Real rather than artificial profits

Real rather than artificial profits

Summary

The uneasy truce in the Gulf continues to buffer markets. Heightened oil price volatility is resulting in swings in interest rate expectations and bond yields. Higher bond yields provide a challenging backdrop for economic growth as the elevated cost of capital impinges on the housing market and business investment.

Against this backdrop, equities remain supported by the resilience in corporate profitability. Companies have delivered results that have been better than expected. This is driven by stronger revenues but also higher profit margins. Whilst technology giants have been at the forefront of these upgrades, they have been present across the world.

The new head of the Federal Reserve, Kevin Warsh, has indicated that he will change the policy environment at the Federal Reserve. However, he may not be able to drive change in the interest rate, as the policymaking committee is currently divided between those seeking to cut rates and those willing for rates to be held steady. With inflation likely to remain higher than policymakers would like due to the impact of the Gulf conflict, central bank decision makers face a challenging backdrop.

Impressive profits

The quarterly corporate earnings season is nearly at an end. On any measure, revenue or profits, it has been very strong. And whilst the US profits have been leading the way, other regions have also enjoyed better than expected outcomes. And we suggest that this is the main driver of markets, despite the understandable concerns and remaining risks from the Gulf conflict.

The surprise in the US is coming from a better than expected increase in revenues. Combined with elevated profit margins, the earnings improvement has been significantly better than expected. At this late stage of the earnings season, the (blended) quarterly revenue growth rate for the S&P 500 is 11.4%. If 11.4% is the actual growth rate for the quarter, it will mark the highest revenue growth rate reported by the index since Q2 2022 (13.9%).

The revenue backdrop is telling. There has been an acceleration of revenue growth in the US. Normally, sales growth accelerates coming out of a recession and then finds a plateau before fading into the next recession. The acceleration of sales growth is striking given that the state of the US economy is ok but not ebullient.

