The Solow Productivity Paradox

The Solow Productivity Paradox

Investors, and even avid readers of our investment comments may be forgiven for not wanting to read about artificial intelligence (AI) anymore. However, since the launch of ChatGPT in November 2022, the weight of “AI Companies” in the S&P 500 has grown from approximately 25% to 45% today. When the concentration is at such elevated levels, the need for fresh and more pertinent ways of thinking about AI as an economic and investment phenomenon remains key.

As an economics graduate, I am always drawn to economic theories that can help explain market activity and provide perspective on the trajectory of specific industries, such as our note on Amara’s Law. One such framework is the Solow productivity model, which, despite its age, offers a useful lens through which to assess both the possibilities and the uncertainty surrounding AI-driven growth.

The Solow Productivity Paradox

In 1987, the Nobel Prize-winning economist Robert Solow said, “You can see the computer age everywhere but in the productivity statistics”, coining what became known as the productivity paradox. This paradox arose at a time of rapid technological progress, when innovations such as personal computers and mainframes were reshaping workforces, yet productivity growth remained subdued.

The same observations could made today: AI appears widespread in headlines, boardrooms and capital expenditure plans, yet it is notably absent from macroeconomic data such as employment, productivity or inflation data. Likewise, across the S&P 493 (excluding the seven largest mega-cap technology stocks), there is little evidence of AI filtering through into profit margins or forward earnings expectations. Recent data from Goldman Sachs shows that approximately 70% of S&P 500 firms mention AI broadly, but just 1% have quantified the impact of AI on earnings figures.

Earlier this month, we wrote about the market sell-off in software stocks as companies such as Anthropic and their workflow automation plugin ‘Claude Cowork’ spooked investors about the future profit margins of software companies and whether AI companies could easily eat into their margins. The market consensus is that software engineers will slowly be displaced by AI. And yet, despite the current displacement narrative, recent data has shown job postings for software engineers are rising rapidly - up 11% year on year.

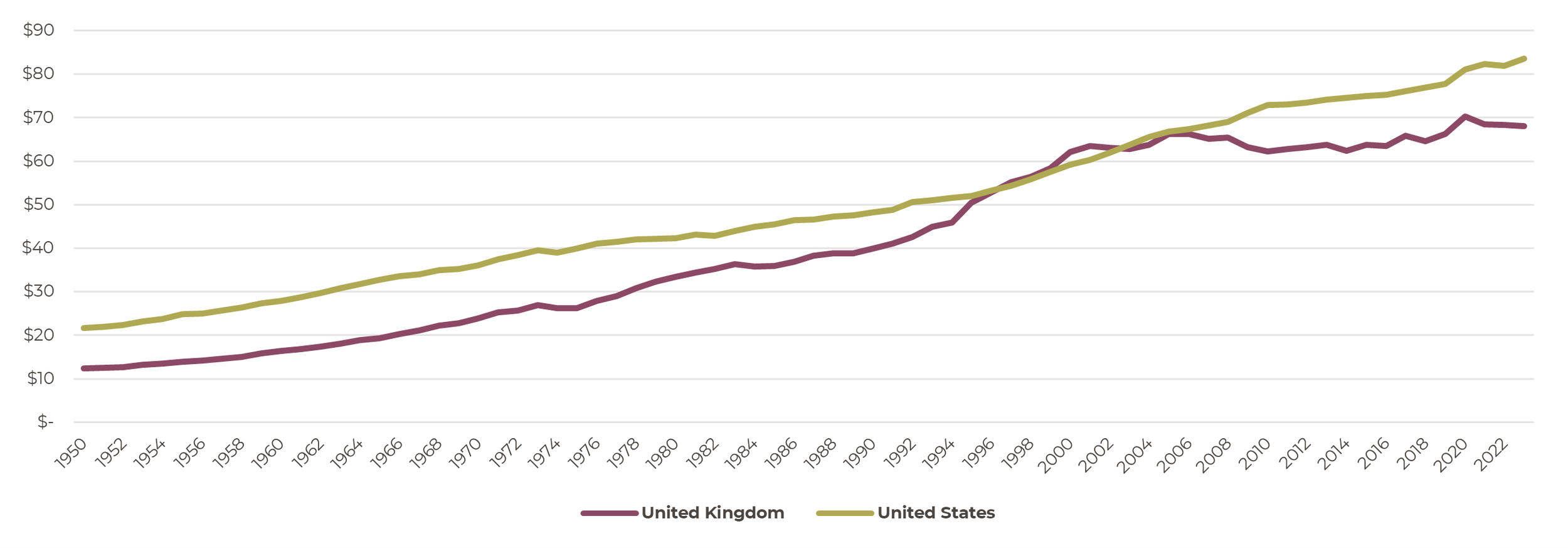

There are many ways to measure productivity. The most widely used metric is ‘output per hour worked’. This measures gross domestic product (GDP) per hour of work. The chart below shows data sets for the United States and United Kingdom and is adjusted for inflation and differences in living costs between countries, displayed in US dollars.

