Clouds of war inflating away the benign backdrop

Clouds of war inflating away the benign backdrop

Summary

The US-Israeli attacks on Iran interrupted the benign and improving backdrop seen at the start of 2026 and will have consequences for economies and investment markets.

It remains unclear what the objectives are and how military tensions can dissipate in the near term. Given the uncertainty we have sketched out a few scenarios based on possible outcomes and their consequences for oil prices, economies, interest rates and financial markets. Such scenario mapping frees us to think about different uncertainties rather than planning for any one particular eventuality.

There are scenarios that see a de-escalation of tensions, a fall in the oil price and a resumption of the global economic recovery, albeit a recovery that is likely to have stalled given the war. Each day that military threat restricts the flow of oil in the Strait of Hormuz and oil prices remain elevated and volatile, the risk builds of an economic slowdown. A downside scenario could result in a collapse of Iranian oil production, in the same way that Libyan oil production fell during the civil war, following the UK and France’s intervention (post the passing of the UN Security Council Resolution 1973). Iranian oil production is an important source of global energy and it would be a challenge to replace it over a prolonged period, which may give way to elevated oil prices.

Oil prices have increased by 57% since the end of February already resulting in higher petrol prices. Whilst the UK has higher petrol prices than the US, due to the high tax wedge in the petrol price, the rise of oil is having a larger immediate impact in the US where petrol prices have increased by 22% since the start of the war compared to ‘only’ 6.5% in the UK.

It is likely that the short-term effect of the war will show up in the inflation data. As a result, investors have shifted expectations for the path of interest rates in coming months. In the US, fewer rate cuts are now expected. In the UK, a few weeks ago markets had been pricing in rate cuts through the rest of 2026, but this has now changed to expectations that the Bank of England will raise interest rates. This is already transmitting itself into higher mortgage rates that in turn is likely to dampen the nascent recovery in activity that was building in the UK housing market.

While we wait for the news flow, there is so much we do not know, and what we think we know is subject to change at a moment’s notice.

Scenario mapping

After a period of global economic stability, albeit clouded by the threats to Greenland and the kidnapping of the President of Venezuela, the attacks on Iran by the US and Israel has brought greater uncertainty to the global economic outlook.

There are better qualified writers (those with deeper knowledge of the Middle East or intelligence matters) than most financial commentators but investment professionals do have to try to make sense of unfolding events and draw conclusions on behalf of clients.

Given the current uncertainty, the scenarios below consider different potential outcomes for Iran’s political leadership (‘regime’) and their economic implications. Whilst an economist will always look at the downside risks from elevated oil prices and the consequential impact for higher inflation and lower economic growth, there are two potential ‘upside’ scenarios in which oil prices fall.

| Regime | Conditions | Oil | Economics | |

|---|---|---|---|---|

| Regime Survival | Continuation | US intervention decreases/ceases — the current regime cuts a deal or fights to a draw | Risk premia remain high due to ongoing tensions and continued regional uncertainty | Inflation up and growth hit (especially so in Emerging Markets and Europe due to reliance on natural gas) |

| Regime change | Modern Authoritarian | Factions of the military, the Islamic Revolutionary Guard Corps, and clerics take power and cut a deal (Venezuela-like scenario) | Oil prices could ease due to a more stable or controlled outcome | An improvement in risk appetite and markets even though there may be a 'war-hit' in the near term but energy prices fall post-war |

| Democratic Transition | Improbable though not impossible — major elements of the political, military and religious leadership join protestors (Romania 1989 scenario) | Oil prices subside due to stability and enables longer term international investment into Iran (but likely take time for this to result in additional oil flow) | ||

| Civil War / Anarchy | U.S. and others intervene — political and military fracture into competing factions (Libya 2010 scenario) | Iran goes off-line in terms of oil production in the short-medium term | Oil prices high; other countries increase oil supply |

It is unclear how the blockade of the Strait of Hormuz can be cleared, especially as Iran has found the pressure point in the conflict. By effectively closing the shipping lanes and firing missiles at its Gulf neighbours, Iran has escalated the war. How drawn out this will be is linked to the duration of the blockade and how quickly normality can be established in shipping.