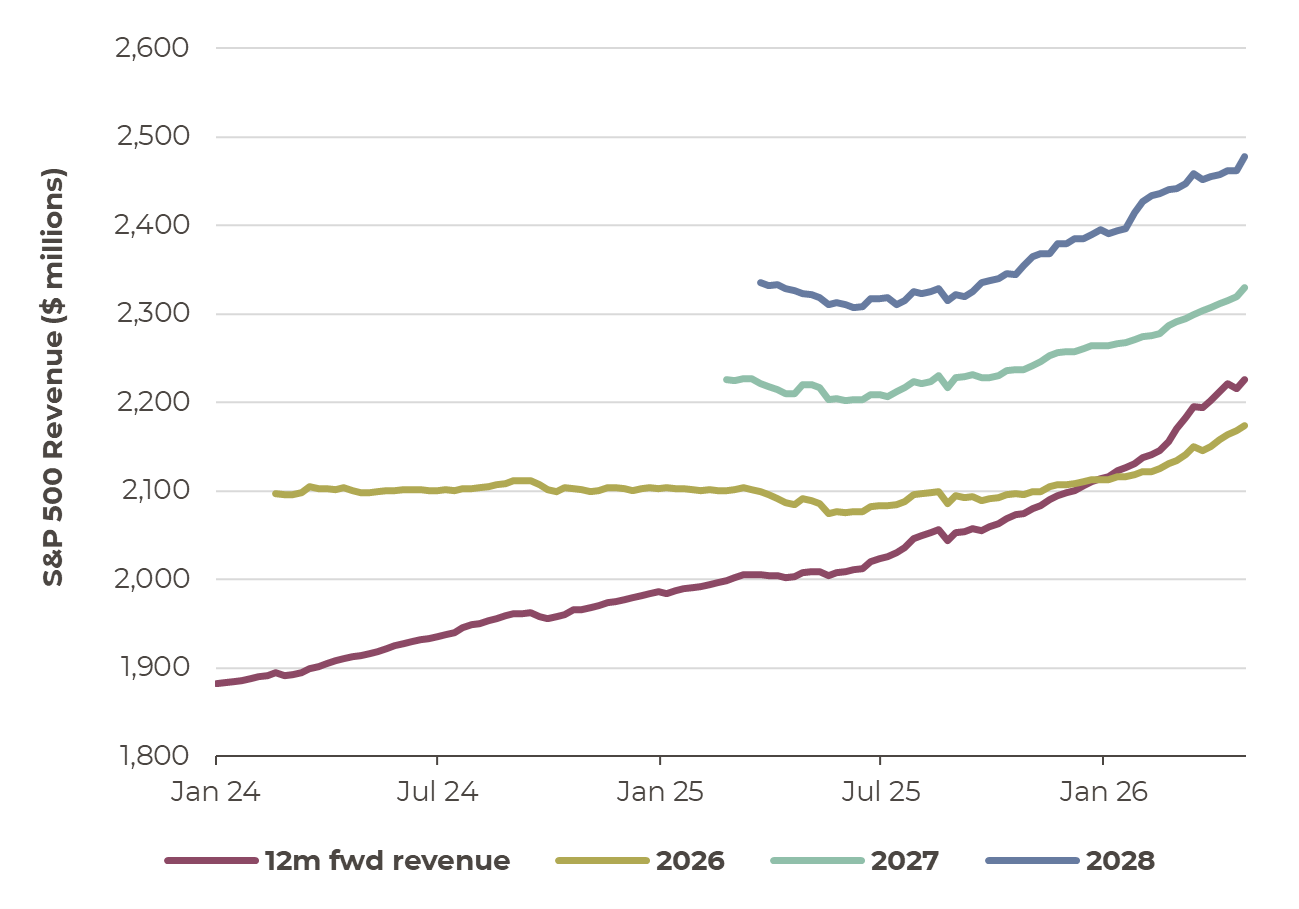

After a few years of solid 5% revenue growth, current expectations are that revenues in the US will grow by 7.2% in 2026 and a further 6.4% in 2027. And these estimates have trended upwards as estimates for 2026, improving by 5 percentage points over the past year.

