Mind the flood

Mind the flood

Summary

With a Memorandum of Understanding (MoU) between Iran and the US scheduled for signing on 19 June, expectations are rising that the fragile ceasefire may transition into a more durable peace agreement. Oil prices have fallen in expectation that the Strait of Hormuz will be unblocked and global energy supply will return to some sense of normality. Lower oil prices should alleviate inflationary pressures, although the March price spike will continue to feed through into inflation data in the near term.

The new Chair of the Federal Reserve, Kevin Warsh, has signalled a potential shift in the policy framework. However, he may not be able to change the interest rate, as the policymaking committee is currently divided between those seeking to cut rates and those willing to keep rates on hold (or even raise them).

The US economy has been resilient even in the face of higher oil prices, with growth largely supported by investment in Artificial Intelligence (AI). Until recently funding for AI spending has come from Private Equity investing into private companies such as Anthropic and OpenAI, while publicly listed companies have funded their investment spending through free cash flow and borrowing but this is changing as the scale of investment increases.

Recent weeks have seen the Initial Public Offering (IPO) of SpaceX, which raised $75 billion, with further listings from Anthropic and OpenAI anticipated. At the same time, listed companies (Meta, Alphabet, Oracle) are increasingly raising equity capital. This marks a notable shift from the past decade, during which US corporates have been net buyers of equity via share buybacks, supporting equity returns.

If inflation pressures ease as oil prices fall, interest rates remain low and earnings remain robust, investors may be willing to provide new capital to companies at current levels.

A flood of oil

The previously unstable state of ceasefire interspersed with conflict appears to be evolving into a more credible cessation of hostilities.

On 14 June, the US, Iran, and mediator Pakistan indicated that a formal agreement may be signed on 19 June in Geneva. While the full terms remain undisclosed, it is understood that a 60-day extension to the ceasefire is under consideration. Uncertainty around the original war rationale, combined with a lack of clarity or consistency about its objectives, makes a lasting peace deal a challenge.

