Middle East conflict and interest rates: why energy markets now matter for policy expectations

Middle East conflict and interest rates: why energy markets now matter for policy expectations

The escalation of conflict in the Middle East has quickly become more than a geopolitical issue. While much remains uncertain, and what we believe we know can change at a moment’s notice, for financial markets the key question is how disruption to energy supply, particularly through the Strait of Hormuz, may affect inflation and, in turn, the outlook for interest rates in major developed economies.

Our recent note, War, Waterways and Wallets: Iran’s Geopolitical Shock, examined the immediate market response and the strategic importance of the Strait of Hormuz as a key global energy corridor. Rather than revisiting those dynamics, this article focuses on the broader effects on the global economy, and how the energy shock feeds through to monetary policy expectations.

The inflation channel

Higher oil and gas prices tend to push up headline inflation in most economies through fuel, transport and utility costs. That, in turn, can slow the pace at which inflation returns to central bank targets and make policymakers more cautious about cutting interest rates.

Before the escalation of the conflict, investors had generally expected the Federal Reserve, the Bank of England and the European Central Bank to continue easing monetary policy during 2026 as inflation pressures continued to subside. The increase in energy prices has made that path less certain.

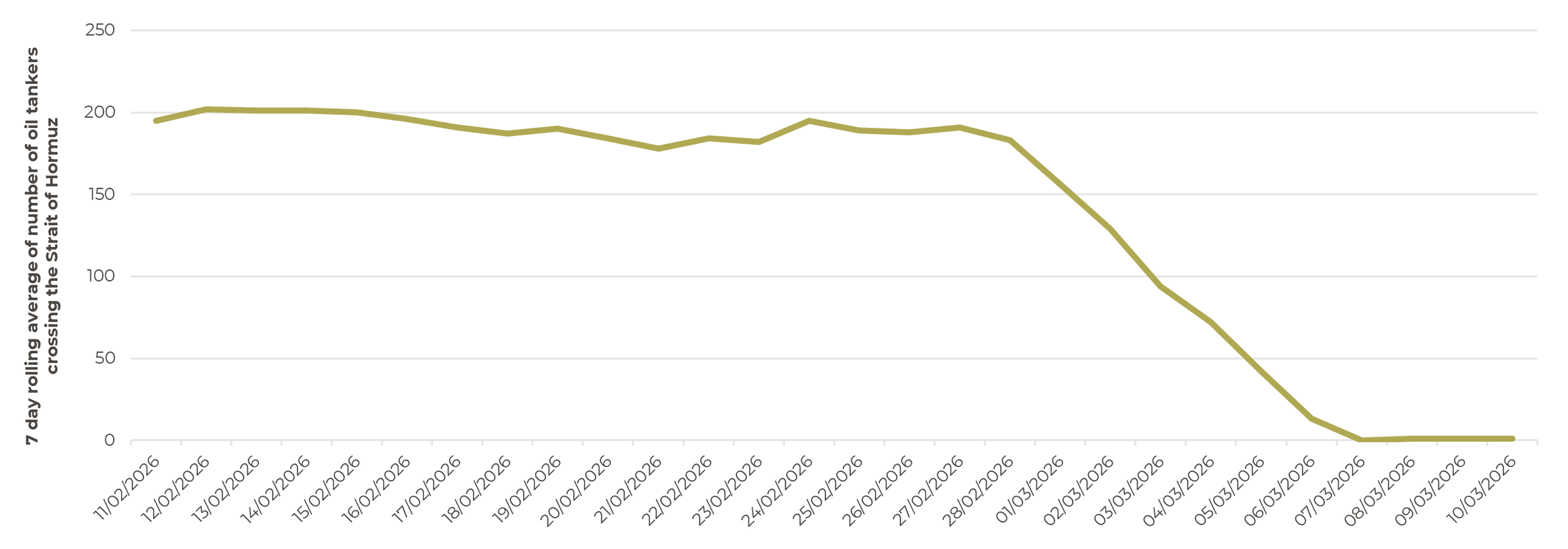

The number of oil tankers crossing the Strait of Hormuz has fallen to an average of one per day, down from around 200 a month earlier, highlighting the scale of the disruption

Source: Artorius, Bloomberg

If higher oil prices persist, central banks may need to maintain tighter policies for longer in order to ensure that inflation expectations remain under control. In such a scenario, interest rate cuts could be delayed or implemented more gradually than markets previously anticipated.