S&P 500 revenue estimates

Source: Bloomberg, Artorius

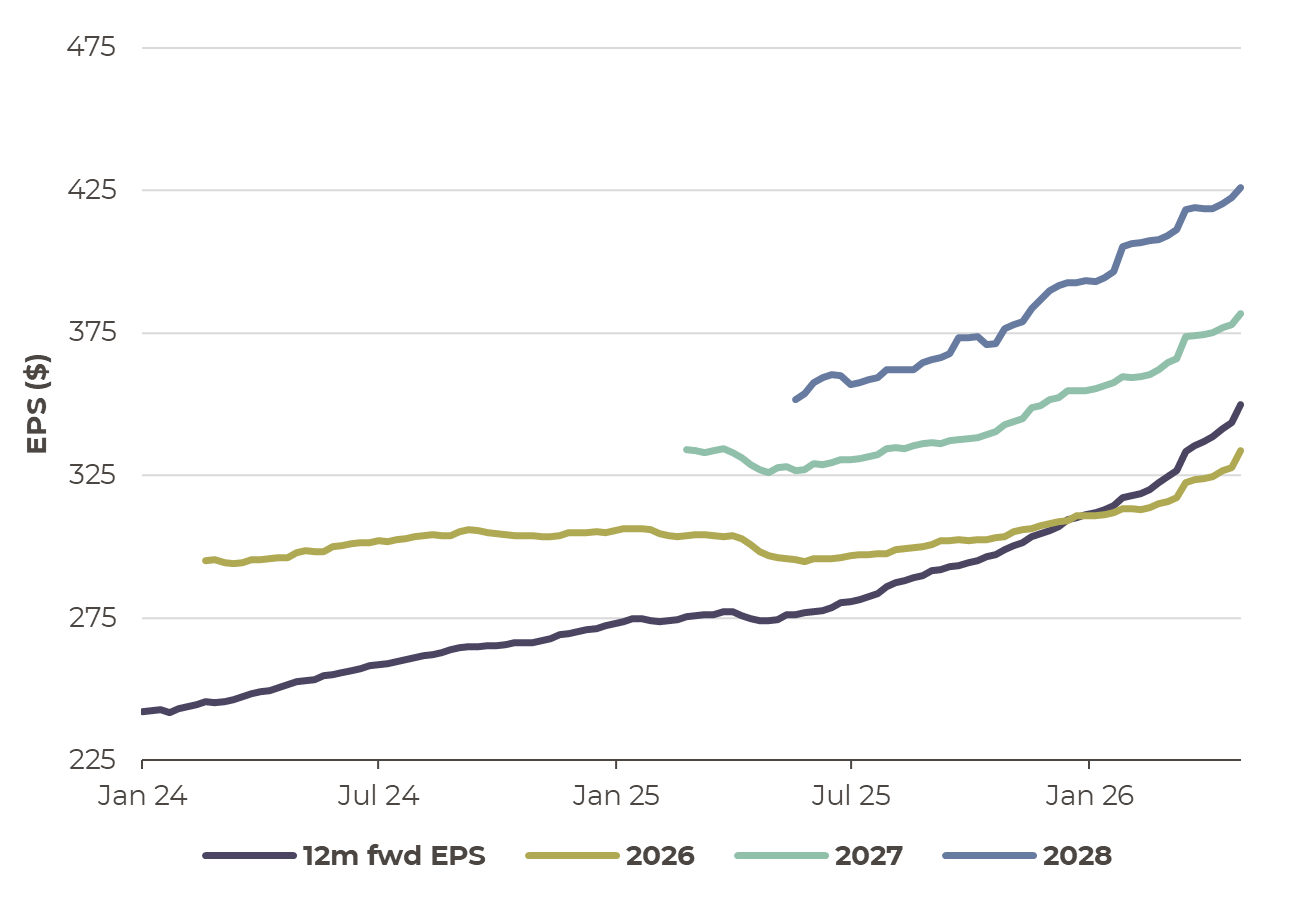

The robust revenue backdrop provides ground for the strength of earnings which also continue to be better than expected. Profits are a key driver of returns for investors, and in the face of uncertainty resulting from the Gulf conflict, the earnings backdrop has insulated the equity market from the invidious impact of oil price volatility and the prospect of higher interest rates.