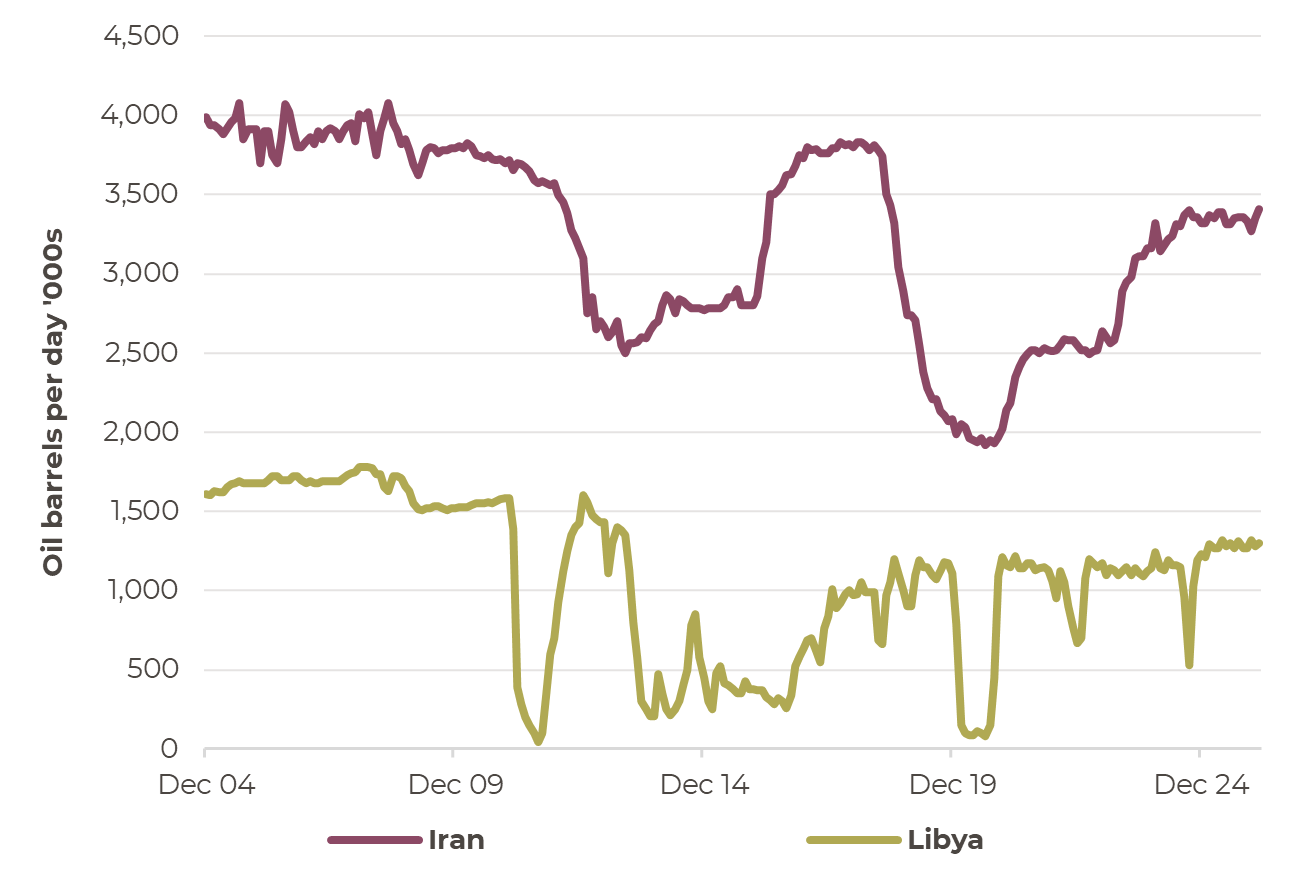

In the short-term higher oil prices will show up in inflation, especially petrol prices, more of which below. In the medium term, the scenario that possibly poses greatest risk is a Libyan style collapse of oil production should there be a disorderly regime change. Following intervention by the UK and France in 2011, the Libyan government collapsed later that year, and ongoing civil conflict and a subsequent deterioration in security from 2013 led to a prolonged drop in oil production. Current Iranian production levels are about three times as high as Libya, so it may be more challenging to replace if a similar disruption took place.