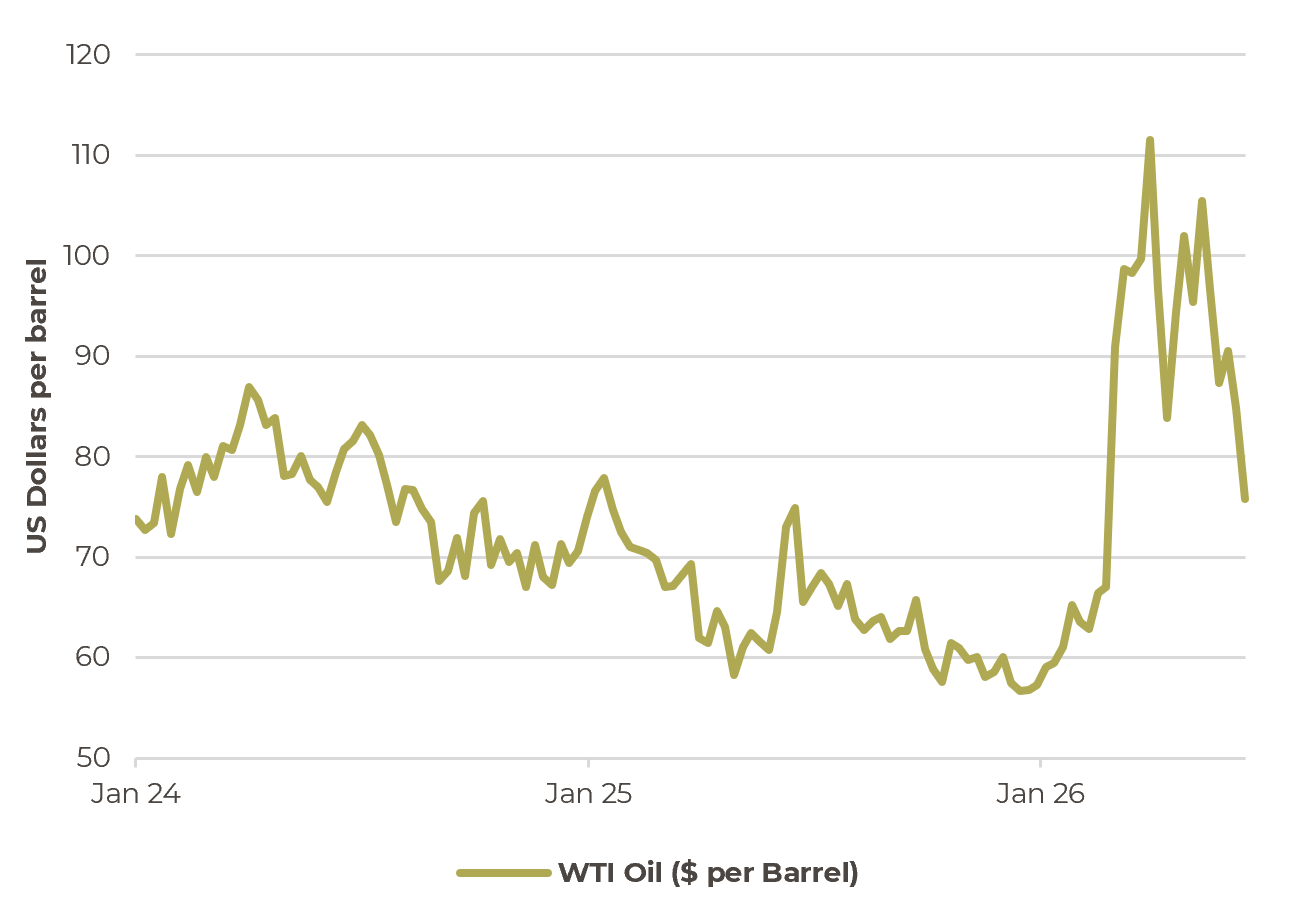

In the short-term the extension to the ceasefire appears to signal that neither the US or Iran want to reengage militarily (although Israel is less clear). This has resulted in a fall in oil prices over the past few days reflecting expectations that the Strait of Hormuz will reopen to normalise the flow of oil and natural gas around the world.

West Texas Intermediate (WTI) oil price has fallen on hopes of peace.

Source: Bloomberg, Artorius

Mind the Gap?

