The oil tax refunded

The oil tax refunded

Summary

Peace is good. And peace is being priced back into markets. The de-escalation of the military conflict into an uneasy ceasefire has seen equity markets recover all the losses triggered by the US-Israeli attacks on Iran.

The oil market appears to be pricing a fall back to $80 per barrel in coming months. The downward slope of the oil price curve is both unusual and is pricing in a resolution to the conflict. However, it is notable that the natural gas price curve is not downward sloping suggesting that there is less optimism about the path of natural gas prices than oil prices. And natural gas matters for the likes of the UK, as this is a key determinant of the energy price paid by UK households and industry. This is something the government will be nervous about in coming months.

Oil prices remain higher than they were before the conflict started and bond yields reflect the likelihood of higher inflation. Higher bond yields have resulted in higher mortgage rates and in both the US and the UK the housing market appears to have stalled.

In the US, tax refunds are running 11% higher than in 2025. According to research from Bank of America, the higher level of tax refunds reflects the ‘benefits’ of President Trumps ‘One Big Beautiful Act’ and will more than compensate for the impact of higher oil prices for at least six months for the average US household. This may shelter the US from the impact of high oil prices on US consumer spending. Other countries may not be so sheltered.

Flux

At the point of typing, the war has de-escalated into a fragile peace, albeit with the Strait of Hormuz being blocked by both Iran and the US. The oil price has fluctuated with every twist of the conflict. The de-escalation and announcement of a ceasefire resulted in a welcome fall from $115 to $95 per barrel on the 7th April. Following US-Iran talks held in Pakistan, oil prices have risen back over $100 per barrel.