Libyan and Iranian oil production (Barrels of oil per day)

Source: Bloomberg, Artorius

Another inflation shock but a repeat of 2022 should be avoided

The most immediate economic effect of the current war is showing up in the prices of oil and natural gas. The escalation in the Gulf has caused an energy price shock given that 20% of the world’s oil supplies transit the Strait of Hormuz.

Oil prices matter as they are a cost of ‘doing’ business for much of the world. Likewise natural gas prices have been pushed higher by the attacks on Iran and Iran’s response. The closure of the Strait of Hormuz has meant that around 20-25% of global oil and gas supplies have slowed to a trickle. Higher oil prices will result in higher inflation and slower economic growth. If oil prices settle at $100 per barrel, then inflation in the US could be around 1% higher than it otherwise would have been. The impact is slightly less in the UK, but inflation is set to climb over the next few months.

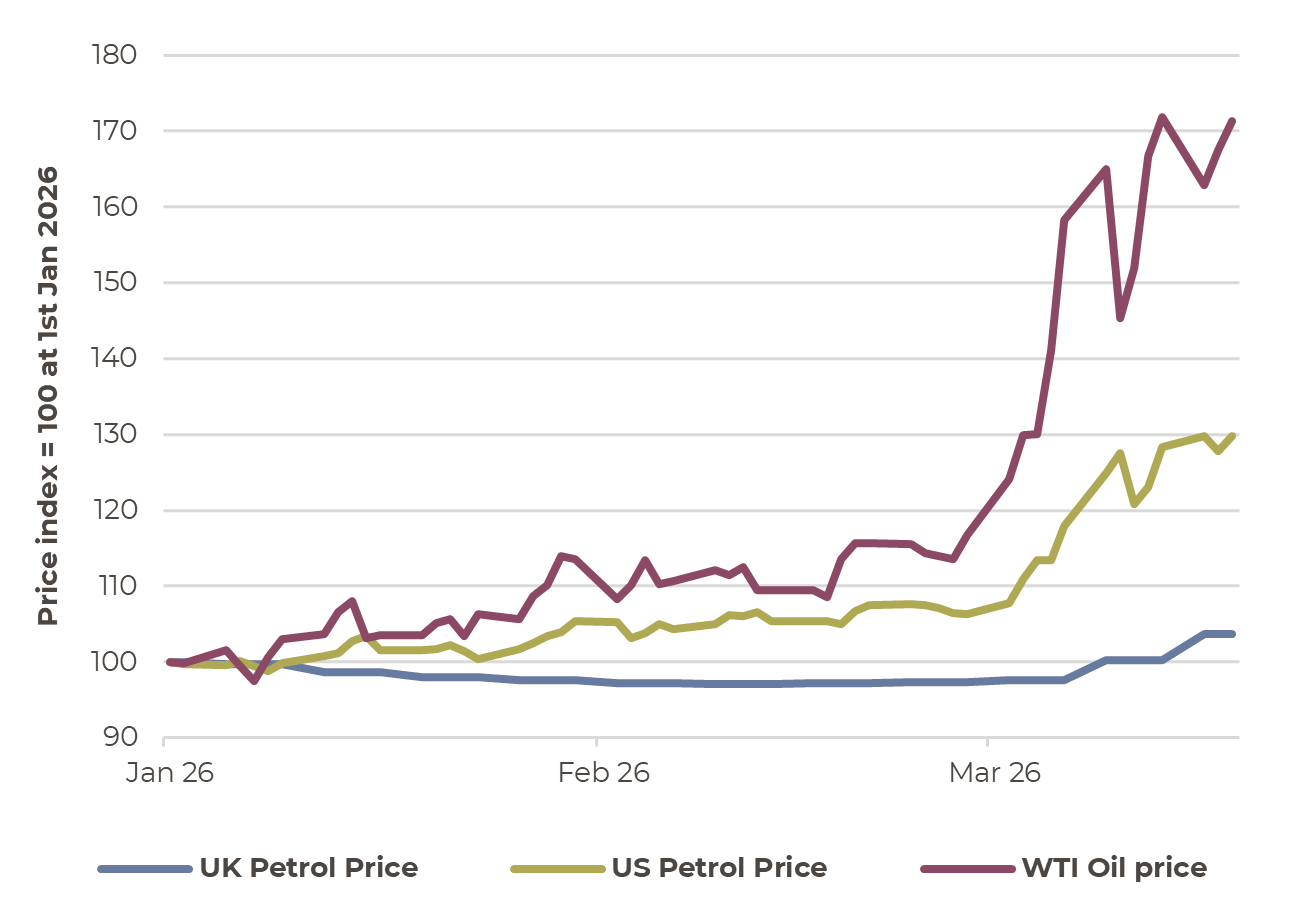

The immediate sign of the inflation shock is showing up already in petrol prices. The chart to the right shows the oil price and petrol prices in the US and UK since the start of 2026, (WTI (West Texas Intermediate) is a key benchmark price for crude oil). Oil prices have risen by around 70%, most of which has taken place since the US-Israeli attacks. US petrol prices have risen by just under 30% whilst the UK has ‘only’ seen a 4% increase since the start of the year.

The difference in the oil price impact on petrol prices is due to differing levels of tax in the petrol price. In the UK, oil only accounts for about 33% of the overall cost of petrol, the rest is mostly tax. In the US, oil is around 50% of the cost and so the US petrol price is more affected by changes in the oil price. Therefore, the inflationary impact of the oil price change will be less immediate in the UK than in the US.

The longer-term impact of the inflationary effect is likely to be determined by second order (indirect) effects, including policy responses. In the UK, if the government chooses to increase state benefits (UK State Pension and Universal Credit) and the minimum wage in line with headline inflation, then, as in 2022-23, inflation can rise to a higher level than the initial impact of energy prices would have suggested.