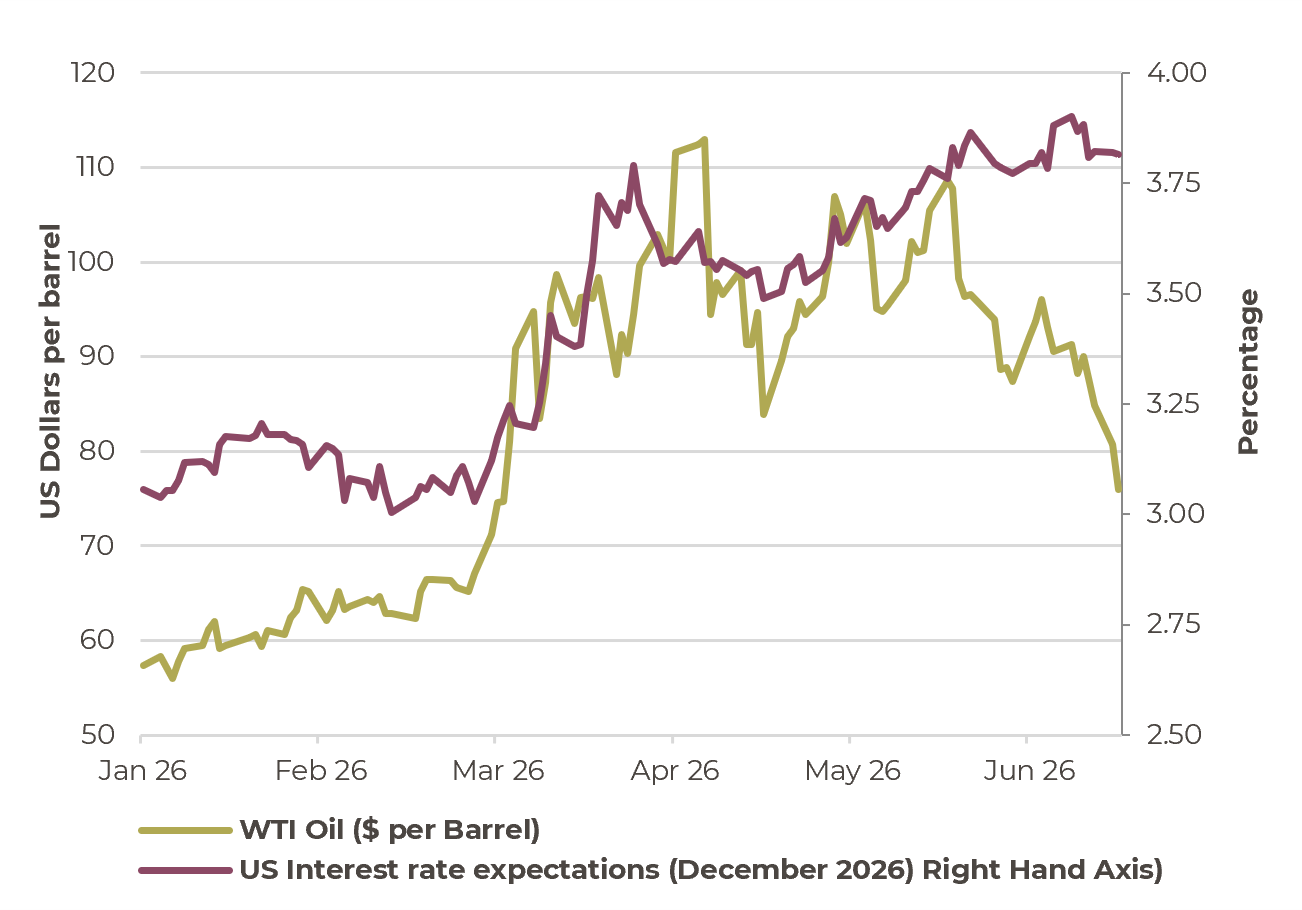

Lower oil prices are a welcome thing. It should reduce inflationary pressure, albeit time lags will mean that inflation is likely to remain above central bank comfort levels for the remainder of 2026. This may explain why interest rate expectations for the end of 2026 remain unmoved.

US markets, which had previously priced rates at ~3% by the end of 2026, are now implying limited change from current levels. Even in 2027, forward expectations suggest rates rising toward ~4% by the middle of the year. This is in sharp contrast to the pre-war scenario when rates had been expected to fall to below 3%.

Despite oil prices falling in recent weeks, markets are not pricing in interest rates cuts for the rest of 2026

Source: Bloomberg, Artorius

The Federal Reserve has a new Chair, Kevin Warsh, and this week saw his first meeting overseeing interest rate policy. While he was appointed by President Trump to be a dove (i.e. reduce interest rates), his first meeting saw the Federal Reserve unanimously leave rates unchanged at 3.5%-3.75%. The messaging was more hawkish than anticipated, he signalled a stronger focus on restoring price stability amid persistent inflation and elevated geopolitical uncertainty. His debut marked a notable shift in communication style (his statement was just 132 words) with less reliance on forward guidance and an emphasis on data-dependent policymaking.