S&P 500 Earnings per Share (EPS) estimates

Source: Bloomberg, Artorius

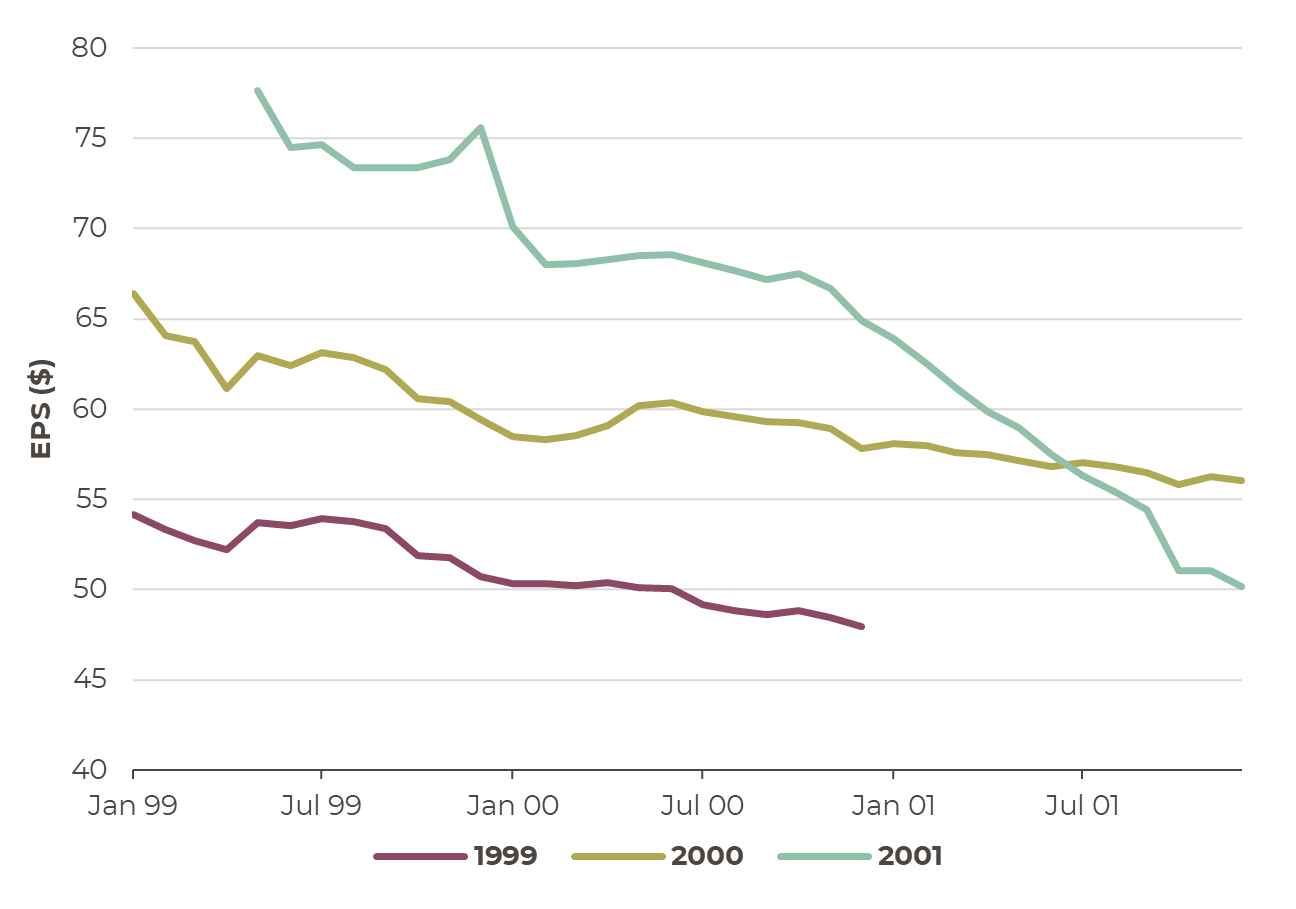

It’s rare to see earnings accelerate like this during a mid-cycle expansion. Fittingly, the best analogy is 2018, when Trump’s Tax Cuts and Jobs Act caused an earnings boom. That was Trump 1.0 and we are now in 2.0. For now, earnings have been growing so strongly that it’s hard to call this a bubble. Bubbles are about excessive valuations and a lack of earnings growth, as was the case in 1999-2000. In the technology bubble of 1999-2000, equity markets rose even though earnings were being reduced and interest rates were being increased.

S&P 500 Earnings per Share (EPS) estimates

Source: Bloomberg, Artorius

If earnings (and revenues) remain resilient it appears to be a boom. And the boom is showing up in stronger economic growth and investment spending in the US economy. The risk is that the companies driving the earnings bonanza have moved from being cash-generative to borrowing to finance the investment boom. This works if the on-going revenue growth translates into higher profits for those technology companies. Any check on growth, be that a scare like Deep-Seek in January 2025, or a reappraisal of the costs of capital as bond yields rise, may bring about a change in momentum and provide a wider challenge to the market.

Delayed peace?

Whilst the consequences of the US-Israeli attacks on Iran continue to be felt in higher oil prices, markets appear to be tolerant of the uncertainty. The fragile peace that descended in April has continued (which is good news) but the seeming lack of progress in arriving at a longer-term resolution is concerning, especially with regards the opening of the Strait of Hormuz.

