Oil & Chips

Oil & Chips

Despite a ceasefire in the Middle East, underlying geopolitical tensions remain elevated. Yet market behaviour through April could easily suggest a return to stability: the MSCI All Country World Index has risen around 10%, while the S&P 500 is also up 10% (in USD), marking the best monthly performance since 2020.

In the US, the dropping of the criminal investigation into Federal Reserve (Fed) Chair Jerome Powell has also cleared the way for Kevin Warsh’s expected confirmation as his successor. Against this backdrop, this week’s investment comment examines the drivers behind recent market strength, analyses Q1 earnings momentum and considers the potential implications of a new Fed chair for the remainder of Trump’s term.

No Spillover

Investors could be forgiven for concluding that all is well in the world, despite ongoing conflict in the Middle East. In the lead-up to the Iran war, markets had already experienced an AI-driven sell-off that extended into March. While the dominant narrative attributed the weakness in March to geopolitical tensions, the Strait of Hormuz remains effectively constrained and oil is still above $100 per barrel. This raises the question of why markets are rallying so strongly.

Investors of a certain age may recall the oil embargoes and the inflationary surges of the 1970s, but the world in 2026 is far less dependent on oil. Crude oil production now accounts for roughly 2% of global output - around one quarter of the share it represented during the 1979 Iranian Revolution. Of that, only about one-fifth passes through the strategically sensitive Strait of Hormuz, which is now the focal point of geopolitical tension.

Oil’s subdued reaction

Oil has risen modestly since the war began compared with earlier price spikes.

| Number of Months | Low Price | High Price | Real Price Change, WTI | |

|---|---|---|---|---|

| August 1973 to October 1974 | 15 | $26 | $71 | 173% |

| February 1979 to April 1980 | 15 | $71 | $159 | 124% |

| July 1990 to September 1990 | 3 | $43 | $97 | 126% |

| February 2007 to June 2008 | 17 | $94 | $209 | 122% |

| February 2009 to April 2011 | 27 | $64 | $164 | 156% |

| May 2020 to May 2022 | 25 | $24 | $128 | 433% |

| March 2026 to April 2026 | 2 | $67 | $105* | 57% |

Note: Prices adjusted for inflation. * Latest close (30th April 2026)

Source: Artorius, Bloomberg

Inflation expectations have remained broadly stable. The five-year breakeven inflation rate has increased by just 0.2% since the start of the conflict, while the Fed’s decision on Wednesday to hold the target range at 3.5%–3.75% suggests policymakers do not expect the current tensions to trigger a sustained inflation shock in the near term, and are likely willing to look through any temporary price pressures stemming from the conflict.

Oil markets are in backwardation – meaning prices today are higher than those expected in the months ahead, pointing to a meaningful decline over time. This suggests the market is pricing in a move towards $70 per barrel by early next year, even in the absence of any clear indication that the current conflict is nearing resolution. Taken together, this points to oil’s declining systemic importance and Iran’s reduced capacity to materially disrupt global energy markets, though it may also signal a degree of market complacency, with prices expected to follow a relatively orderly path despite ongoing geopolitical uncertainty.

There remains a risk that the conflict could escalate into a broader global confrontation. In such a scenario, sustained higher oil prices would likely weigh on consumption and sales, and any meaningful price pressure would be expected to feed through into higher inflation expectations - something that has not yet materialised. It is also unclear what impact lower consumption would have on the large technology companies that continue to drive equity markets. However, recent signals from Trump suggest a preference for de-escalation and a quicker resolution. With midterm elections approaching, a significant escalation is unlikely to be politically advantageous.

Against this backdrop, Gulf Arab states are likely to prioritise the expansion of pipeline infrastructure that routes oil north through the Mediterranean, enabling them to bypass the Strait of Hormuz and, over time, erode Tehran’s strategic leverage. Saudi Arabia and the United Arab Emirates already have limited bypass capacity in place, and both are expected to further develop and scale these alternative routes. However, the timescale for any meaningful shift in regional dynamics is likely to be extended rather than immediate. As a result, while Iran’s ability to exert pressure through control of key energy chokepoints may diminish over time, the near-term impact is more limited. Looking further ahead, the Persian Gulf is likely to have materially stronger bypass infrastructure than it does today, reducing the region’s vulnerability to disruption.

These structural shifts are unfolding alongside a strong start to the year for corporate earnings, with Q1 results coming in broadly ahead of expectations so far.

SOX Surge

Nearly a third of the way through Q1 earnings season, results are running around 12% ahead of expectations, comfortably above the historical average of roughly 7%. This is the strongest upside surprise outside of a post-recession rebound and sits above both 5- and 10-year earnings averages.

The outperformance has been heavily concentrated in the technology sector, driven in large part by the unprecedented buildout of AI-related data centre infrastructure, leading to all-time highs across equity markets.