The degree of economic exposure varies across regions. The United States benefits from significant domestic energy production, which provides some insulation from global supply shocks. By contrast, both the United Kingdom and the eurozone remain more dependent on imported energy, making inflation in those economies particularly sensitive to changes in global oil and gas prices.

Nevertheless, in all three regions the central policy dilemma is the same: whether to look through what may prove to be a temporary energy-driven rise in inflation, or to maintain tighter monetary policy to prevent broader price pressures from becoming embedded in the economy.

Emerging markets face a more mixed picture. Energy exporters such as Brazil and Middle Eastern oil exporting economies, who are able to export oil still, may benefit from higher oil prices, which can support fiscal balances and strengthen economies. By contrast, energy-importing economies, particularly in parts of Asia and emerging Europe, may experience renewed inflationary pressure and weaker currencies, potentially forcing central banks to maintain tighter policy for longer. As a result, the impact of the current energy shock across emerging markets is likely to be uneven, reflecting differences in energy dependence, trade balances and monetary policy credibility.

Markets are adjusting to a more uncertain outlook

Financial markets have already begun adjusting to this uncertainty. Government bond yields in several developed economies have risen as investors reassessed the likelihood of near-term interest rate cuts. At the same time, equity markets have experienced greater volatility as investors attempt to price in both geopolitical risk and the potential macroeconomic consequences.