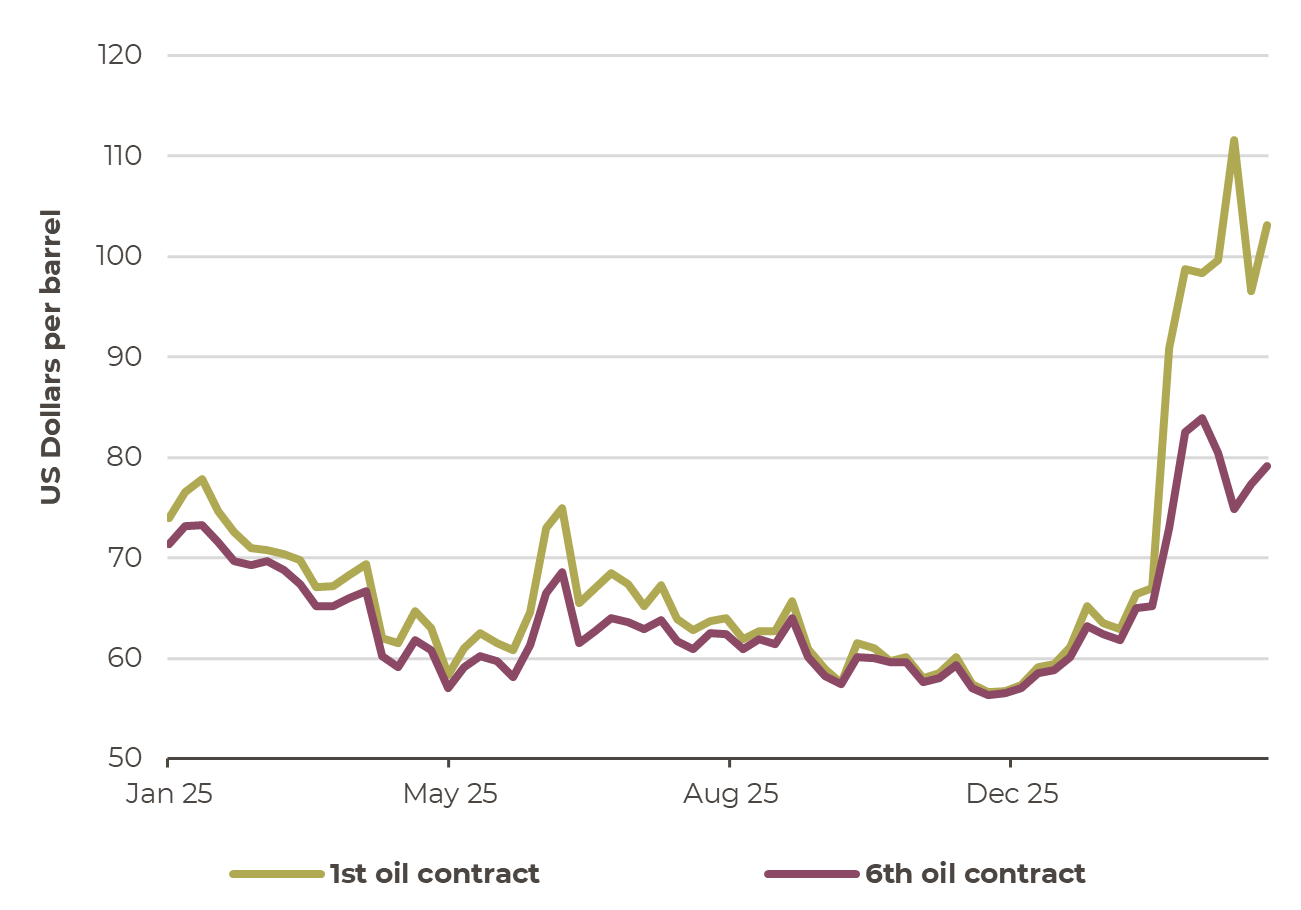

The chart on the right shows the oil price both at the first month contract, which is the oil price ‘most’ commentators will be referring to, but also the sixth month contract, i.e. the price at which the market is willing to pay for oil in six months time, so effectively what the market expects the then current oil price will be in six months’ time. Contracts allow companies that use oil to pre-purchase their oil for months ahead and know what price they will eventually have to pay for delivery. In January the sixth month contract will be the expected oil price in June. Currently the sixth month contract relates to the price of oil expected in October.

Normally, the first month and sixth month contract price are very similar with the average difference of $3.50 between contracts over the past five years. The US-Israeli attacks on Iran at the end of February saw the 1st month oil price jump up sharply from around $70 to $100 per barrel. The price of the sixth month contract ‘only’ rose to $80. At the peak there was a $35 per barrel difference between first and sixth month oil contracts.

Even after the immediate escalation of the Russian invasion of Ukraine in 2022, the gap only reached $15, and quickly normalised as oil prices gradually fell through 2022.

Oil prices: 1st and 6th month contracts. The gap between ‘near-term’ oil prices and ‘future’ oil prices reflects a belief (hope) that the conflict and disruption to the Strait of Hormuz will not last too long.