Productivity: output per hour worked

Source: Data Page: Productivity: output per hour worked”, part of the following publication: Max Roser, Bertha Rohenkohl, Pablo Arriagada, Joe Hasell, Hannah Ritchie, and Esteban Ortiz-Ospina (2023) - “Economic Growth”. Data adapted from Feenstra et.al. Retrieved from https://archive.ourworldindata.org/20251013-111729/grapher/labor-productivity-per-hour-pennworldtable.html

The first observation is that the Solow productivity paradox can be seen in full effect in the US. The emergence of businesses using computers that began in the 1950s to widespread internet adoption in the early 1990s did not lead to any significant pick up in the productivity numbers. Productivity continued to rise as computers became a main stay in businesses during the 1960s and 70s, but this was in-line with the previous trend seen.

The UK experienced a notable productivity surge from the mid-1990s, largely driven by structural reforms rather than technology. Key factors included the 1986 ‘Big Bang’ deregulation of London’s financial markets, increased foreign direct investment, labour market reforms that improved flexibility, and the rapid expansion of the service sector. These changes created a more competitive and efficient environment, enabling firms to increase output and productivity.

After the 2008 global financial crisis, UK productivity stagnated, while in the US, the recession had little visible effect on productivity trends. US firms continued to invest heavily in digital technologies and productivity-enhancing systems, supported by a flexible labour market that enabled efficient reallocation. By contrast, the UK faced financial austerity, under-investment, and ongoing structural constraints, which slowed productivity growth despite technological progress.

The AI J-curve

It is possible that AI will follow a J-curve dynamic, whereby the upfront investment, disruption and adjustment cost precedes any visible improvement in macroeconomic data. Ultimately, this will depend on where value accrues within the AI ecosystem. At present, there is intense competition among developers of large language models (LLM), which is pushing the marginal cost of access towards zero for end-users. This runs counter to the traditional textbook assumption that an innovator enjoys a period of monopoly pricing power before competitors replicate the product. During the computer age of the 1980s, for example, early movers were typically able to secure a strong competitive advantage before their products became widely available.

From a macroeconomic perspective, this distinction matters. The primary value creation may not lie in the models themselves, but in how generative AI is applied, integrated and scaled across different sectors of the economy. The academic literature remains inconclusive regarding the aggregative impact, with estimated annual gains in annual productivity ranging from as low as 0.07% to over 1% in the short run, and cumulative gains over 10-20 years spanning from under 1% to as much as 12%.

There are a lot of unanswered questions about how the economic adjustment will play out. Unlike past general-purpose technologies, which took decades to diffuse, AI use is spreading fast, and AI is still a relatively new technology. The launch of LLMs took place in 2022 and business adoption started to take meaningful shape in 2025. Whether AI will primarily be a substitute or a complement for labour and who the main beneficiaries will be is still difficult to forecast. Will this lead to a meaningful shift in the productivity frontier and change the way modern business is conducted for the rest of our lives? Or will much of the value AI creates accrue primarily to the capital holders and not the workers. Time will tell.

In other news

Nvidia’s Q4 fiscal 2026 results were released on 25 February 2026, marking its 14th consecutive quarter of results that exceeded analyst estimates. Revenue growth was again driven primarily by its data‑centre segment, reflecting continued demand for the computing power required to train and operate large AI models at scale. However, despite the positive earnings print, Nvidia’s share price fell about 5 % on the following trading session, suggesting that a significant portion of the AI‑driven optimism may already be priced in. Nvidia’s performance illustrates an important distinction within the AI narrative: while macroeconomic productivity data may not yet show a clear uplift, value is clearly accruing at specific nodes of the AI supply chain — particularly among providers of critical computing infrastructure.

In many ways, this mirrors the dynamic highlighted by Solow. Technological revolutions may first be evident in corporate earnings, capital expenditure cycles, and market concentration, long before they register meaningfully in aggregate productivity statistics. The computer age was visible in equity markets and balance sheets before it appeared in national accounts; AI may prove no different.

At the end of last week, the US Supreme Court ruled that the ‘Liberation Day’ tariffs introduced by President Trump in April 2025 were illegal, stating that the president had overstepped his authority under the International Emergency Economic Powers Act. In response, Trump quickly replaced them with a new tariff regime, initially announcing a global 10% duty and later increasing it to 15%. These are seen as temporary and can last only up to 150 days; anything beyond that would require Congressional approval. Equity markets largely shrugged at the news, showing little reaction. Uncertainty remains over whether previously collected tariffs will be reimbursed, how the new framework will be implemented, and the potential impact on corporate margins and supply chains.

Yuval Peshchanitsky

Portfolio Analyst

*Any feedback provided can be anonymous

Important Information

All expressions of opinion reflect the judgment of Artorius at 27th February 2026 and are subject to change, without notice. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete; we do not accept any liability for any errors or omissions, nor for any actions taken based on its content. The value of an investment and the income from it could go down as well as up. The return at the end of the investment period is not guaranteed and you may get back less than you originally invested. Past performance is not a reliable indicator of future results. Nothing in this document is intended to be, or should be construed as, regulated advice. Artorius provides this document in good faith and for information purposes only. Reliance should not be placed on the information contained within this document when taking individual investments or strategic decisions.

Artorius Wealth Management Limited is authorised and regulated by the Financial Conduct Authority. Artorius is a trading name of Artorius Wealth Management Limited.

FP20260227001