The house of AI

The house of AI

Summary

Given the tendency for commentators to highlight the risks in the current environment, be that oil prices, interest rates or valuations, it can be hard to hear good news above the prevailing negativity. Corporate profits are growing robustly around the world, while economies are generally performing better than expected, especially given the oil-price shock that followed the US and Israeli attacks in February 2026.

The resumption of hostilities has pushed up oil prices. This could lead to a rekindling of inflationary pressures and may result in higher interest rates in the US (and elsewhere). There is a notable disconnect between strong US economic data and subdued consumer confidence. This is likely the result of inflation starting to outstrip wage inflation, causing real wages to fall, and an ongoing recession in the US housing market.

Strong economic growth in the US is predicated on a surge in spending by the technology giants seeking to build their artificial intelligence (AI) capabilities. This AI spending is also driving corporate profitability, particularly in the US and Asia. Profits have risen faster than equity prices through 2026, resulting in markets that look cheaper (lower valuations) than they did at the start of the year despite rising in price.

The combination of rising equity prices and declining valuations is encouraging, but it also suggests that investors remain sceptical about the sustainability of the AI investment cycle. That scepticism may prove justified. However, as companies publish their quarterly results over the coming weeks, we should gain greater clarity on both the outlook for profits and their future investment intentions.

Back to war?