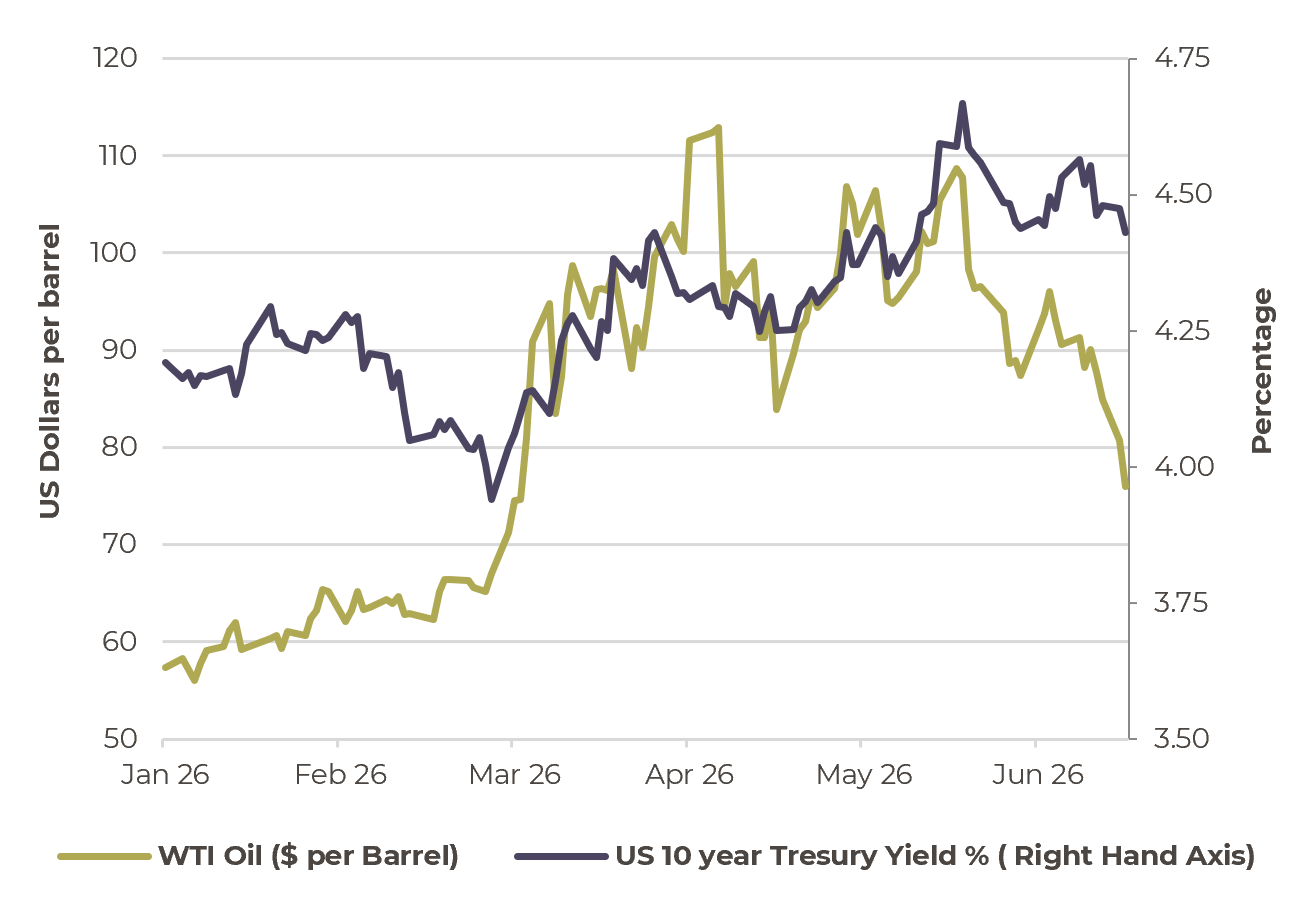

Whilst oil prices have fallen in recent weeks, US bond yields remain above pre-war levels

Source: Bloomberg, Artorius

A flood of equity

‘The times they are a-changin’. Bob Dylan wrote a song about it. For years US companies have engaged in share buybacks. Sometimes funded by increasing debt but generally funded by strong cashflows. As capital was returned to shareholders, the equity market was shrinking, which resulted in the invention of the term ‘de-equitisation’ to explain the phenomenon.

De-equitisation saw the number of companies listed in New York fall from a peak of 6,500 in 1997 to 4,700 in 2024. In addition, as companies bought back their own equity, there were fewer shares available for investment. And given the timeless law of supply and demand, as supply has fallen, prices have risen. Some commentators believe this is one of the factors that has contributed to the strong historical returns from US equities.

This trend is now reversing rapidly. The IPO of SpaceX raised an initial $75bn when it floated on the Nasdaq on Thursday 11th June. This valued the company at $1.75trillion, the largest IPO in history, and there is more to come.

