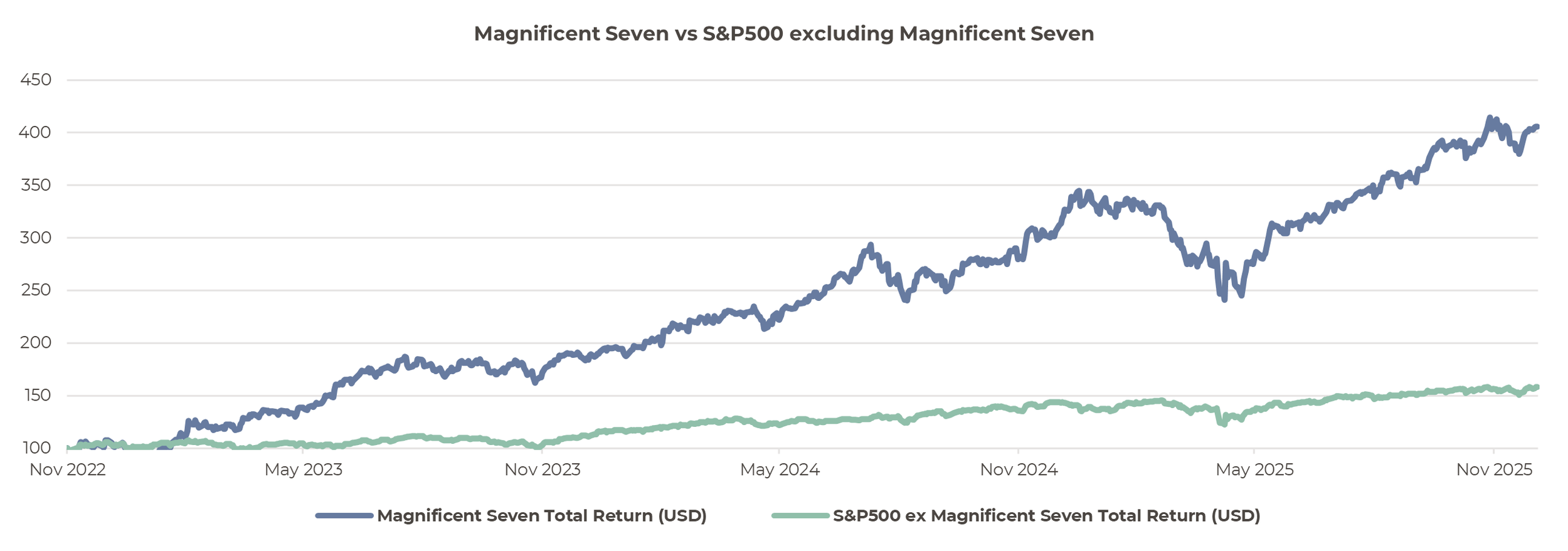

Today, investors cannot shy away from forming a view on the largest AI companies. The so-called 'Magnificent Seven'—some of the largest AI-exposed firms—now make up roughly 35% of the S&P 500, creating significant concentration risk for holders of the index. This concentration is largely a consequence of their strong market performance; since the launch of ChatGPT in November 2022, total returns (in USD) for the Magnificent Seven have exceeded 400%, compared with just over 150% for the S&P 500 excluding these companies.

Source: Artorius, Bloomberg

Amara’s Law provides a perspective on the timing and scale of technological change. Short-term effects can be overestimated, long-term impact underestimated, and timing is unpredictable. Watching adoption, tracking meaningful metrics like token usage and corporate deployments, and recognising the scale of global experimentation helps maintain perspective amid the noise. The full impact of transformative technologies emerges gradually, rather than all at once.

In short, AI in 2025 is likely overestimated in the immediate term. Early deployments are impressive but limited, and many startups are pre-revenue or only running pilot projects. Nevertheless, it could be a mistake to dismiss AI’s long-term potential. Its broader influence is probably still underestimated, much like the internet after the dot-com crash. Innovations in machine learning—from natural language processing to autonomous systems—are expected to spread gradually across industries, reshaping workflows, productivity, and decision-making. The most significant gains will likely appear over years rather than months, reinforcing the patience needed to understand AI’s true impact.

Yuval Peshchanitsky

Portfolio Analyst

*Any feedback provided can be anonymous

Important Information

All expressions of opinion reflect the judgment of Artorius at 5th December 2025 and are subject to change, without notice. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete; we do not accept any liability for any errors or omissions, nor for any actions taken based on its content. The value of an investment and the income from it could go down as well as up. The return at the end of the investment period is not guaranteed and you may get back less than you originally invested. Past performance is not a reliable indicator of future results. Nothing in this document is intended to be, or should be construed as, regulated advice. Artorius provides this document in good faith and for information purposes only. Reliance should not be placed on the information contained within this document when taking individual investments or strategic decisions.

Artorius Wealth Management Limited is authorised and regulated by the Financial Conduct Authority. Artorius is a trading name of Artorius Wealth Management Limited.

FP20251205001