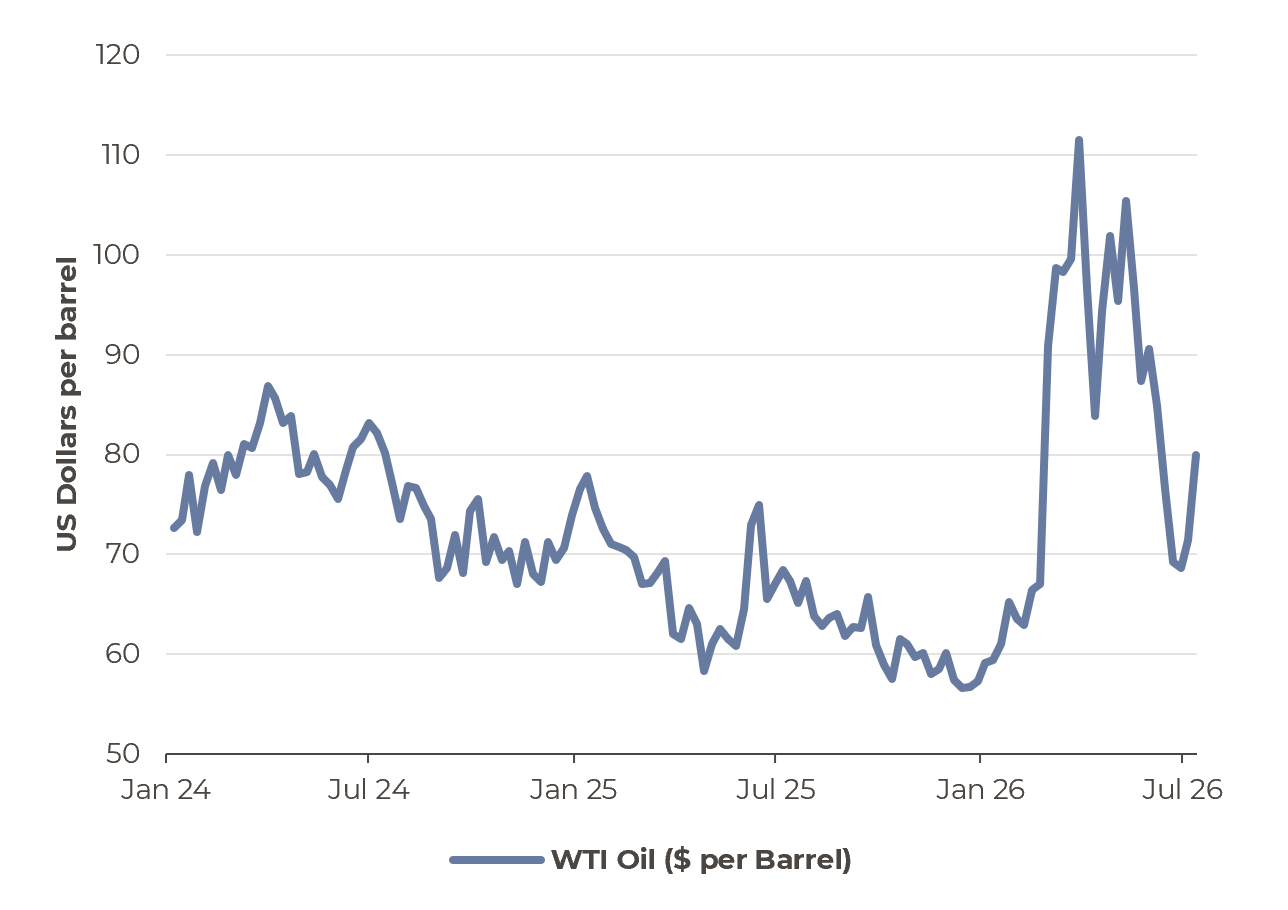

The escalation in military activity in the Gulf has rekindled concerns about the oil market. The latest flare-up follows a period of what might be described as a “Schrödinger’s ceasefire”: an unstable state in which US–Iran hostilities appeared both active and suspended, while continuing diplomatic negotiations offer the possibility of a genuine and lasting resolution.

The fragility of the ceasefire has been plain to see, but the current military action is limited in comparison to the March action. However, the Strait of Hormuz, through which over 20% of global oil and natural gas are shipped, appears to be closed to shipping, resulting in higher oil prices over recent days.

Equity and bond markets appear to be pricing minimal impact from the latest hostilities. However, just as the global economy appeared poised to enjoy a period of relative calm, renewed tensions in the Gulf threaten to disrupt an otherwise benign backdrop.

The West Texas Intermediate (WTI) oil price fell as conflict de-escalated but has risen in mid-July on the resumption of hostilities in the Gulf