Source: Bloomberg, Artorius

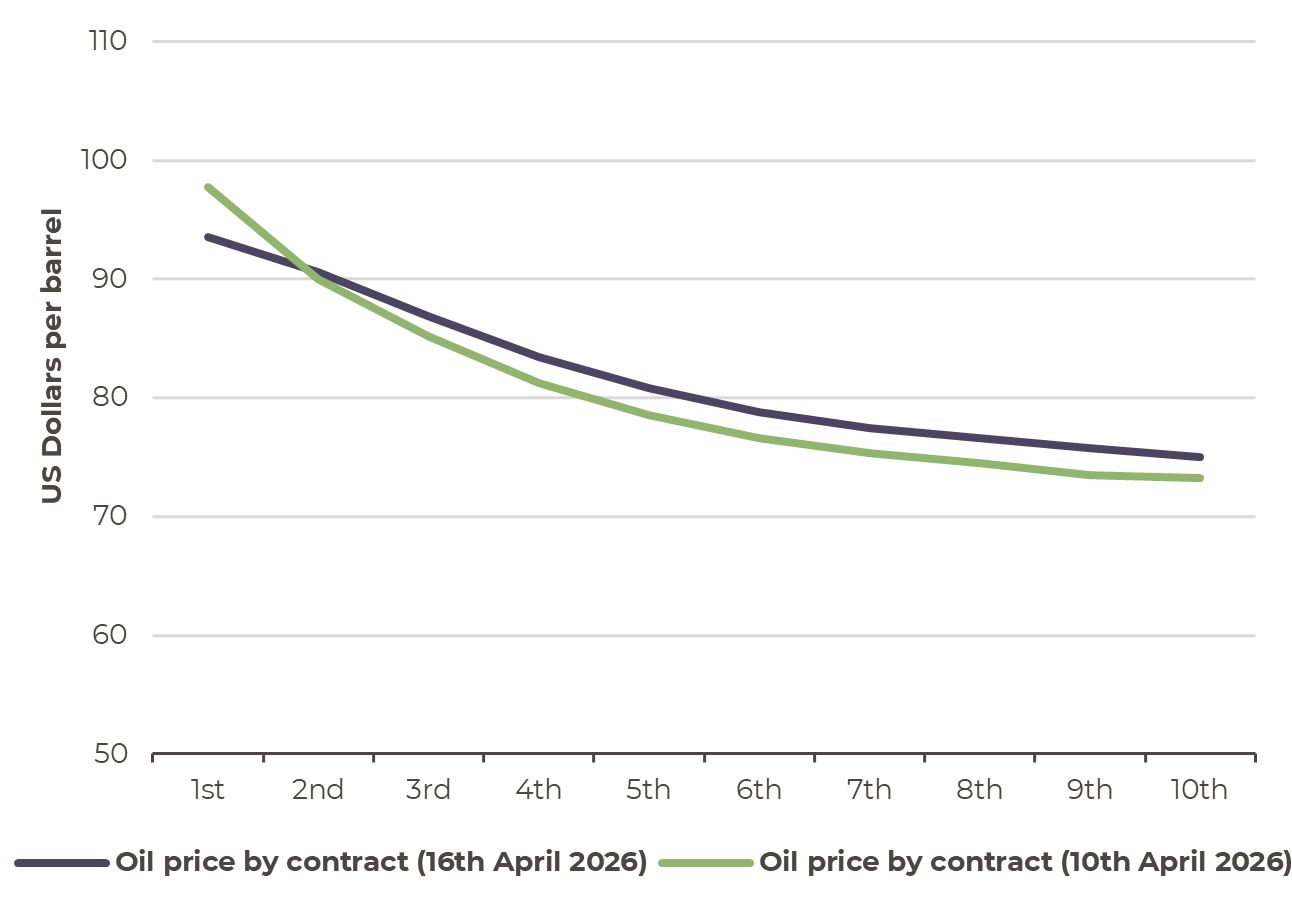

This downward sloping oil price curve is unusual, and suggests that the market believes that the energy price shock will be relatively short-lasting. The chart below shows the oil price curve after the ceasefire announcement on 10th April and also as at the 15th April. The change of the oil price at the first month (current price) over the past few days isn’t impacting the oil price in future months.

Whilst the oil price is over $90 per barrel, the downward sloping curve shows that markets expect oil prices to fall in coming months. Of note, the ceasefire and news of further negotiations over recent days has reduced the oil price in the near term, but has had limited impact on the oil price for future months.

The oil price has a downward sloping curve reflecting an expectation of falling oil prices in coming months