How oil, UK and US petrol prices have moved since 1st January 2026

Source: Bloomberg, Artorius

Great rate expectations

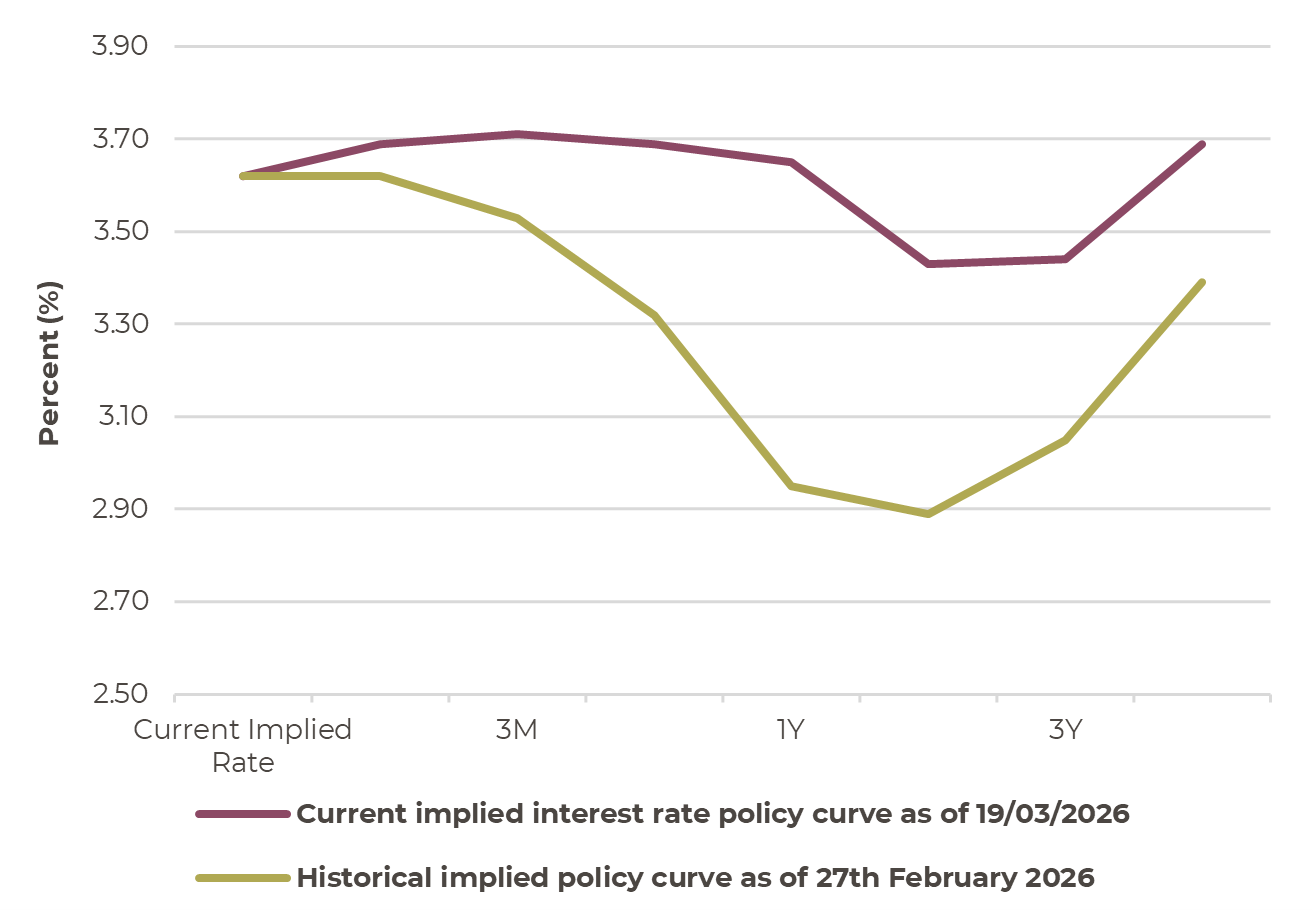

Higher oil prices have resulted in a change in interest rate expectations. At the end of February, i.e. just before the US-Israeli attack on Iran, investors were anticipating that US interest rates would be cut by about 0.6% through the remainder of 2026. As of the 19th of March, investors now expect US rates to be held at current rates through 2026, and then only slightly cut in 2027. This shift in expectations is shown in the chart below.

One interesting aspect of the interest rate backdrop in the US, is that the Federal Reserve is mandated to take into account the US labour market not just inflation. Unlike most central banks who just have an inflation target, the US central bank is required to strive for ‘maximum employment’ as part of their mandate. Given the backdrop of a cool labour market where jobs growth is sluggish and unemployment is rising, the Federal Reserve may choose to look through the inflationary impact of the oil price shock and cut interest rates if the US economy stumbles in coming months.

