Relief all round but for how long?

Relief all round but for how long?

To describe this as an eventful week would be a significant understatement. President Trump set a deadline of 8pm Eastern Time (US) on Tuesday, 7th April, for Iran to reopen the Strait of Hormuz. He warned that, if no agreement was reached, “a whole civilization will die tonight” — a stark escalation in rhetoric.

Positively, Trump did not follow through on that threat. Less than two hours before the deadline, he announced on Truth Social that a two-week ceasefire had been agreed, contingent on the immediate and safe reopening of the Strait of Hormuz. The pause is intended to create space for negotiations based on a ten-point proposal put forward by Iran. Trump’s announcement triggered an immediate and sizeable positive reaction from oil, bond and equity markets.

A positive market response starting with the energy market

There has been significant market volatility since the start of the US–Iran conflict. As noted in previous Investment Comments, the closure of the Strait of Hormuz has restricted the flow of key energy products such as oil, liquefied natural gas (LNG), and refined fuels. It has also disrupted the supply of fertiliser and other petrochemicals used in the production of plastics. Less obvious, but also important, is the adverse impact on helium supply, which is used in MRI scanners and semiconductor manufacturing.

Sustained higher energy prices have both short-term and longer-term negative consequences for economic growth. The extent of the impact depends on the scale of the price increase and the length of time prices remain elevated. The longer prices stay high, the greater the drag on economic growth.

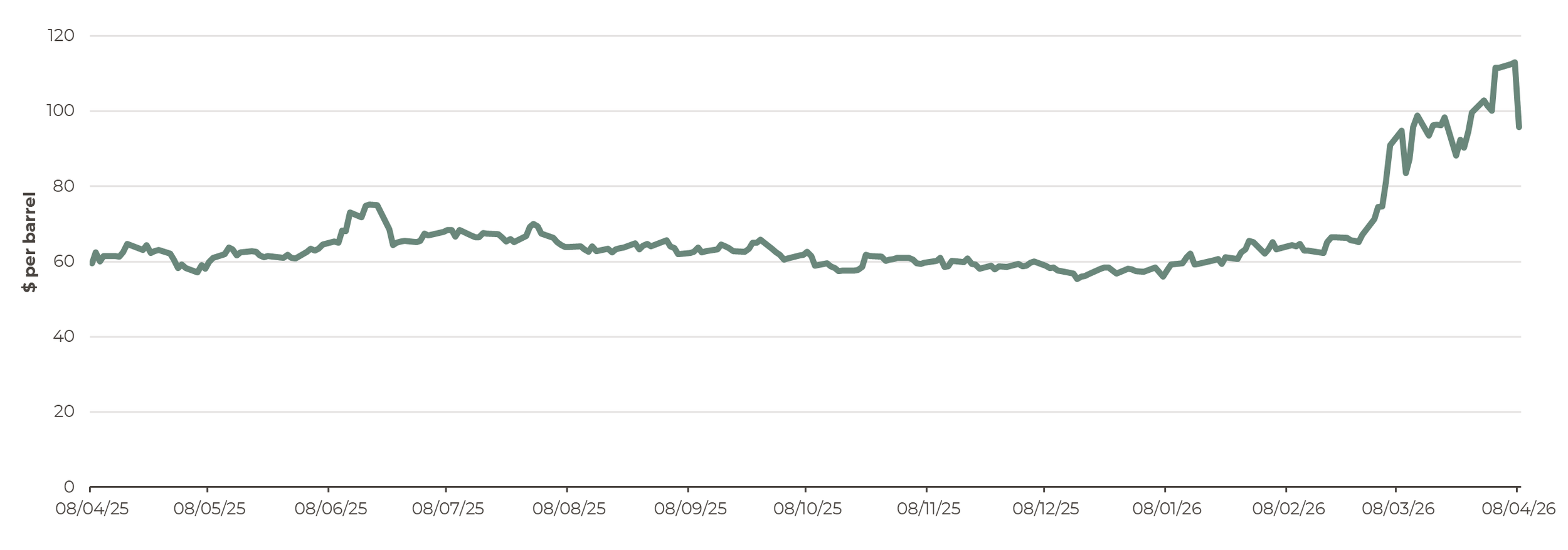

The market response to the ceasefire announcement on the 7th April was particularly notable in energy prices. As shown in the chart below, the oil price rose significantly following the outbreak of the war at the end of February. As it increasingly appeared that there was no clear path for the US to exit the conflict while securing the reopening of the Strait of Hormuz, oil prices continued to climb. However, the announcement of the ceasefire prompted a sharp decline of more than 10%, with West Texas Intermediate, the main U.S. oil benchmark, falling from $112.95 a barrel to $95.76.