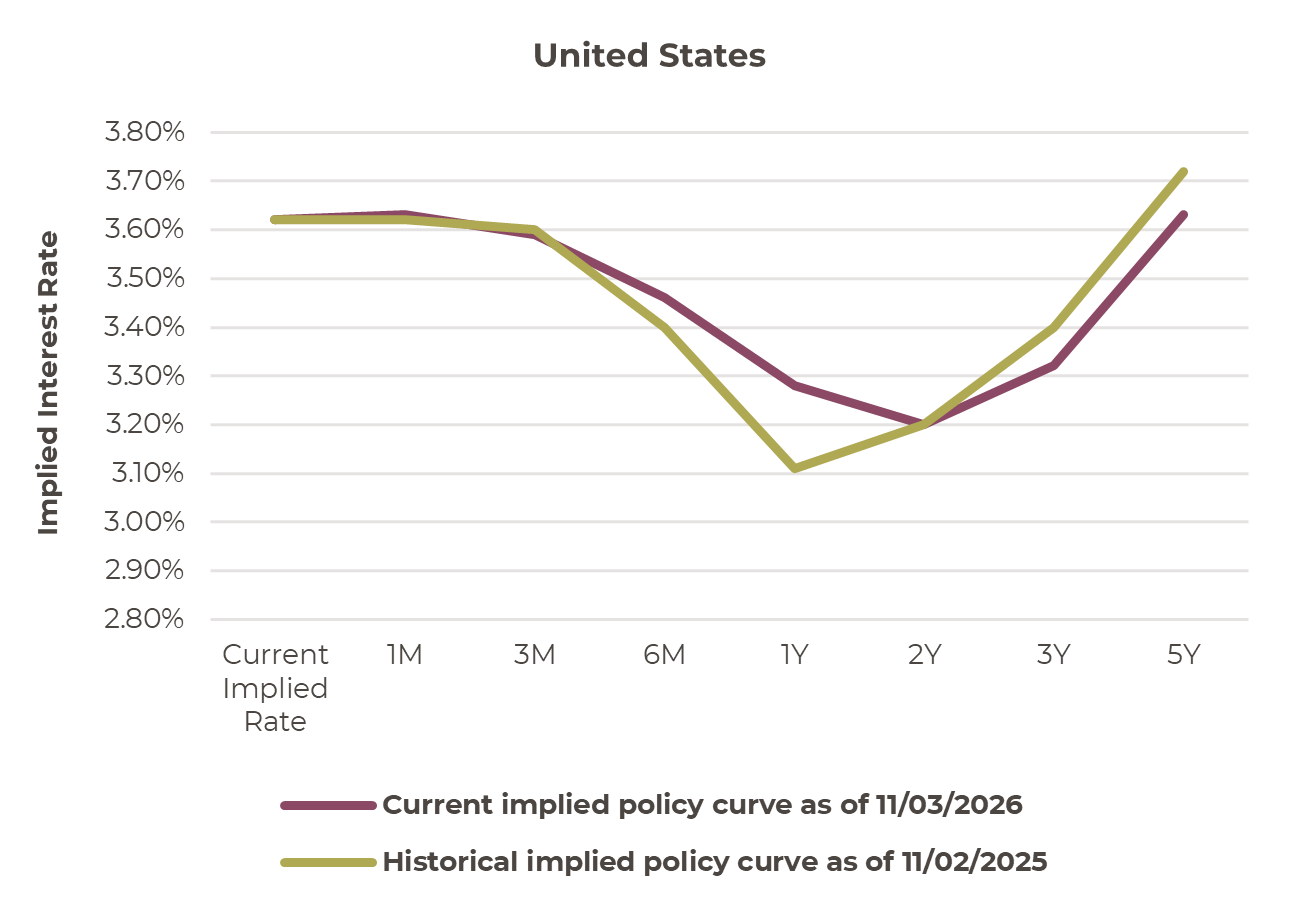

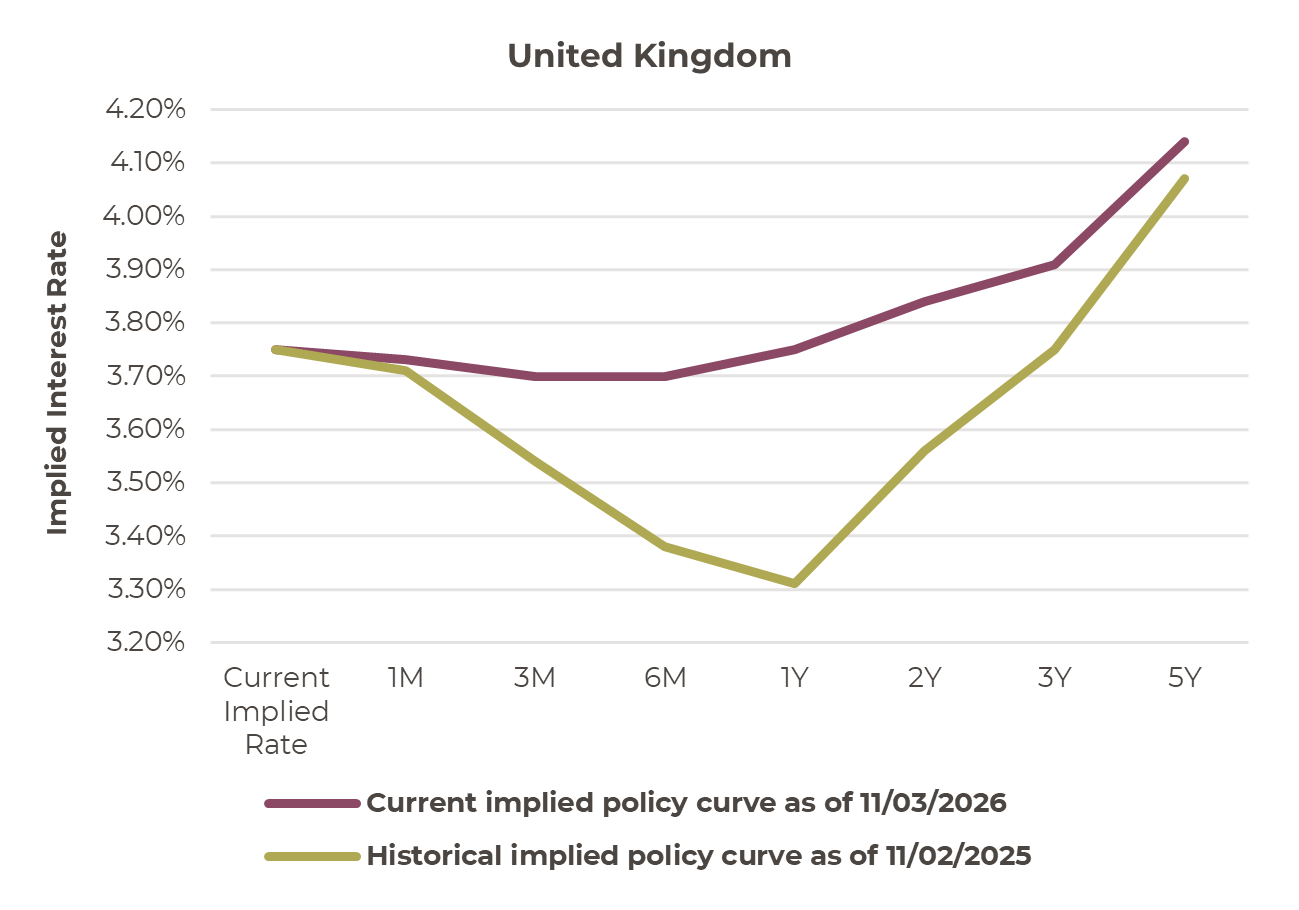

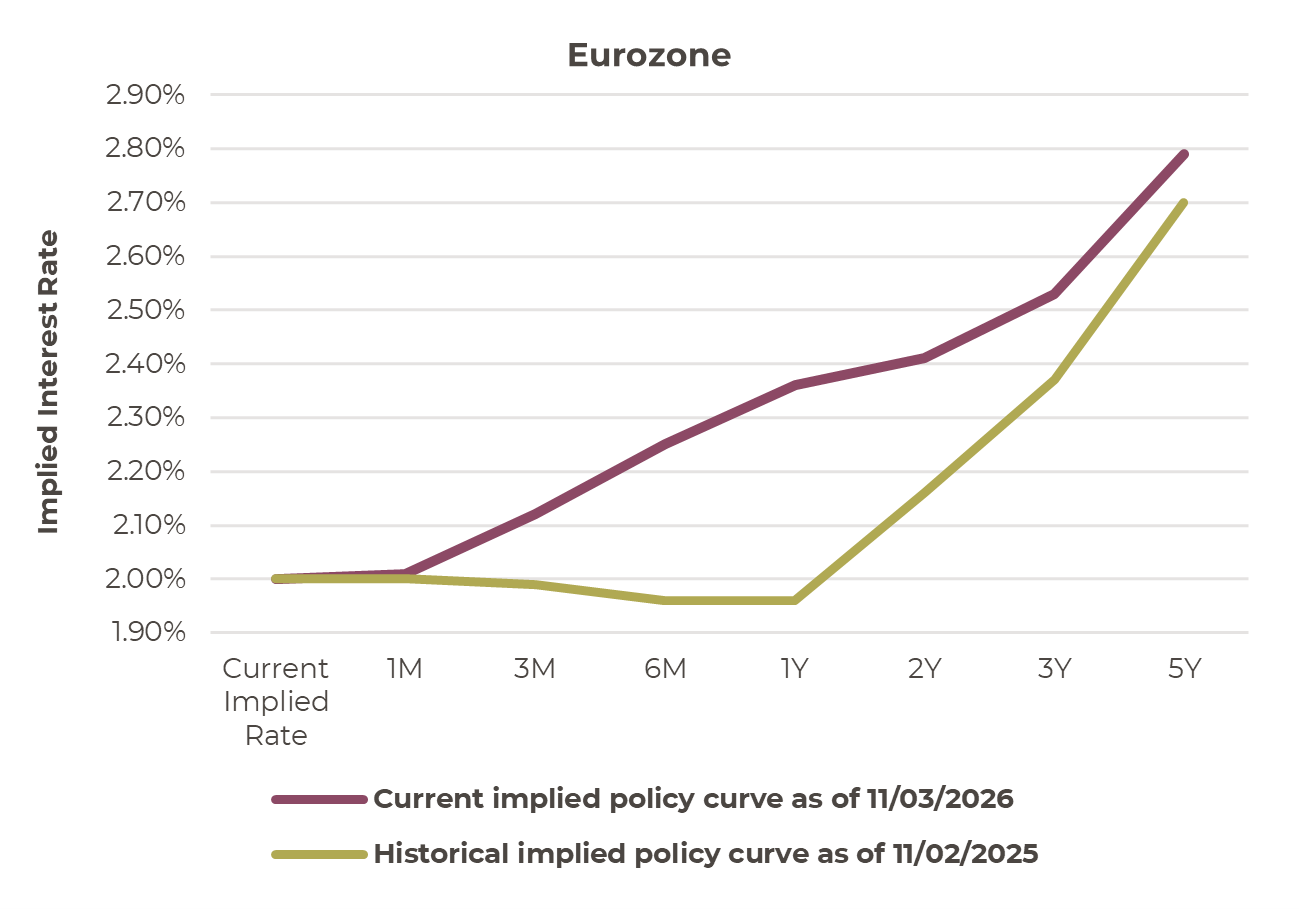

Interest rate expectations have risen over the past month, particularly in the UK and eurozone, reflecting increased market uncertainty

Source: Artorius, Bloomberg

The key variable now is duration. Geopolitical shocks often trigger short-term volatility but only produce lasting macroeconomic effects when they lead to sustained disruptions in energy supply.

If the current conflict stabilises and energy flows normalise, the impact on inflation and interest rate expectations may prove temporary. In that scenario, central banks could still move towards easing policy later in the year.

However, if supply disruptions persist, particularly if shipping through the Strait of Hormuz remains constrained, energy prices could remain elevated for longer. That would make the path back to central bank inflation targets more difficult and could delay interest rate cuts across several major economies.

What should investors watch?

For investors, the key indicators in the coming weeks and months will be:

developments in shipping and security in the Strait of Hormuz.