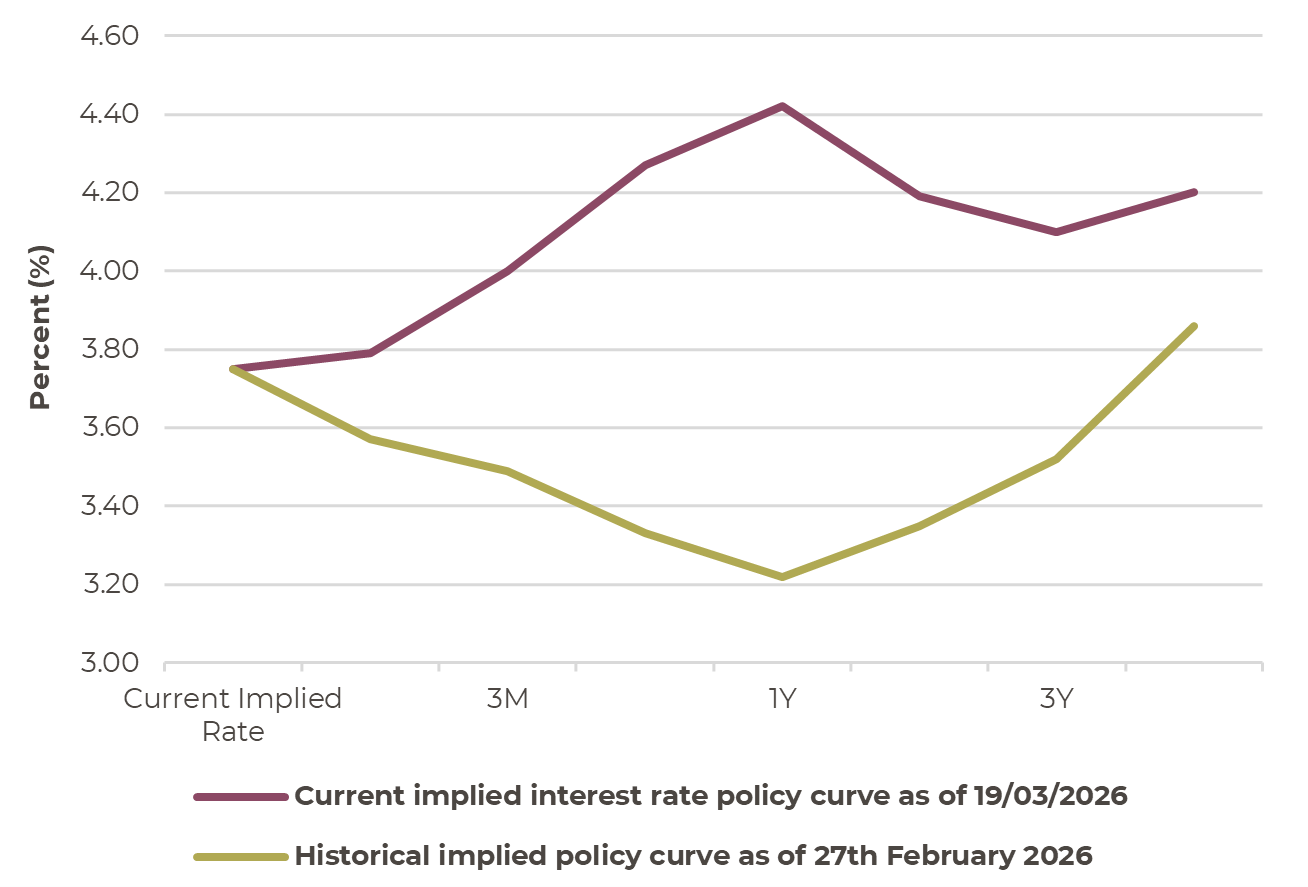

Investors have gone from expecting interest rate cuts in 2026 in the UK, to now pricing in a chance of higher interest rates by the start of 2027. This is already showing up in higher mortgage rates, which in turn is likely to slow down the recovery of the UK housing market that had been seen in recent months.

US interest rate expectations have shifted over the past 3 weeks. Fewer rate cuts are now anticipated by the market as shown by the implied policy interest rate curve shifting higher since the end of February 2026

Source: Bloomberg, Artorius

UK interest rate expectations have shifted over the past 3 weeks. Expectations of rate cuts are now anticipated by the market as shown by the implied policy interest rate curve shifting higher since the end of February 2026.

Source: Bloomberg, Artorius

How the central banks respond to higher inflation will determine if the oil induced inflation shock deepens into a more prolonged economic slowdown.

