War, Waterways and Wallets: Iran’s Geopolitical Shock

War, Waterways and Wallets:

Iran’s Geopolitical Shock

The attack on Iran by Israel and the US has created a moment of regime uncertainty in Iran. The geopolitical implications are profound, but for markets the calculus may be much simpler: will the war disrupt oil and gas supply and economies in a sustained way?

Most geopolitical shocks that proved brief, or where supply was quickly stabilised, tended to create volatility rather than lasting damage. The template appears to not be conflict itself but the duration and transmission. However, history offers one true outlier. The Yom Kippur War in 1973 triggered a deep and protracted equity and bond bear market because it led to a meaningful, extended reduction in global oil supply due to an embargo by the Organization of Arab Petroleum Exporting Countries (OAPEC).

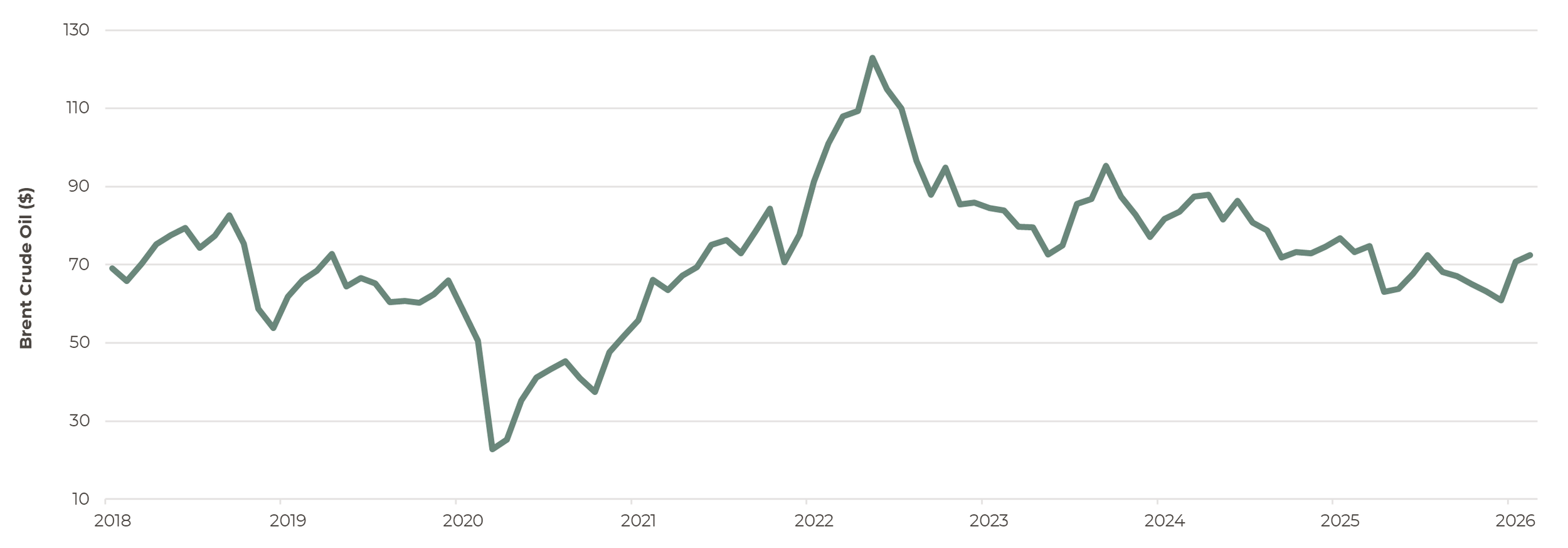

Brent crude oil prices increased by roughly 12.5% as markets reopened at the beginning of this week. The move appears to reflect a rational repricing of risk rather than panic. Oil is higher whilst disruption is plausible; it is not yet pricing in a lasting supply shock.

Brent takes an upwards turn

Source: Artorius, Bloomberg

Pricing the passage

The critical focal point remains the Strait of Hormuz, through which around 20% of global oil exports transit. As the economist Herbert Marleau of Palos Management stated, a full closure would constitute a potential negative risk event, potentially driving Brent towards $120-125 per barrel. A rapid stabilisation or regime transition could see prices retrace towards $60. However, another scenario is continued tension: shipping under threat, constrained insurance, incremental output increases from the Organization of the Petroleum Exporting Countries Plus (OPEC+), and oil potentially peaking upwards of $80.

Importantly, the current constraint appears to be commercial rather than physical, which is causing investors to be more cautious. Insurers issued cancellation notices within hours of the initial strikes, effectively freezing shipping irrespective of a formal blockade. In other words, markets are being tightened by insurance and financing constraints before any physical disruption. That distinction matters and regional equity markets underline the point.