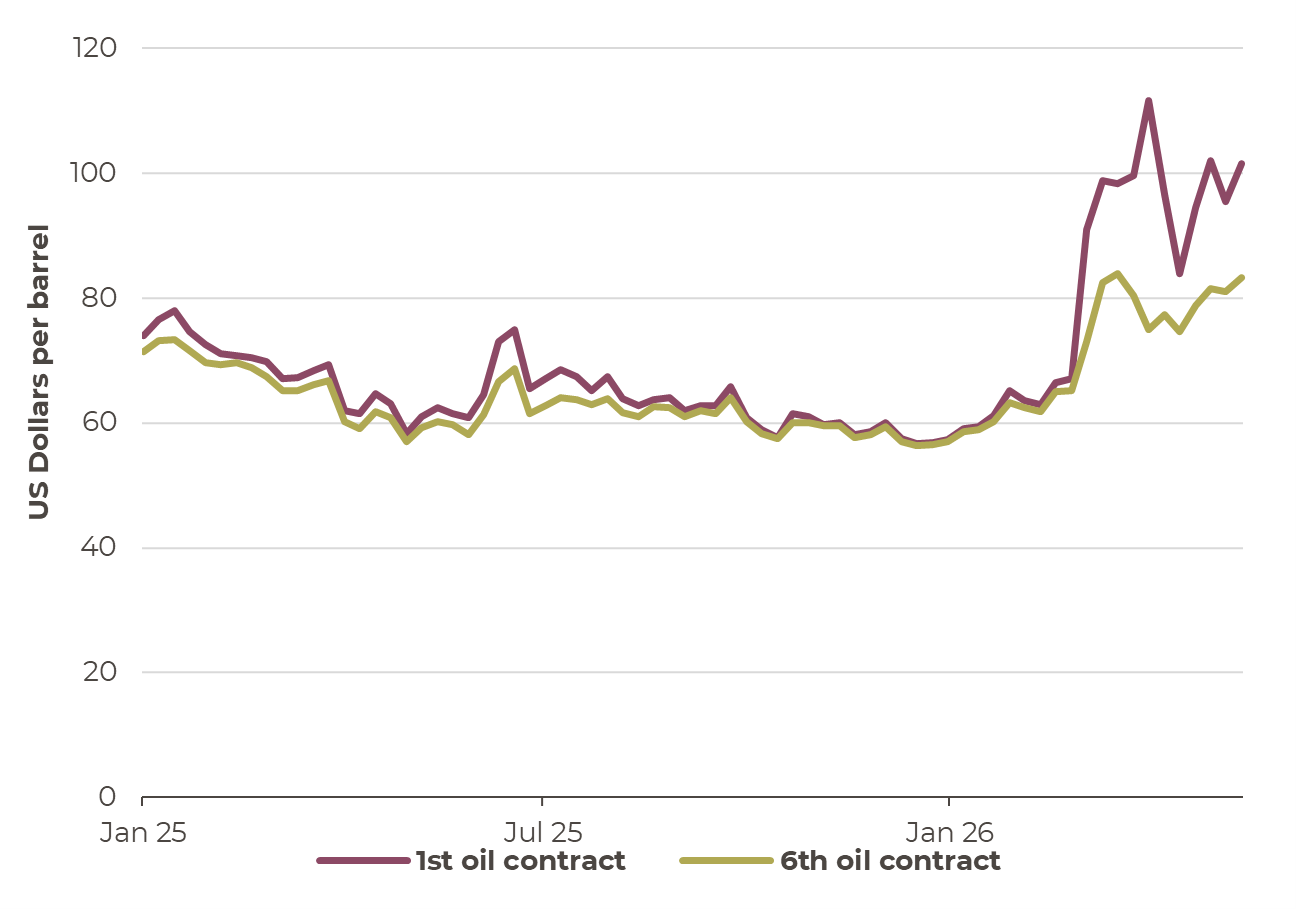

The chart on the right shows the oil price both at the first month contract (the oil price ‘most’ commentators will be referring to) and the sixth month contract, i.e. the price at which the market is willing to pay for oil in six months’ time - effectively what the market expects the oil price will be then. Contracts allow companies that use oil to pre-purchase it months ahead and know what price they will eventually have to pay for delivery. For example, in January the sixth month contract will be the expected oil price in June. Currently the sixth month contract relates to the price of oil expected in November.

Normally, the first month and sixth month contract price are very similar, with an average difference of just $3.50 between contracts over the past five years. The US-Israeli attacks on Iran at the end of February saw the first month oil price jump up sharply from around $70 to $100 per barrel. The price of the sixth month contract ‘only’ rose to $80. At the peak there was a $35 per barrel difference between first and sixth month oil contracts.

Even after the immediate escalation of the Russian invasion of Ukraine in 2022, the gap only reached $15 and quickly normalised as oil prices gradually fell through 2022.

Oil price volatility is one sign of the impact of the on-going tensions, but the supply of non-oil commodities also matters. The Gulf region is a major supplier of helium (used in semi-conductors) and urea (fertilizer). The consequences of the war’s disruption may extend from the very food on our global table to the upper reaches of technology. From food to virtual reality, the impact may become very present in our economies.