If oil prices fall back, inflation in Europe and Asia in 2026 would likely be only around 0.5 percentage points higher than pre-conflict forecasts. Under this scenario, central bank strategies would remain largely unchanged, and the impact on real economic growth would be minimal.

A more severe scenario in which the conflict persists for several months could see oil prices rise to around $130 per barrel before declining in the second half of the year. At a global level, the hit to growth would be modest, though the impact would be felt unevenly across regions. The euro-zone economy would probably contract in Q2 2026 and then flatline over the second half of the year.

The US economy would fare better but would nonetheless experience a slowdown in growth. Despite the weaker growth outlook, the accompanying rise in inflation would likely force central banks to shift policy. The Federal Reserve could abandon rate cuts while the European Central Bank could move to raise interest rates.

Recent history has been good

Ahead of the conflict, global economic conditions were improving. There was a noticeable improvement in business sentiment and the outlook for profits had been improving, and not just in the US. This benign backdrop has been challenged by oil prices climbing. The resilience of the equity markets in the face of the challenges of the war does seemingly betray a willingness of investors to look through the economic consequences of the war and hope that the economic progress of the past few months would resume.

Conclusion

The US-Israeli attacks on Iran interrupted the benign and improving backdrop seen at the start of 2026 and will have consequences for economies and investment markets.

It remains unclear what the objectives are and how military tensions can dissipate in the near term. Given the uncertainty we have sketched out a few scenarios based on possible outcomes and their consequences for oil prices, economies, interest rates and financial markets. Such scenario mapping frees us to think about different uncertainties rather than planning for any one particular eventuality.

There are scenarios that see a de-escalation of tensions, a fall in the oil price and a resumption of the global economic recovery, albeit a recovery that is likely to have stalled given the war. Each day that military threat restricts the flow of oil in the Strait of Hormuz and oil prices remain elevated and volatile, the risk builds of an economic slowdown. A downside scenario could result in a collapse of Iranian oil production, in the same way that Libyan oil production fell during the civil war, following the UK and France’s intervention (post the passing of the UN Security Council Resolution 1973). Iranian oil production is an important source of global energy and it would be a challenge to replace it over a prolonged period, which may give way to elevated oil prices.

Oil prices have increased by 57% since the end of February already resulting in higher petrol prices. Whilst the UK has higher petrol prices than the US, due to the high tax wedge in the petrol price, the rise of oil is having a larger immediate impact in the US where petrol prices have increased by 22% since the start of the war compared to ‘only’ 6.5% in the UK.

It is likely that the short-term effect of the war will show up in the inflation data. As a result, investors have shifted expectations for the path of interest rates in coming months. In the US, fewer rate cuts are now expected. In the UK, a few weeks ago markets had been pricing in rate cuts through the rest of 2026, but this has now changed to expectations that the Bank of England will raise interest rates. This is already transmitting itself into higher mortgage rates that in turn is likely to dampen the nascent recovery in activity that was building in the UK housing market.

While we wait for the news flow, there is so much we do not know, and what we think we know is subject to change at a moment’s notice.

*Any feedback provided can be anonymous

Important Information

Artorius provides this document in good faith and for information purposes only. All expressions of opinion reflect the judgment of Artorius at 20th March 2026 and are subject to change, without notice. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete; we do not accept any liability for any errors or omissions, nor for any actions taken based on its content.

The value of an investment and the income from it could go down as well as up. The return at the end of the investment period is not guaranteed and you may get back less than you originally invested. Past performance is not a reliable indicator of future results.

Nothing in this document is intended to be, or should be construed as, regulated advice. Reliance should not be placed on the information contained within this document when taking individual investment or strategic decisions.

Any advisory services we provide will be subject to a formal Engagement Letter signed by both parties. Any Investment Management services we provide will be subject to a formal Investment Management Agreement, which will include an agreed mandate.

Artorius Wealth Management Limited is authorised and regulated by the Financial Conduct Authority. Artorius is a trading name of Artorius Wealth Management Limited.

FP20260320001