West Texas Intermediate oil price

Source: Artorius, Bloomberg

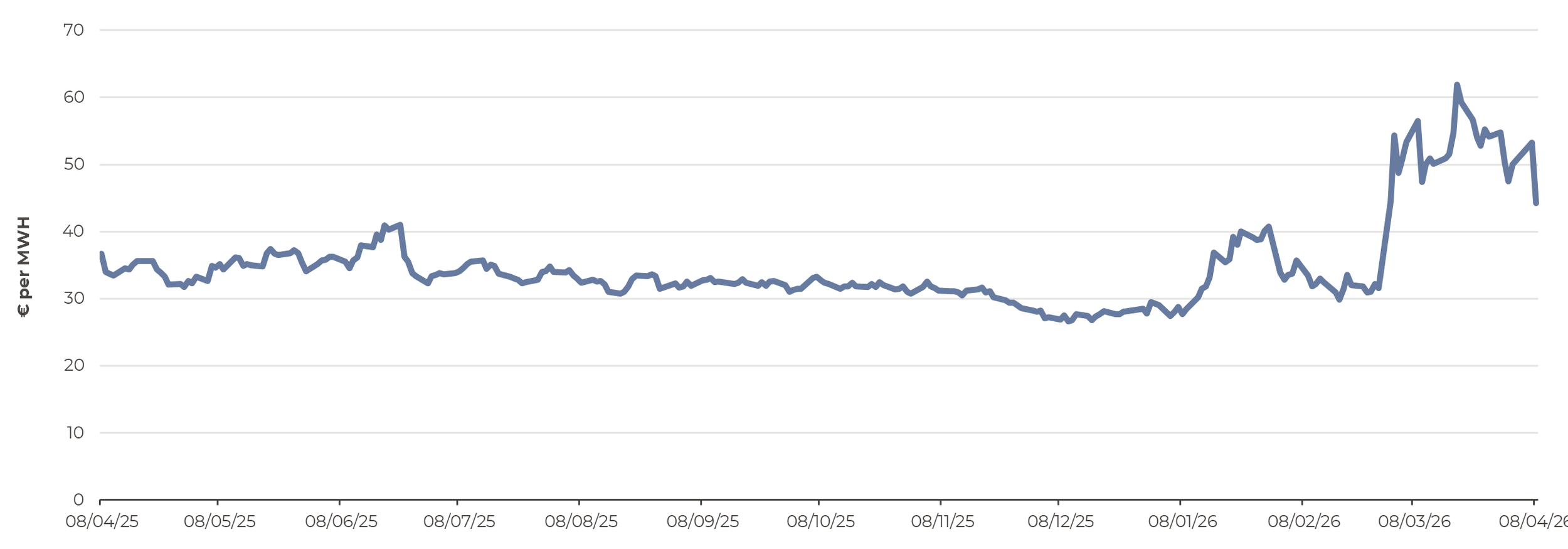

The relief in energy prices was not limited to oil. As shown in the chart below, natural gas prices also declined sharply.

European natural gas price

Source: Artorius, Bloomberg

Energy prices not back at pre-war levels

While the double-digit decline in energy prices is welcome news, it is notable that prices remain well above pre-war levels. Looking at oil, for example, the trend in the months leading up to the war showed prices broadly ranging between $60 and $70 per barrel. As a result, even after falling to $95 per barrel, prices remain approximately 35% above the top of that range. Natural gas prices have followed a similar pattern.

What does this mean in practice? In the short term, it suggests that energy inflation will remain a significant issue for most economies. This is likely to erode household budgets and influence corporate decision-making, including delaying recruitment or postponing capital investment plans. Higher energy prices are also likely to feed through supply chains, potentially leading to higher prices for manufactured goods such as food and electronics later in the year.

The second key point is that, because energy prices have not retraced to pre-war levels, underlying risks remain. While a worst-case scenario appears to have been avoided for now, the Strait of Hormuz remains closed, and there is still no clear resolution for the US or the wider regions.