Source: Bloomberg, Artorius

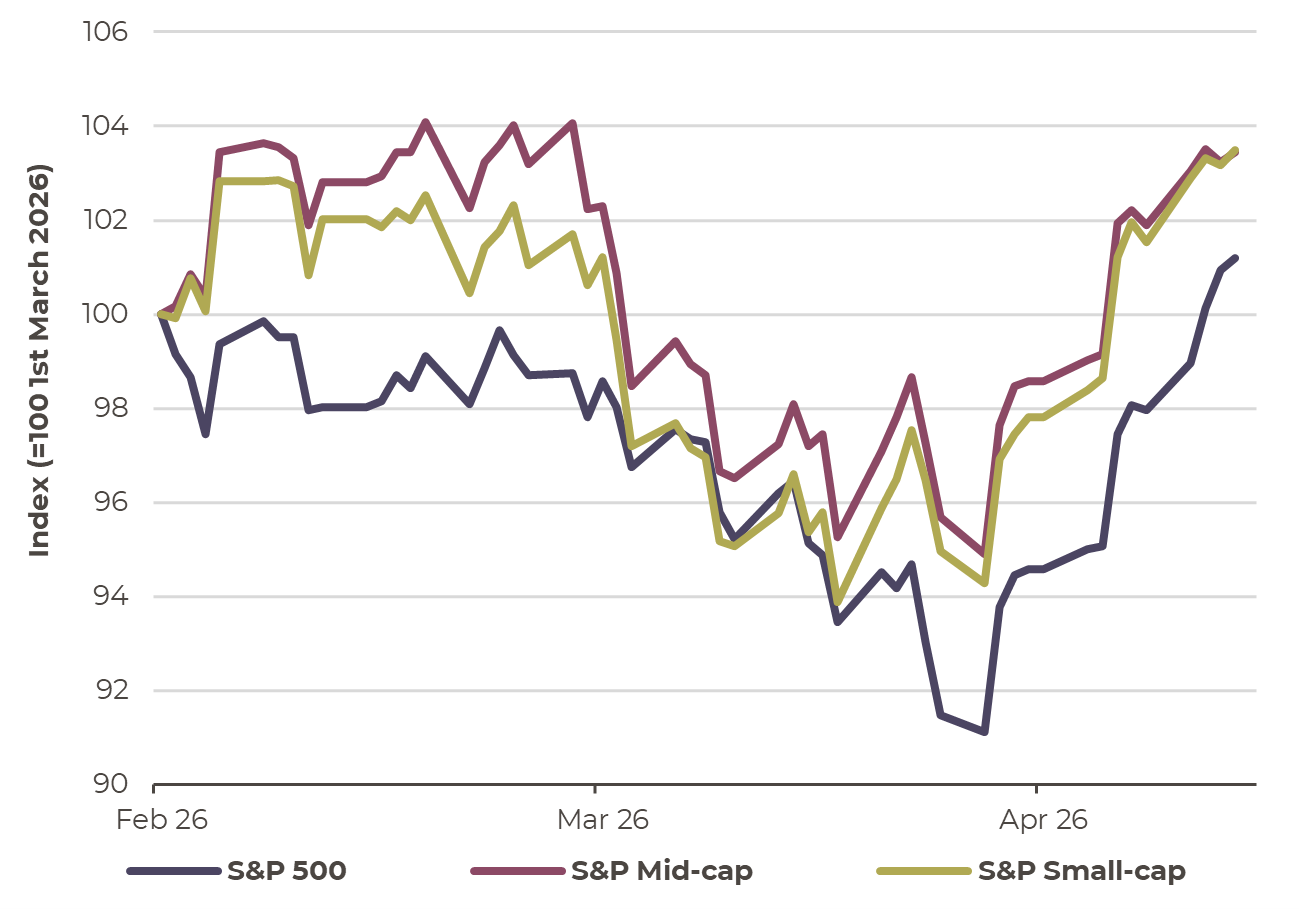

The economic impact of the oil price shock maybe be more dependent on the oil price over coming months rather than the here and now. The here and now price has been more volatile than the longer-term oil price. This may explain why the equity markets seem sanguine despite oil price volatility. Whilst equity markets were jolted by the commencement of military action, the recovery in equity prices over past two weeks has been robust. Even in the economically sensitive parts of the market which dominate mid and small cap equity indices, markets have largely recovered the ‘war’ losses. So, despite the higher oil prices and heightened inflation risk, investors remain positive on equities.