Source: Bloomberg, Artorius

Good news

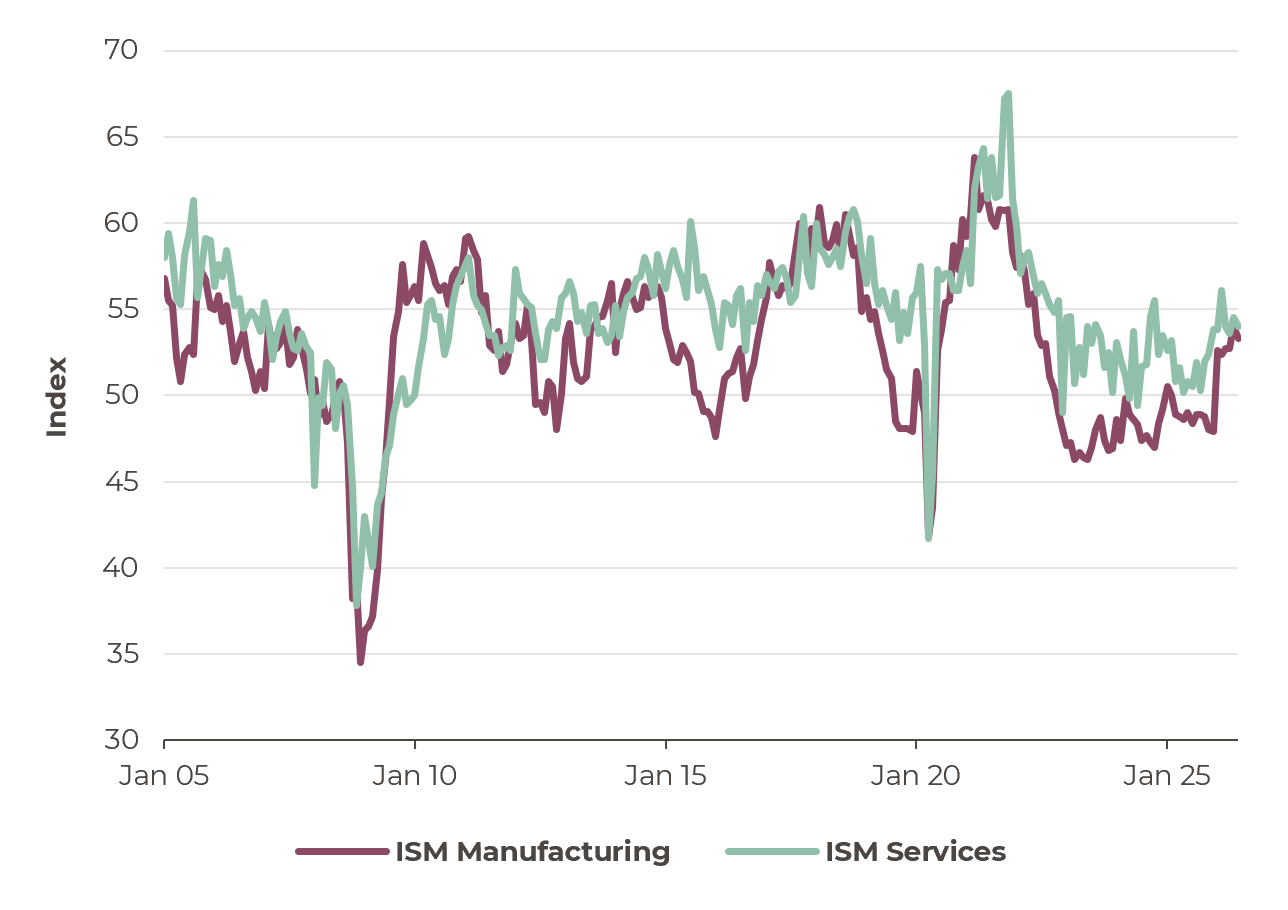

Global economic growth continues to exceed expectations, despite the oil-price shock resulting from the Gulf conflict. US economic data shows that manufacturing and services activity is resilient and picking up, as shown in the recent survey from the Institute for Supply Management (ISM). This may partly reflect the interest rate cuts delivered in 2024 and 2025, but recent growth is largely dependent on the surge in technology investment by US companies. This investment boom has accelerated significantly over the past six months.

US technology investment as a share of Gross Domestic Product (GDP) has now surpassed the peaks reached during the 1990s. Spending plans announced by the largest technology companies for 2026 are nearly 50% higher than they were roughly six months ago. This pace of growth is staggering. One potential concern, however, is that these companies are increasingly turning to the capital markets, through both equity and debt issuance, to finance their investment. Until recently, much of this expenditure had been funded internally from cash flow.

However, beneath the strong headline growth figures, significant areas of the US economy remain weak. The US housing market remains becalmed and, together with a lack of strong employment growth, may explain exceptionally low consumer confidence reported in surveys. Although equity markets are close to all-time highs, the benefits of stronger economic growth are not yet being widely felt on Main Street.

Both US manufacturing and services activity are on the rise

Source: Bloomberg, Artorius

One reason for the prevailing gloom among US consumers is that inflation remains elevated. The spike in oil prices in March pushed US inflation above 4%. With wages growing at a slower pace, workers are experiencing a renewed squeeze on real incomes and purchasing power. The Federal Reserve cited persistent inflationary pressures as one reason for leaving interest rates unchanged at its latest meeting. Indeed, bond markets are now pricing in the possibility of rate increases over the coming months, reflecting the combination of resilient economic growth and inflation remaining above the 2% target.