Oil prices: First and six month contracts. The gap between ‘near-term’ oil prices and ‘future’ oil prices reflects a belief (hope) that the conflict and disruption to the Straits of Hormuz will not last too long, but oil prices are expected to remain higher than in 2025 with inflationary consequences

Source: Bloomberg, Artorius

From oil to inflation

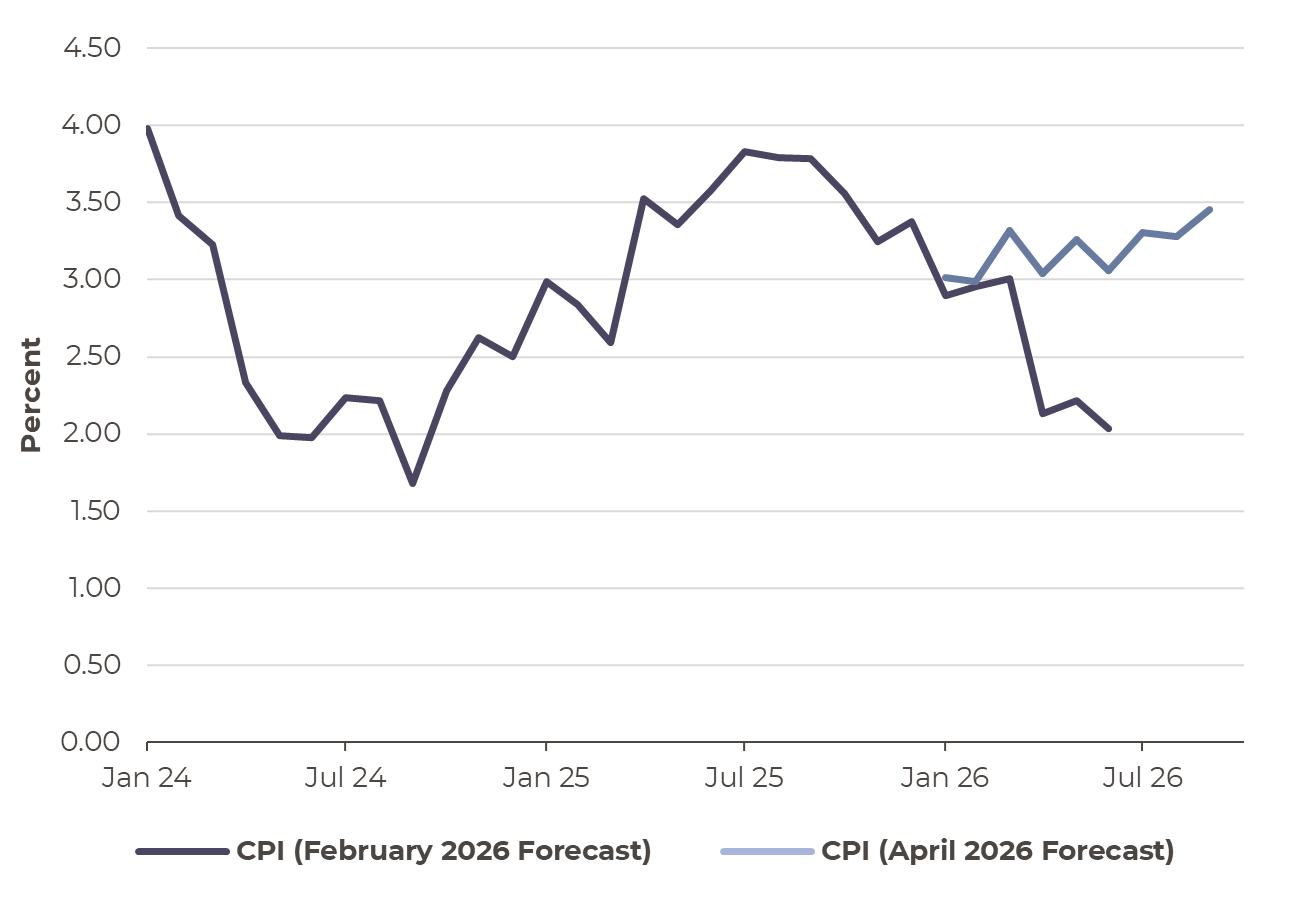

The inflationary impact of the war is showing up in the inflation data. In the UK, in the recent Monetary Policy Report (the old Inflation Report for readers of a certain genre), the Bank of England presented an update on their thinking on the outlook for inflation in the UK. The report highlighted that the forecast made in February 2026 had concluded that the UK inflation rate would fall to around 2% in the middle of 2026.

