Can We Get A Strait Answer?

Can we get a Strait answer?

Financial markets have entered a regime where geopolitics, energy, and macroeconomic policy are no longer separable - and the result is fierce, narrative-driven repricing. Monday’s trading session illustrated this perfectly: bond yields surged to post-2008 highs before reversing sharply on claims of President Trump having negotiations with Iran to stop the ongoing conflict in the Middle East.

Nowhere is this more evident than in interest rates. UK gilt yields have climbed aggressively, with the 10-year gilt yield breaching 5% at the start of the week, reflecting a dramatic shift in expectations. Markets that had been pricing in interest rate cuts are now anticipating multiple increases as energy-driven inflation feeds through. The speed of this adjustment highlights a deeper fragility.

UK 10-year gilts are yielding to the times

Source: Artorius, Bloomberg

Energy on the edge

Beyond the immediate market impact, the deeper concern lies in how long the energy supply shock will last and the potential for ongoing inflation. Reuters reported that the recent strikes on Qatar’s Ras Laffan liquefied natural gas (LNG) complex have taken roughly 17% of the country’s LNG export capacity offline, with repairs expected to take between three and five years - turning what markets initially treated as a temporary disruption into a prolonged structural supply issue.

The Strait of Hormuz is not merely an oil chokepoint; it is a critical artery for a wide range of inputs including LNG, fertilisers, helium, and pharmaceuticals. While oil prices have moved significantly, there have been even larger price moves in refined products, such as petrol and diesel, which means the impact will be felt more directly by consumers and businesses. Higher fuel and energy costs will feed through quickly into transport, heating, and production expenses, squeezing household budgets and compressing profit margins across sectors.

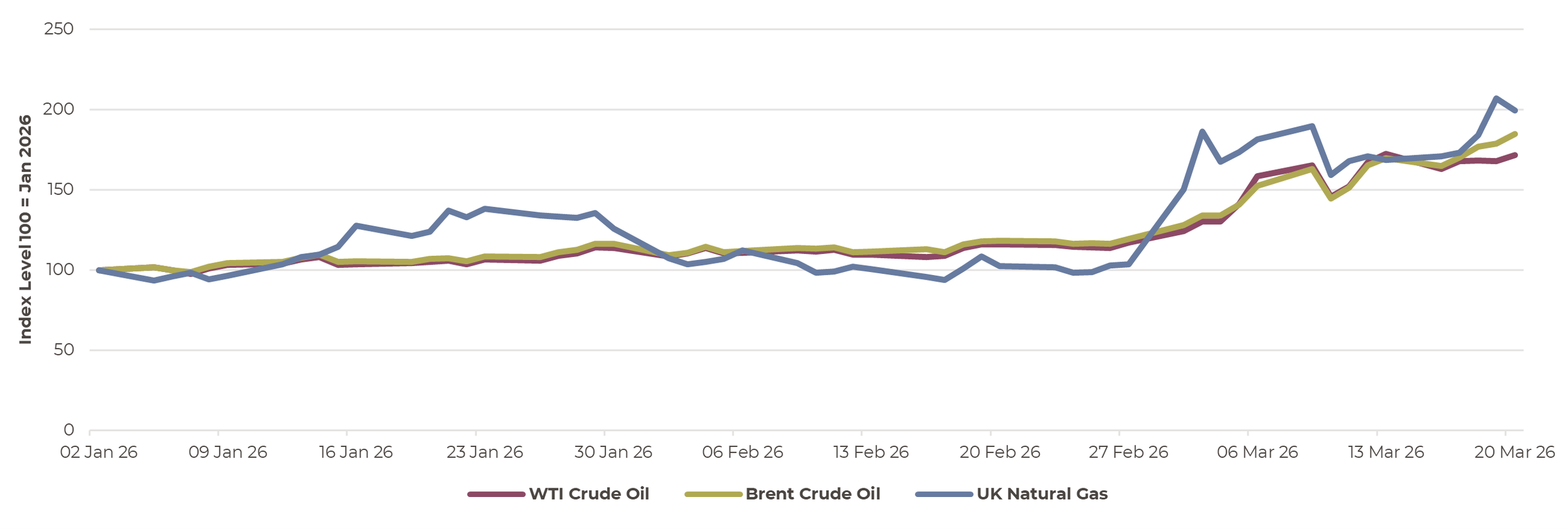

In the below graph, the slight premium of Brent Crude oil over West Texas Intermediate (WTI) Crude oil largely reflects geography and geopolitics. Brent is a seaborne, global benchmark that is far more exposed to disruptions in Middle Eastern shipping routes like the Strait of Hormuz, whereas WTI is more tied to inland US production and inventories. As tensions escalate and tanker traffic through Hormuz is curtailed, a ‘fear premium’ is increasingly priced into Brent.

In contrast, the sharper recent rise in UK natural gas reflects Europe’s acute dependence on imported LNG, a significant portion of which transits the same chokepoint; disruptions have already driven gas prices sharply higher due to immediate supply concerns and limited short-term substitutes.

Oil and natural gas rise amid geopolitical conflict

Source: Artorius, Bloomberg

When everything moves, where do you go?