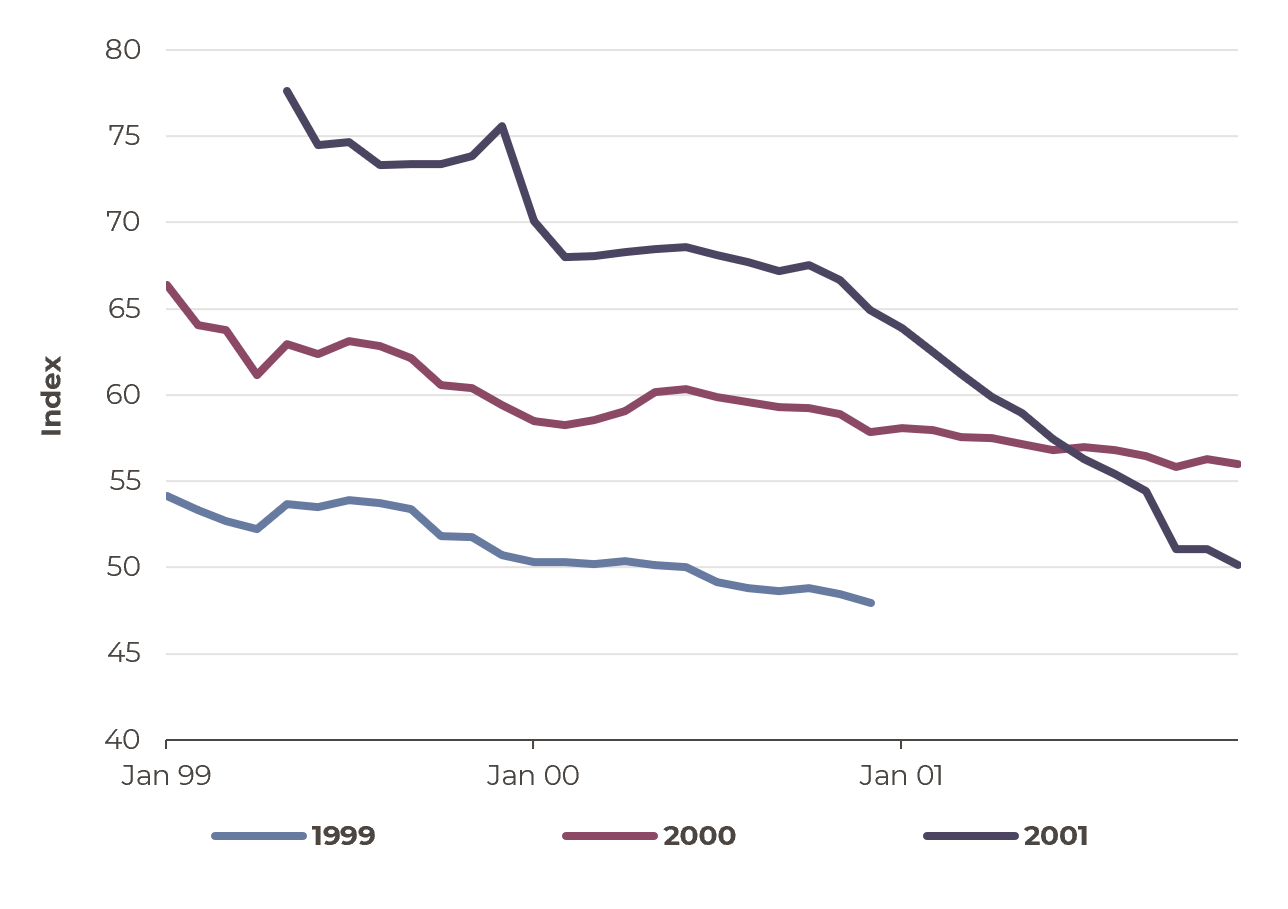

Equity markets could become more volatile if policymakers choose to raise US interest rates aggressively. In our view, the future path of interest rates will be a key influence on investor sentiment and market outcomes. The experience of 1999-2000 offers a cautionary parallel, during which rising interest rates, elevated valuations and downward revisions to profit expectations combined to bring the technology bubble to an end.

The good news is that June’s US inflation data was better (lower) than expected, which may alleviate the need for interest rates to increase in the near term. However, under the new Federal Reserve Chair, Kevin Warsh, the policy agenda appears likely to place greater emphasis on returning inflation towards the 2% target than was the case under Jerome Powell.

Profits boom

The robust economic backdrop continues to support corporate earnings, which have generally exceeded expectations. Profits are a key driver of investment returns and, in the face of uncertainty resulting from the Gulf conflict, the strong earnings backdrop has insulated equity markets from the invidious impact of oil price volatility and the prospect of higher interest rates.