Financial markets followed suit

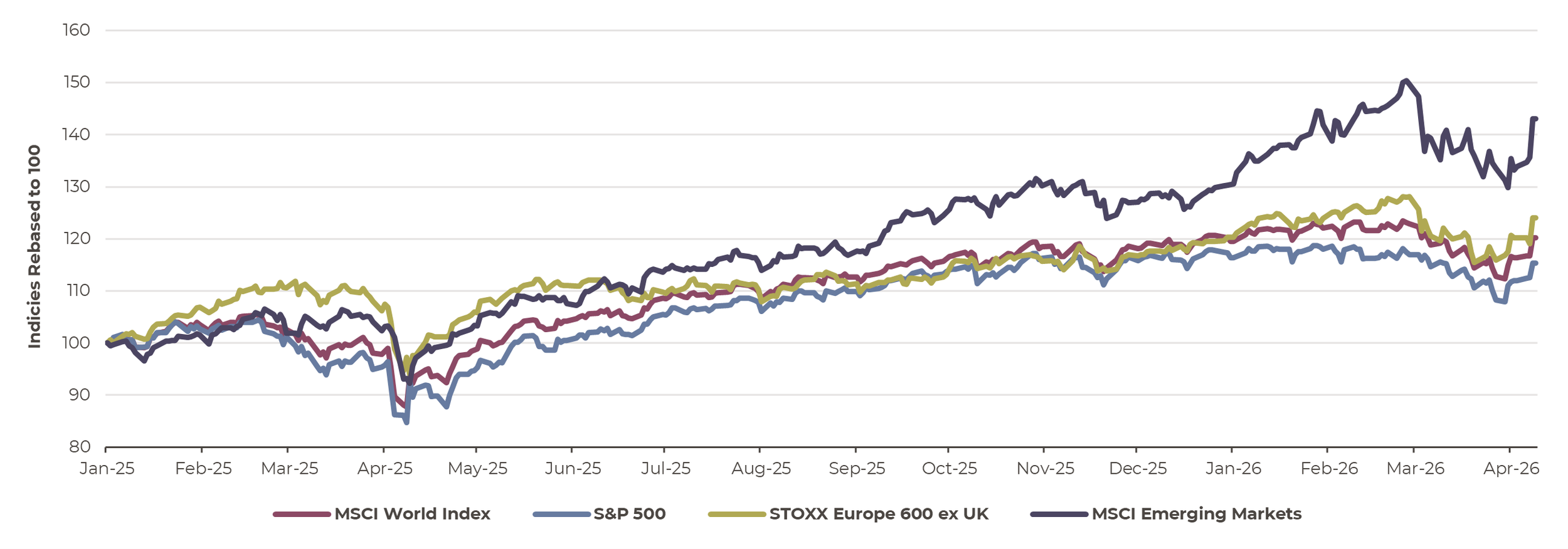

What has been particularly interesting, and perhaps somewhat disconcerting, is the financial market reaction to the US-Iran conflict. In broad terms, equity markets have remained relatively resilient since the start of the conflict, especially given the scale of the energy shock and its potential ramifications. While all equity markets responded positively to the ceasefire, emerging markets recorded the strongest rebound, which is understandable given their greater reliance on energy imports. Notably, equity prices have not yet returned to pre-war levels.