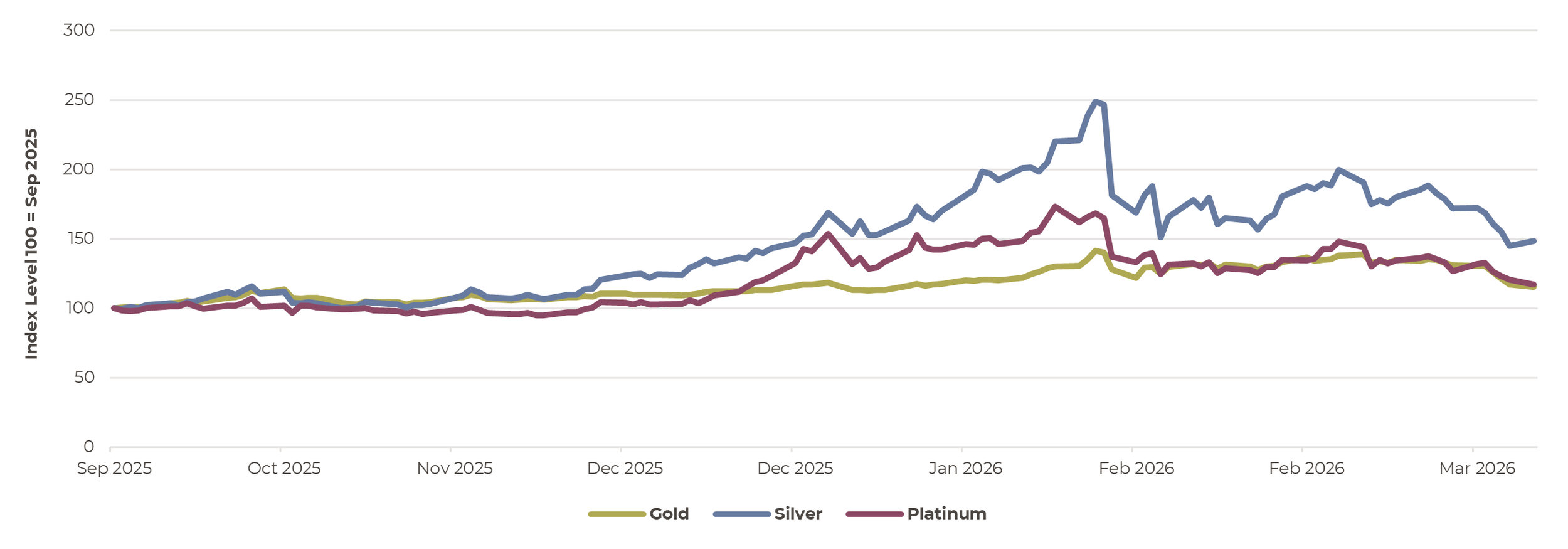

At the same time, traditional market relationships are breaking down. Gold, platinum, and silver, typically beneficiaries of geopolitical stress, have declined sharply since the start of the conflict. One potential driver is the rise in bond yields, which is outweighing safe-haven demand. When bond yields rise gold becomes less attractive because it doesn’t generate income.

Over recent months, investors had increasingly crowded into precious metals, driven by lingering concerns about inflation, government deficits and broader geopolitical uncertainty. During the crisis, investors have taken profits on gold positions and as speculative investors sell their positions prices have fallen sharply.

The precious retreat

Source: Artorius, Bloomberg

The price of conflict

Recent developments point to a market still searching for balance, but with few signs of resolution. While there has been a modest pick-up in tanker flows through the Strait of Hormuz towards India, it is insufficient to offset the broader disruption in global energy supply.

In response to the ongoing Middle Eastern war, the UK is more likely to focus on trying to cushion the impact on households and businesses, for example through energy price caps or targeted fiscal support, as seen following Russia’s invasion of Ukraine. Measures aimed at increasing domestic energy production, such as increasing North Sea oil and gas production, may appear attractive on paper, particularly if paired with windfall taxes and continued green investment. However, practical constraints mean any meaningful boost to supply would be slow to materialise and unlikely to have a significant impact on energy prices or the broader economic environment in the near term.

Beyond the domestic response, the geopolitical ramifications are becoming increasingly pronounced. Higher energy prices are providing a significant boost to Russia’s fiscal position, effectively easing the pressure created by sanctions, particularly as some restrictions are incrementally eased. These dynamics are further compounded by a diversion of Western military resources towards the Middle East, reducing the availability of equipment and support for Ukraine. What had looked like increasing pressure on Russia has, at least temporarily, been reversed and will increase its capacity to sustain the war in Ukraine.

Looking ahead, there are three key variables that will determine the outcome:

The extent and duration of disruption to energy supply will determine whether current price pressures become entrenched.

Central bank reactions will be critical in shaping market expectations, particularly in how they balance controlling inflation against growth risks.

Any evidence of broader supply chain disruption will signal a shift from price volatility to real economic damage.

In this environment, short-term relief rallies driven by headlines should not be mistaken for resolution. The underlying dynamics are tight energy markets, fragile supply chains, and constrained policy responses, which remain firmly in place. In response, we have reallocated our exposure, slightly moving out of European equities into short-dated government bonds to derisk portfolios and reduce sensitivity to headline-driven volatility.

Mark Christie

Investment Analyst

*Any feedback provided can be anonymous

Important Information

All expressions of opinion reflect the judgment of Artorius at 27th March 2026 and are subject to change, without notice. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete; we do not accept any liability for any errors or omissions, nor for any actions taken based on its content. The value of an investment and the income from it could go down as well as up. The return at the end of the investment period is not guaranteed and you may get back less than you originally invested. Past performance is not a reliable indicator of future results. Nothing in this document is intended to be, or should be construed as, regulated advice. Artorius provides this document in good faith and for information purposes only. Reliance should not be placed on the information contained within this document when taking individual investments or strategic decisions.

Artorius Wealth Management Limited is authorised and regulated by the Financial Conduct Authority. Artorius is a trading name of Artorius Wealth Management Limited.

FP20260327001