For now, earnings have been growing so strongly that it’s hard to call this a bubble. Bubbles are about excessive valuations and a lack of earnings growth, as was the case in 1999-2000. During the technology bubble of 1999-2000, equity markets continued to rise even though earnings expectations were being downgraded and interest rates increased. Today, by contrast, robust economic growth and rising corporate profits are reinforcing equity-market strength, creating a virtuous circle.

Nevertheless, an important question remains over the long-term returns generated by the substantial AI investment undertaken by the major technology companies. However, as businesses increasingly incorporate AI into their operations, evidence of improved productivity and profitability may help investors recognise the lasting value created by the current investment cycle.

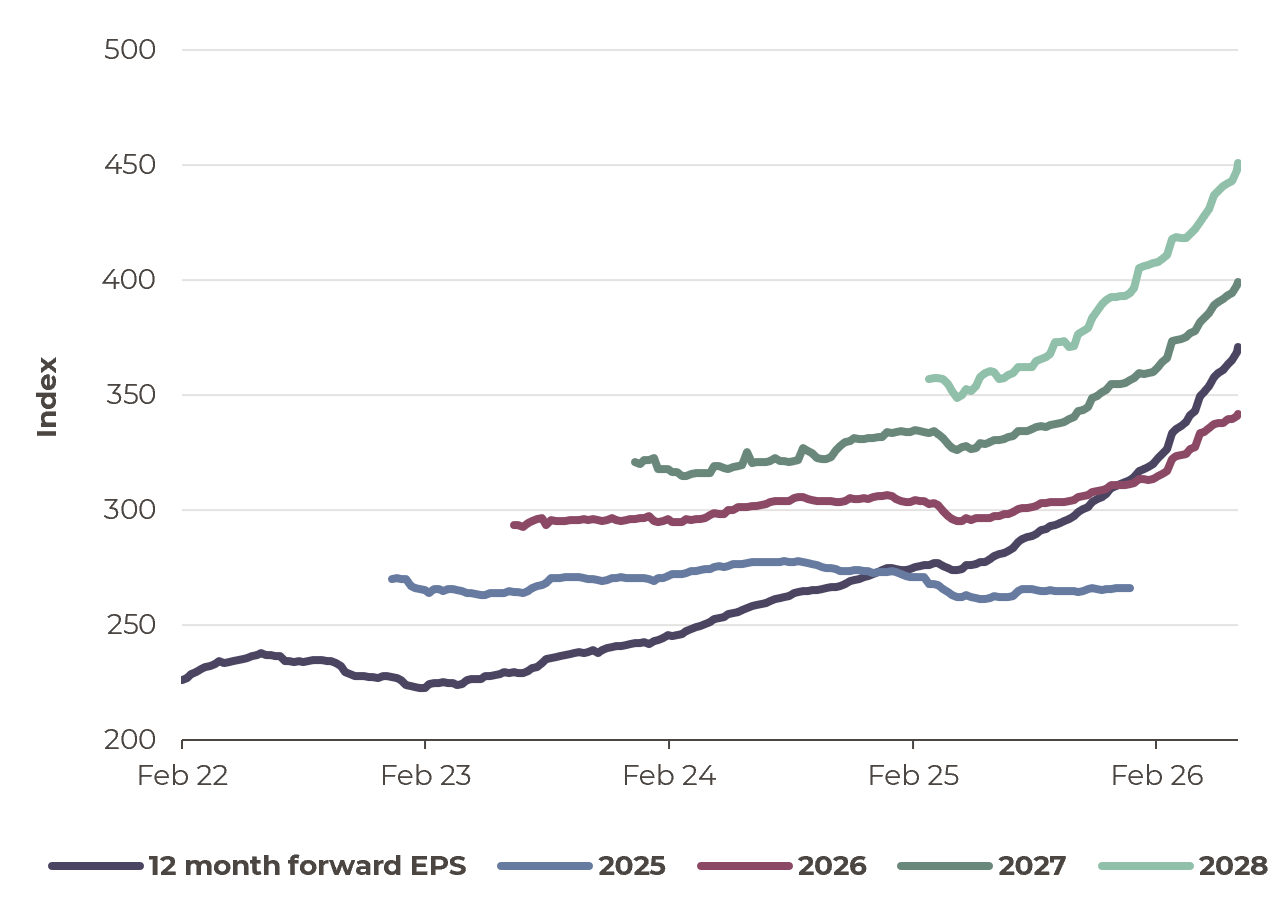

US (S&P 500) earnings estimates are rising sharply as measured by Earnings per Share (EPS)