Even though the sums are so large ($75bn for SpaceX and probably the same again for OpenAI and Anthropic IPOs), very little of the company is actually available for investing. SpaceX raised $75bn which at the time of the IPO amounted to less than 4% of the company’s value.

While many investors took part in the IPO, others will only gain exposure to the likes of SpaceX when they become part of an index. Index methodologies vary, but historically, most have required new listings to "season" for several months following their entry into the public market. This period gives stocks time to demonstrate their investability before being added to an index. However, per recent announcements from Nasdaq, FTSE Russell, and others, some index providers are changing their rules to allow faster entry for large IPOs. This could well result in a scarcity premium and result in strong price moves post flotation.

In addition to the IPOs, there has been significant fund raising by companies already listed. Instead of returning capital through buybacks, companies are starting to ask investors for more money.

Alphabet (Google) is looking to raise $80bn. An initial $30bn offering with a further $10bn investment secured from Berkshire Hathaway. The remaining $40bn will be raised later in the year subject to market conditions. Meta (Facebook) is reportedly looking at raising funds to invest into its AI platform and ceased its buyback program last year. Oracle expects to raise $45 to $50 billion of gross cash proceeds during the 2026 calendar year. The company plans to achieve its funding objective by using a balanced combination of debt and equity financing.

This represents a marked reversal of capital flows from the past decade and is reminiscent of the late 1990s when technology and telecom giants raised capital to invest into the then new world of the internet.

It is notable that, despite their strong earnings growth, it is the US technology giants who are the primary capital raisers. Whether these companies ultimately justify their implied valuations – or whether the current expectations embedded in the AI narrative prove too optimistic – remains an open question.

Conclusion

With a Memorandum of Understanding (MoU) between Iran and the US scheduled for signing on 19 June, expectations are rising that the fragile ceasefire may transition into a more durable peace agreement. Oil prices have fallen in expectation that the Strait of Hormuz will be unblocked and global energy supply will return to some sense of normality. Lower oil prices should alleviate inflationary pressures, although the March price spike will continue to feed through into inflation data in the near term.

The new Chair of the Federal Reserve, Kevin Warsh, has signalled a potential shift in the policy framework. However, he may not be able to change the interest rate, as the policymaking committee is currently divided between those seeking to cut rates and those willing to keep rates on hold (or even raise them).

The US economy has been resilient even in the face of higher oil prices, with growth largely supported by investment in Artificial Intelligence (AI). Until recently funding for AI spending has come from Private Equity investing into private companies such as Anthropic and OpenAI, while publicly listed companies have funded their investment spending through free cash flow and borrowing but this is changing as the scale of investment increases.

Recent weeks have seen the Initial Public Offering (IPO) of SpaceX, which raised $75 billion, with further listings from Anthropic and OpenAI anticipated. At the same time, listed companies (Meta, Alphabet, Oracle) are increasingly raising equity capital. This marks a notable shift from the past decade, during which US corporates have been net buyers of equity via share buybacks, supporting equity returns.

If inflation pressures ease as oil prices fall, interest rates remain low and earnings remain robust, investors may be willing to provide new capital to companies at current levels.

*Any feedback provided can be anonymous

Important Information

Artorius provides this document in good faith and for information purposes only. All expressions of opinion reflect the judgment of Artorius at 19th June 2026 and are subject to change, without notice. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete; we do not accept any liability for any errors or omissions, nor for any actions taken based on its content.

The value of an investment and the income from it could go down as well as up. The return at the end of the investment period is not guaranteed and you may get back less than you originally invested. Past performance is not a reliable indicator of future results.

Nothing in this document is intended to be, or should be construed as, regulated advice. Reliance should not be placed on the information contained within this document when taking individual investment or strategic decisions.

Any advisory services we provide will be subject to a formal Engagement Letter signed by both parties. Any Investment Management services we provide will be subject to a formal Investment Management Agreement, which will include an agreed mandate.

Artorius Wealth Management Limited is authorised and regulated by the Financial Conduct Authority. Artorius is a trading name of Artorius Wealth Management Limited.

FP20260619001