Given the degree of uncertainty for the outlook (due to the conflict and oil price reaction), the Bank has a range of scenarios. In the central case the inflation rate is expected to remain above 3% for much of the forecast period. The chart shows the gap between the inflation rate forecast made in February 2026 and April 2026.

The good news may be that if (and it is an if) inflation stays below 4%, the second order effects of higher inflation, i.e. wage inflation, may be more modest than would be the case if inflation races higher, as it did in 2022.

The Bank of England UK inflation forecast (as measured by the Consumer Price Index (CPI)) has changed between January and April as a result of the conflict.

Source: Bloomberg, Artorius

Bond yields and guilty yields?

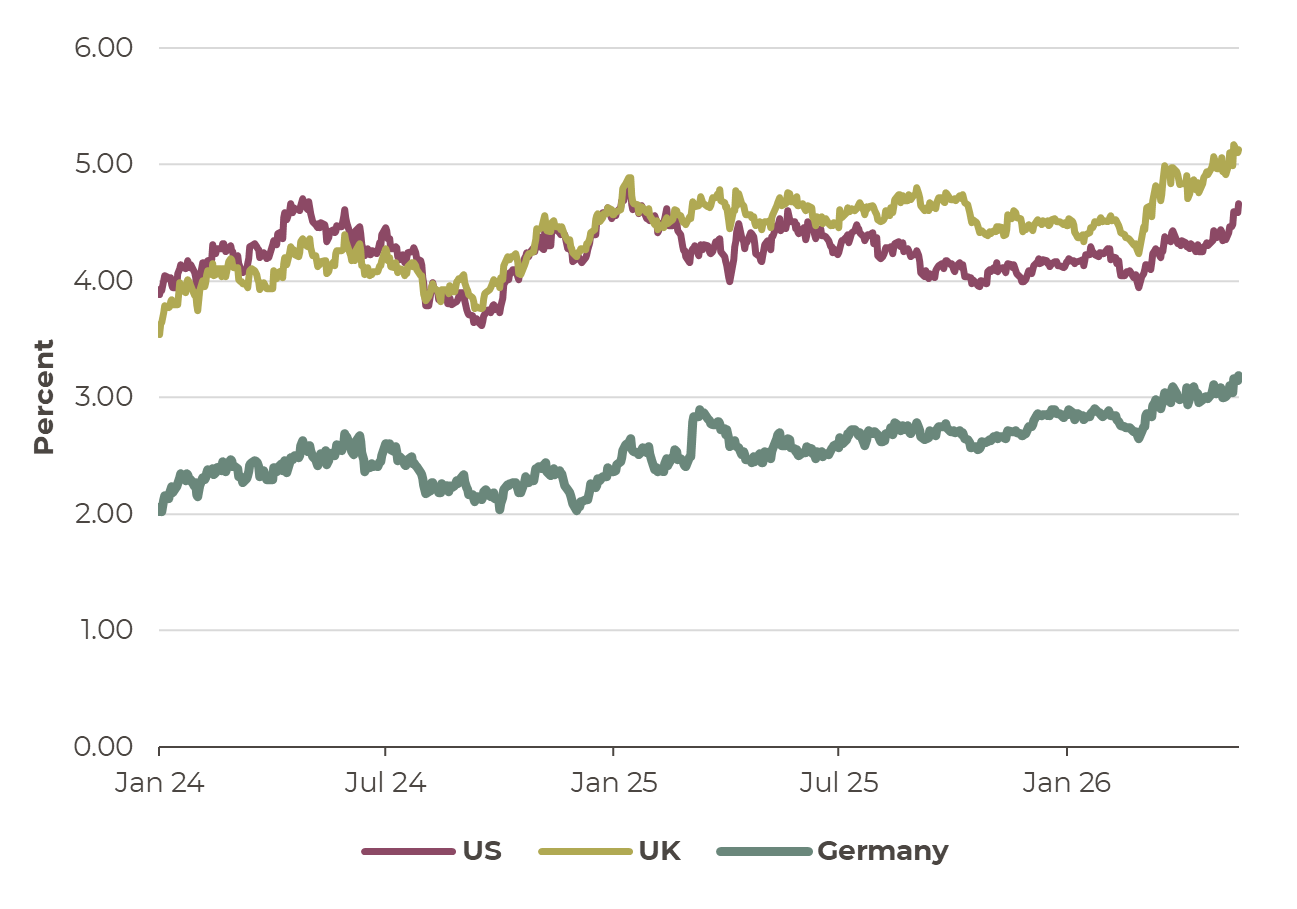

The changing inflationary backdrop has resulted in a shift in interest expectations. Whereas previously interest rates were expected to be cut in 2026, expectations are now that interest rates may need to rise in the UK and the US. This has contributed to a rise in bond yields across the world.

It is fair to say that the UK has seen its 10 year government bond yield increase by more than other countries in recent months (by about 0.3%), but the major move in bond yields has been global. It is right to suggest that the perilous position of the Prime Minister and the debate around his replacement hasn’t helped. The unwillingness of Labour MPs to engage in fiscal discipline would challenge the ability of the next Prime Minister (or indeed this one) to effect change that resonates with the electorate.

10 year bond yields have risen across the world, as inflation pressures are universal.

Source: Bloomberg, Artorius

New boss at the Federal Reserve

President Trump has his man. His nominee, Kevin Warsh, has been confirmed by the Senate and is set to become the new Chair of the Federal Reserve. As the new head of the US Central Bank, Warsh will have influence over the direction of travel in monetary policy. However, his will be just one vote amongst 12 when it comes to setting interest rates. As shown at the last Federal Reserve policy meeting, there are differing views. Out of the 12 voting policy makers, one voted to reduce rates and three voted to change the language to a more hawkish tone as they did not support the easing bias in the Federal Reserve’s statement.

Investors expect that the Federal Reserve is likely to leave interest rates unchanged for the near future despite the incoming Chair, given a stable unemployment rate and inflation moving further away from target. Warsh has indicated that he is seeking to make a change to how the Federal Reserve operates, which may change future interest rate expectations.