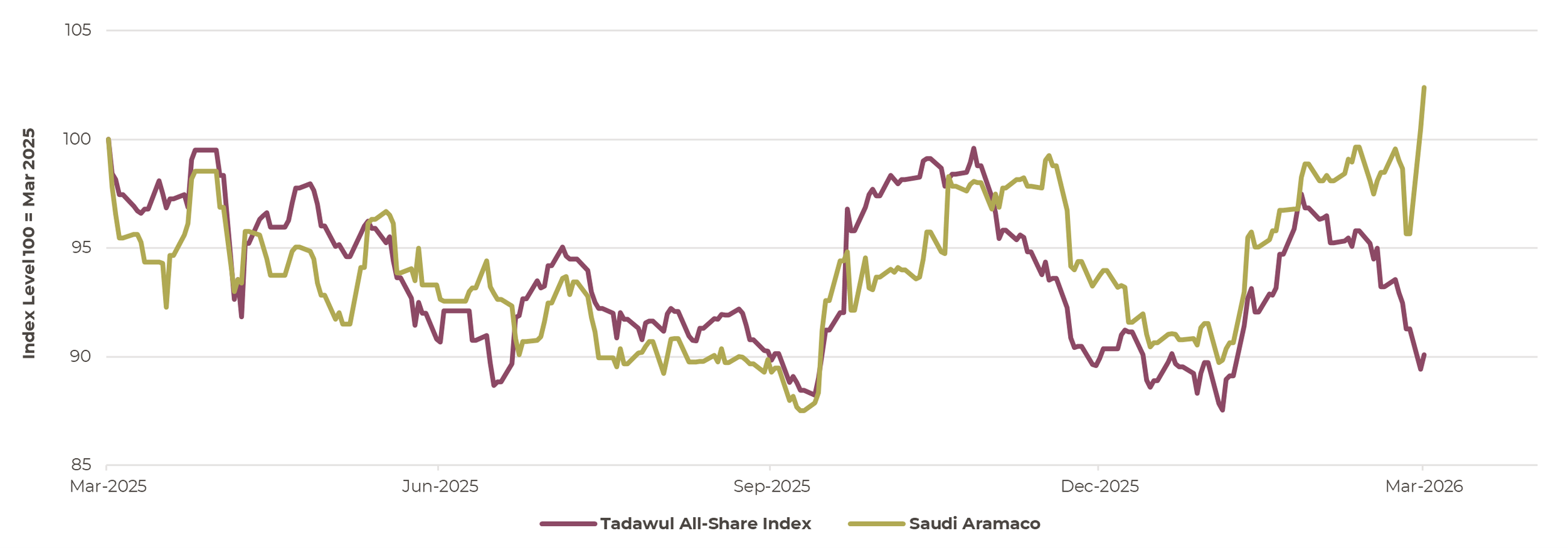

In Saudi Arabia, Saudi Aramco (the Saudi Arabian oil company) rallied strongly on the prospect of higher oil prices, yet the broader Tadawul index (leading stock market index in Saudi Arabia) fell sharply. Energy earnings optimism appears to have been overwhelmed by systemic concern.

Barrels Up, Broader Market Down

Source: Artorius, Bloomberg

Looking into the past…

Similarities with the 1979 Iranian Revolution may be drawn by investors. At the time this triggered an enormous surge in oil prices, not because Iran dominated production, but because fears spread across the region and speculative hoarding intensified as markets anticipated broader disruption. The lesson is that contagion, not just direct supply loss, can drive sustained price spikes.

Today, the global economy is less oil-intensive than it was in the late 1970s. Major economies use materially less oil per unit of Gross Domestic Product (GDP), vehicle efficiency has improved markedly, and natural gas and renewables have displaced oil in several applications.

Vulnerability to oil disruptions, 1978 to Now

| 1978 | Now | |

|---|---|---|

| Middle East as % of world oil production | 34.3 | 31.0 |

| Iran as % of world oil production | 8.5 | 5.2 |

| US as % of world oil production | 15.6 | 18.9 |

| US Consumer Price Index | 7.4 | 3.0 |

| US S&P 500 Price/Earnings ratio | 8.3 | 30.7 |

Sources: Artorius, Bloomberg, Oil production: Energy Institute - Statistical Review of World Energy (2025); The Shift Data Portal (2019) – with major processing by Our World in Data, Federal Reserve Bank of Atlanta, Sticky Price Consumer Price Index less Food and Energy [CORESTICKM159SFRBATL], retrieved from FRED, Federal Reserve Bank of St. Louis.

What lies ahead?

So where does this leave markets? For now, there appears to be a repricing of risk rather than a fundamental market shift. Oil hovering around $80 in the short term is a reasonable assumption given disrupted shipping and shipping insurance withdrawal. A further sustained rally would likely require escalation that materially disrupts regional exports. Equity markets may warrant a somewhat higher geopolitical risk premium, but presence of improving earnings momentum may limit immediate downside.

In essence, 1973 was about supply shock; 1979 was about inflation psychology. Today’s backdrop is structurally different: economies are more diversified, central banks are more attuned to inflation credibility, and energy intensity has declined. Yet interconnected supply chains and capital markets mean disturbances are transmitted rapidly, often through sentiment and positioning. The AI-driven investment cycle adds a further dimension - it is both seen as a potential source of resilience through productivity gains and a possible amplifier of volatility should confidence in the growth narrative wobble.

The narrow passage of Hormuz remains the fulcrum. As long as flows are threatened but not severed, volatility is likely to persist without necessarily morphing into a full-scale bear market. As Howard Marks, co-founder of Oaktree Capital, recently cautioned, “The main thing to consider is how much we don’t know, because we don’t understand the significance of what’s happening; there’s probably nothing sensible that can be done right now.” In other words, when outcomes remain uncertain, acknowledging risk without overreacting to it can be the most rational response.

Mark Christie

Investment Analyst

*Any feedback provided can be anonymous

Important Information

All expressions of opinion reflect the judgment of Artorius at 6th March 2026 and are subject to change, without notice. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete; we do not accept any liability for any errors or omissions, nor for any actions taken based on its content. The value of an investment and the income from it could go down as well as up. The return at the end of the investment period is not guaranteed and you may get back less than you originally invested. Past performance is not a reliable indicator of future results. Nothing in this document is intended to be, or should be construed as, regulated advice. Artorius provides this document in good faith and for information purposes only. Reliance should not be placed on the information contained within this document when taking individual investments or strategic decisions.

Artorius Wealth Management Limited is authorised and regulated by the Financial Conduct Authority. Artorius is a trading name of Artorius Wealth Management Limited.

FP20260306001