Global equity historic performance

Source: Artorius, Bloomberg

Interest rate cuts remain of the agenda

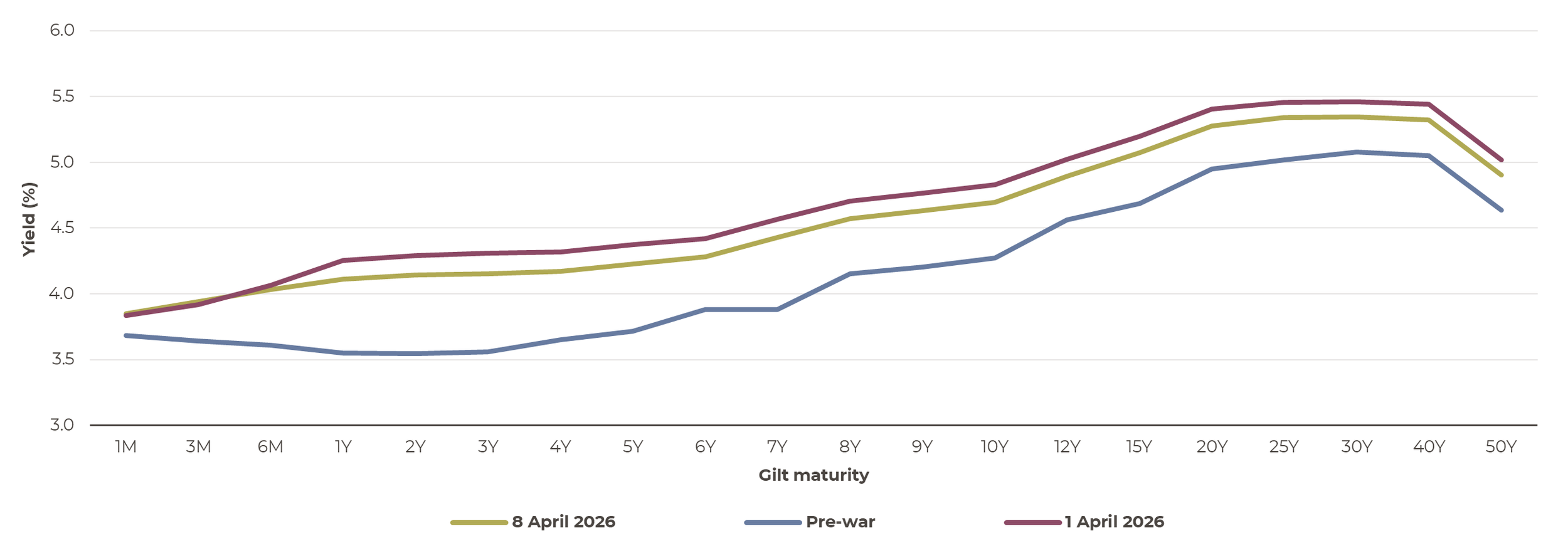

The chart below illustrates how UK gilt pricing changed from before the war, to the week prior to the ceasefire agreement, and immediately afterwards. Before the war, the gilt curve was downward sloping, with yields falling from one-month maturities before beginning to rise again between two and three years. Markets were expecting the Bank of England to cut interest rates.

The outbreak of the war, and its adverse implications for inflation, altered the shape of the yield curve. Yields rose by around 0.5% on average across the curve. The curve also shifted from its previous downward slope to an upward-sloping profile, indicating that markets were instead pricing in the likelihood of higher interest rates to counter inflationary pressures.

The ceasefire agreement provided some relief, with yields falling by around 0.11% on average across the curve. However, yields remain elevated relative to pre-war levels, and the shape of the curve still suggests that interest rate cuts are unlikely in the near term.

UK gilts yield curve as at 8th April 2026

Source: Bloomberg, Artorius

What will earnings season tell us?

The earnings season is set to begin next week, when US listed companies will report their financial performance for the first quarter of the year. While the results themselves are important, market attention is likely to be focused more closely on management commentary regarding the implications of the war for costs and demand.

Key questions will include whether inflationary pressures are beginning to increase operating costs, how long the closure of the Strait of Hormuz can be sustained before it becomes more than a temporary disruption, whether customer demand has been affected, and how companies view the outlook for the months and year ahead.

Our defensive tilt remains whilst significant uncertainty remains

The announcement of the ceasefire was welcome news on many levels. However, while both energy and financial markets responded positively, prices remain some way above pre-war levels. At the time of writing, the situation still feels somewhat precarious. The ceasefire remains in place, but the agreement is already being tested, with Israel continuing strikes in Lebanon while claiming that these actions fall outside the scope of the deal.

Time will tell whether a lasting end to the conflict can be achieved. Given that the risk of further escalation remains high, we continue to maintain a defensive tilt for the time being.

Phil Carroll

Head of Alternatives

*Any feedback provided can be anonymous

Important Information

All expressions of opinion reflect the judgment of Artorius at 10th April 2026 and are subject to change, without notice. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete; we do not accept any liability for any errors or omissions, nor for any actions taken based on its content. The value of an investment and the income from it could go down as well as up. The return at the end of the investment period is not guaranteed and you may get back less than you originally invested. Past performance is not a reliable indicator of future results. Nothing in this document is intended to be, or should be construed as, regulated advice. Artorius provides this document in good faith and for information purposes only. Reliance should not be placed on the information contained within this document when taking individual investments or strategic decisions.

Artorius Wealth Management Limited is authorised and regulated by the Financial Conduct Authority. Artorius is a trading name of Artorius Wealth Management Limited.

FP20260410001