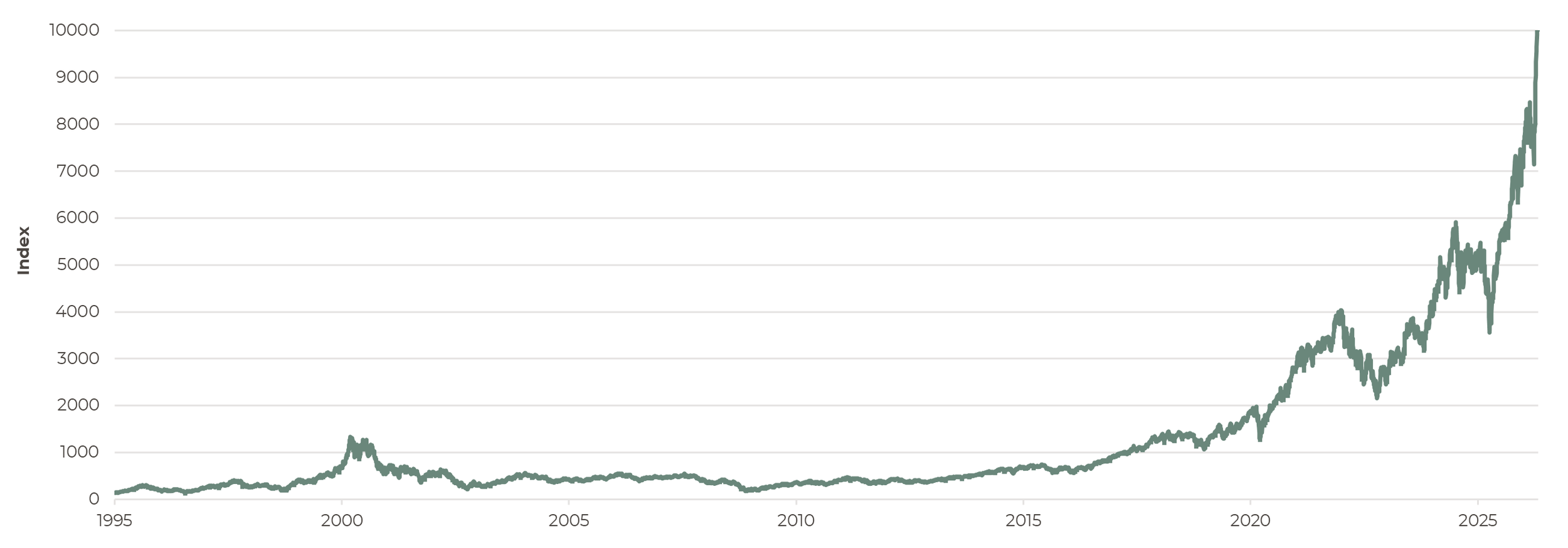

The Philadelphia Stock Exchange Semiconductor Index, widely known as the SOX, has risen 47% over the past 19 trading days (as of 27.04.2026) since markets began to price in a perceived easing in tensions around Iran. Remarkably, it has posted gains in every one of those trading days - the longest winning streak in its history.

SOX Index

Source: Artorius, Bloomberg

Semiconductor manufacturers sit at the centre of the AI investment cycle, as every data centre buildout and large language model begins with demand for advanced chips. Over the past month, earnings expectations for the sector have surged accordingly. Using last year’s earnings, the SOX trades at an elevated multiple of around 60x earnings. But using forward earnings, which have been revised higher recently, valuations look less stretched.

Ultimately, the AI narrative rests on significant margin expansion, underpinned by the expectation that chipmakers can capitalise on their strategic position to command higher pricing from the hyperscalers, who remain locked in intense competition for AI dominance. This dynamic is increasingly being reflected in profitability assumptions.

Since the launch of ChatGPT in late 2022, the SOX index has expanded from roughly 4% to 16% of the S&P 500’s total market capitalisation. The question, however, is whether chipmakers truly have as much pricing power as is often assumed. Much of their output is ultimately purchased by other listed companies, meaning that revenues at firms such as Nvidia and Intel effectively translate into capital expenditure for someone else further down the value chain.

Wednesday’s hyperscaler results (Microsoft, Alphabet, Amazon, Meta) reinforced this backdrop, with continued strong AI-driven demand alongside sustained, and in some cases rising, capital expenditure. This supports near-term semiconductor demand but further underscores the extent to which the earnings outlook for the sector is increasingly tied to a small number of hyperscalers’ investment decisions rather than broad-based end-market demand. The key question for medium-term returns is therefore whether AI monetisation can scale sufficiently to sustain current levels of infrastructure spending.

Succession

In Washington, the Department of Justice last week dropped its criminal investigation into Federal Reserve Chair Jerome Powell, removing a key procedural hurdle to the transition to Kevin Warsh as Fed chair. The episode, centred on scrutiny of Fed building renovations, had become increasingly politicised amid sustained pressure over monetary policy. The breakthrough came after Senator Thom Tillis withdrew his objection to advancing Warsh’s nomination once the investigation ended.

Attention then shifted following Powell’s final scheduled speech on Wednesday, where he suggested he may continue to serve on the Federal Reserve’s Board of Governors, remaining as a governor under his successor, Kevin Warsh, until “it’s appropriate for me to leave”. With the leadership transition to Kevin Warsh as Fed chair now in focus, attention turns to the potential policy implications of a Warsh-led Fed, particularly around the balance sheet, the pace of policy normalisation, and the broader reaction function. We will continue to monitor developments closely as both the policy outlook and institutional dynamics evolve over the coming months and explore the implications in more detail in next week’s commentary.

Yuval Peshchanitsky

Portfolio Analyst

*Any feedback provided can be anonymous

Important Information

All expressions of opinion reflect the judgment of Artorius at 1st May 2026 and are subject to change, without notice. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete; we do not accept any liability for any errors or omissions, nor for any actions taken based on its content. The value of an investment and the income from it could go down as well as up. The return at the end of the investment period is not guaranteed and you may get back less than you originally invested. Past performance is not a reliable indicator of future results. Nothing in this document is intended to be, or should be construed as, regulated advice. Artorius provides this document in good faith and for information purposes only. Reliance should not be placed on the information contained within this document when taking individual investments or strategic decisions.

Artorius Wealth Management Limited is authorised and regulated by the Financial Conduct Authority. Artorius is a trading name of Artorius Wealth Management Limited.

FP20260501001