the trajectory of global oil and gas prices.

inflation expectations in major economies.

central bank commentary on energy-driven inflation risks.

While geopolitical events are inherently unpredictable, their economic effects are generally well understood. In this case, the link from conflict to energy markets, and from energy markets to inflation and monetary policy, is likely to remain central to the global economic outlook in the months ahead.

The key takeaway, as noted in the opening paragraph, is that while much remains uncertain, whatever we believe we know can change at a moment’s notice. This has been clearly illustrated by markets reacting sharply to events this week, with oil prices swinging from around $65 a barrel to $120 at the start of the conflict, before falling back to roughly $85 after Donald Trump announced that the war would soon be over, and then rising back above $100 as hopes of an abrupt end faded. Such volatility underlines how quickly sentiment can shift and highlights the difficulty of forming firm expectations while the geopolitical situation remains fluid. In periods of uncertainty like this, investors are often better served by avoiding reactive decisions and maintaining a long-term perspective until the outlook becomes clearer.

Josh Young de Ferrer

Portfolio Manager

*Any feedback provided can be anonymous

Important Information

All expressions of opinion reflect the judgment of Artorius at 13th March 2026 and are subject to change, without notice. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete; we do not accept any liability for any errors or omissions, nor for any actions taken based on its content. The value of an investment and the income from it could go down as well as up. The return at the end of the investment period is not guaranteed and you may get back less than you originally invested. Past performance is not a reliable indicator of future results. Nothing in this document is intended to be, or should be construed as, regulated advice. Artorius provides this document in good faith and for information purposes only. Reliance should not be placed on the information contained within this document when taking individual investments or strategic decisions.

Artorius Wealth Management Limited is authorised and regulated by the Financial Conduct Authority. Artorius is a trading name of Artorius Wealth Management Limited.

FP20260313001