Source: Bloomberg, Artorius

Back in 1999-2000 earnings starting falling even as stock markets were rising to their peak

Source: Bloomberg, Artorius

Spreading the good news

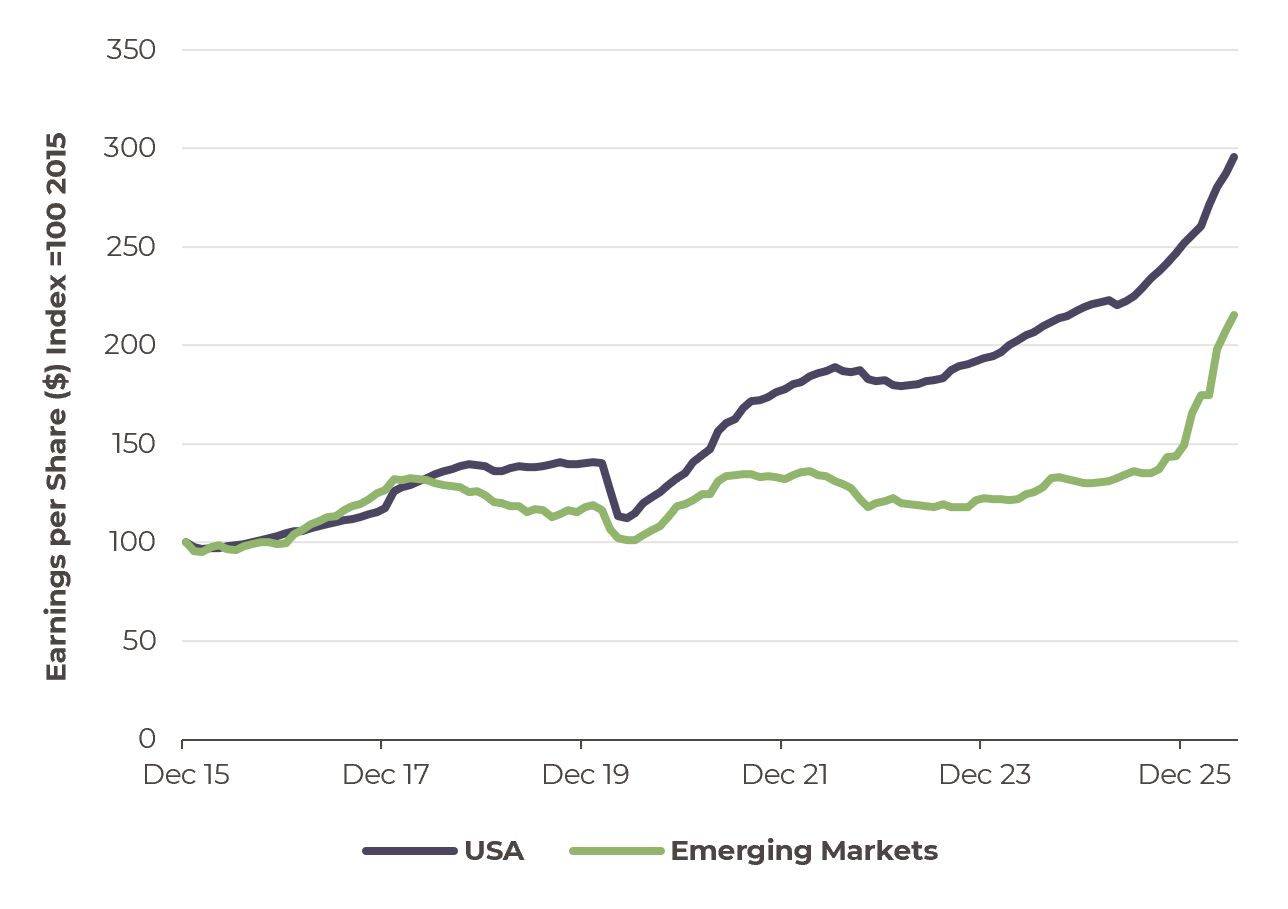

The benefits of the AI investment cycle are not confined to US companies. Earnings across emerging markets and Asia have also risen robustly over the past 12 months, driven overwhelmingly by strong profit growth in the technology sector, as shown in the chart to the right.