Conclusion

The uneasy truce in the Gulf continues to buffer markets. Heightened oil price volatility is resulting in swings in interest rate expectations and bond yields. Higher bond yields provide a challenging backdrop for economic growth as the elevated cost of capital impinges on the housing market and business investment.

Against this backdrop, equities remain supported by the resilience in corporate profitability. Companies have delivered results that have been better than expected. This is driven by stronger revenues but also higher profit margins. Whilst technology giants have been at the forefront of these upgrades, they have been present across the world.

The new head of the Federal Reserve, Kevin Warsh, has indicated that he will change the policy environment at the Federal Reserve. However, he may not be able to drive change in the interest rate, as the policymaking committee is currently divided between those seeking to cut rates and those willing for rates to be held steady. With inflation likely to remain higher than policymakers would like due to the impact of the Gulf conflict, central bank decision makers face a challenging backdrop.

*Any feedback provided can be anonymous

Important Information

Artorius provides this document in good faith and for information purposes only. All expressions of opinion reflect the judgment of Artorius at 21st May 2026 and are subject to change, without notice. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete; we do not accept any liability for any errors or omissions, nor for any actions taken based on its content.

The value of an investment and the income from it could go down as well as up. The return at the end of the investment period is not guaranteed and you may get back less than you originally invested. Past performance is not a reliable indicator of future results.

Nothing in this document is intended to be, or should be construed as, regulated advice. Reliance should not be placed on the information contained within this document when taking individual investment or strategic decisions.

Any advisory services we provide will be subject to a formal Engagement Letter signed by both parties. Any Investment Management services we provide will be subject to a formal Investment Management Agreement, which will include an agreed mandate.

Artorius Wealth Management Limited is authorised and regulated by the Financial Conduct Authority. Artorius is a trading name of Artorius Wealth Management Limited.

FP20260522001