The scale of profits growth across many regions through 2026 has resulted in a surprising drop in valuations even though share prices have increased. The table below compares valuations at the end of 2025 with those at the end of June 2026, alongside market returns over the same period. As long as profits remain on an upward trend, then the current cheapening of markets suggests, in our view, that investors remain sceptical about the longevity of the AI investment cycle.

There are, however, two principal risks. First, interest rates could rise, as they did in 1999. This would increase the cost of capital and could cause companies to reassess their investment plans, particularly as more businesses have turned to external financing. Second, much of the recent growth in profitability has been fuelled by the technology giants’ substantial investment in AI. The ultimate returns on this spending have yet to be demonstrated. If these investments prove less profitable than anticipated, and so capital expenditure is subsequently curtailed, the outlook for earnings in the US, Asia and emerging markets could deteriorate rapidly.

US and Emerging Market Earnings per Share: 2025-26 has seen a sharp rise in profits in the US but an even steeper increase in emerging markets

Equity Regions: Year-to-date returns and valuation changes - the fall in valuations reflects that profits have increased by more than equity prices.

| Equity Region | UK | USA | Europe ex UK | Japan | Asia ex Japan | Emerging Markets |

| Total Return (2026 to End-June 2026) | 5.6% | 9.4% | 9.3% | 18.9% | 22.8% | 22.7% |

| 12 month forward PE | ||||||

| End-June 2026 | 12.7 | 20.6 | 16.4 | 17.4 | 12.3 | 11.3 |

| End-December 2025 | 13.6 | 22.1 | 16.1 | 17.2 | 14.6 | 13.2 |

Conclusion

The resumption of hostilities has pushed up oil prices. This could lead to a rekindling of inflationary pressures and may result in higher interest rates in the US (and elsewhere). There is a notable disconnect between strong US economic data and subdued consumer confidence. This is likely the result of inflation starting to outstrip wage inflation, causing real wages to fall, and an ongoing recession in the US housing market.

Strong economic growth in the US is predicated on a surge in spending by the technology giants seeking to build their artificial intelligence (AI) capabilities. This AI spending is also driving corporate profitability, particularly in the US and Asia. Profits have risen faster than equity prices through 2026, resulting in markets that look cheaper (lower valuations) than they did at the start of the year despite rising in price.

The combination of rising equity prices and declining valuations is encouraging, but it also suggests that investors remain sceptical about the sustainability of the AI investment cycle. That scepticism may prove justified. However, as companies publish their quarterly results over the coming weeks, we should gain greater clarity on both the outlook for profits and their future investment intentions.

*Any feedback provided can be anonymous

Important Information

Artorius provides this document in good faith and for information purposes only. All expressions of opinion reflect the judgment of Artorius at 17th July 2026 and are subject to change, without notice. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete; we do not accept any liability for any errors or omissions, nor for any actions taken based on its content.

The value of an investment and the income from it could go down as well as up. The return at the end of the investment period is not guaranteed and you may get back less than you originally invested. Past performance is not a reliable indicator of future results.

Nothing in this document is intended to be, or should be construed as, regulated advice. Reliance should not be placed on the information contained within this document when taking individual investment or strategic decisions.

Any advisory services we provide will be subject to a formal Engagement Letter signed by both parties. Any Investment Management services we provide will be subject to a formal Investment Management Agreement, which will include an agreed mandate.

Artorius Wealth Management Limited is authorised and regulated by the Financial Conduct Authority. Artorius is a trading name of Artorius Wealth Management Limited.

FP20260717001