US equity markets have recovered their war losses

Source: Bloomberg, Artorius

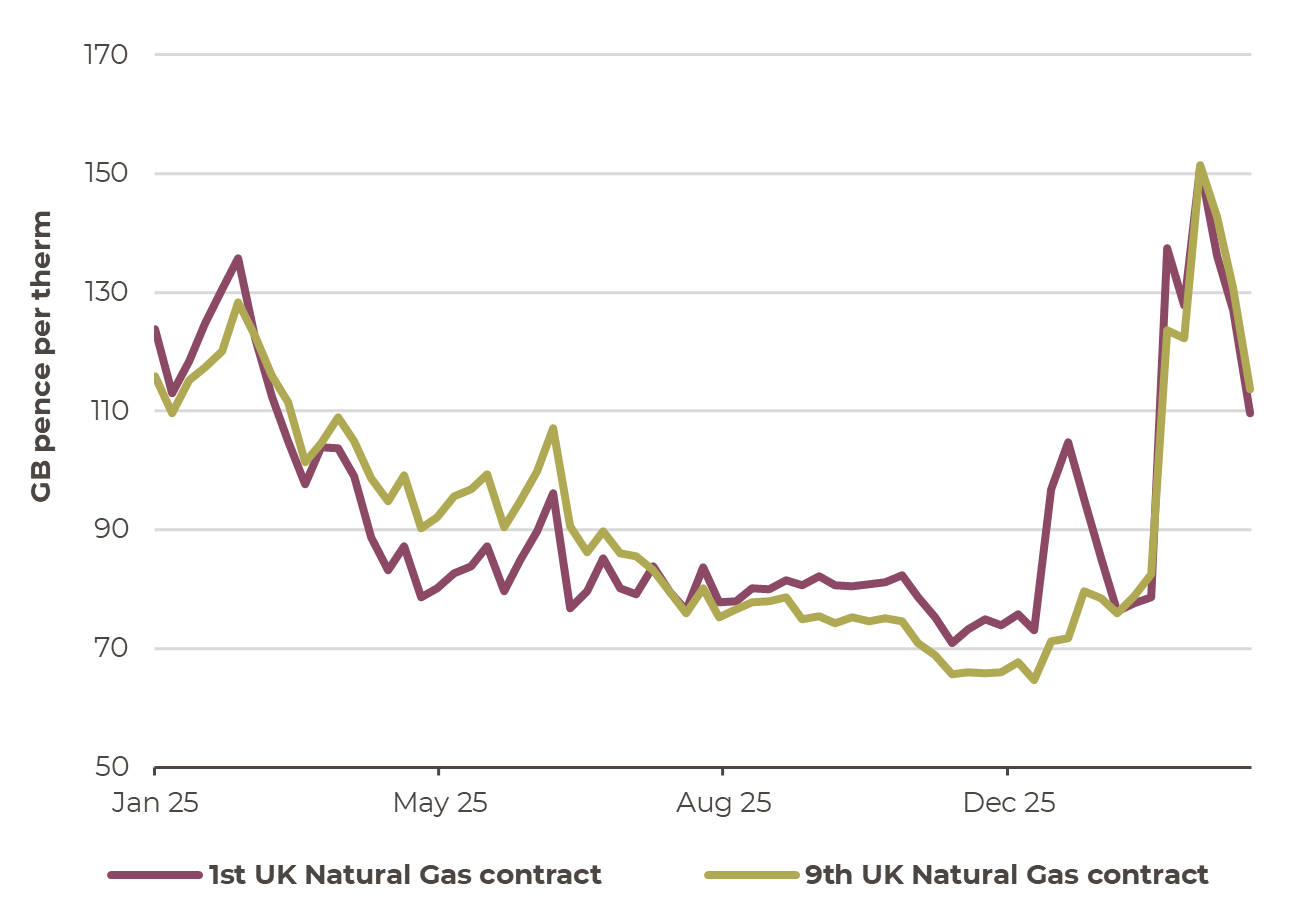

Just because oil is discounting a better outlook for lower oil prices in six months’ time, it isn’t the case for UK natural gas contracts. The price of gas jumped from 80p per therm to 150p per therm through the first three weeks of March. Whilst the price has eased back to £1.10 per therm the contract for the sixth month (currently the January 2027 contract) has tracked the price change. Oddly, while the market is expecting the oil price to fall in coming months, it does not have the same view for natural gas prices. The ‘stickiness’ of natural gas prices may reflect the loss of Qatar’s Ras Laffan facility, the world’s largest Liquefied Natural Gas (LNG) plant, and it highlights that not all energy supply is equal.

The natural gas price is important in determining the cost of energy for UK industry and households. Whilst the price rise in 2026 is less than in 2022, following the Russian invasion of Ukraine, it can be expected that higher prices will impact consumer sentiment and spending.

UK natural gas prices remain elevated, and do not price in a fall in future energy costs (unlike the expectations over the oil price)

Source: Bloomberg, Artorius

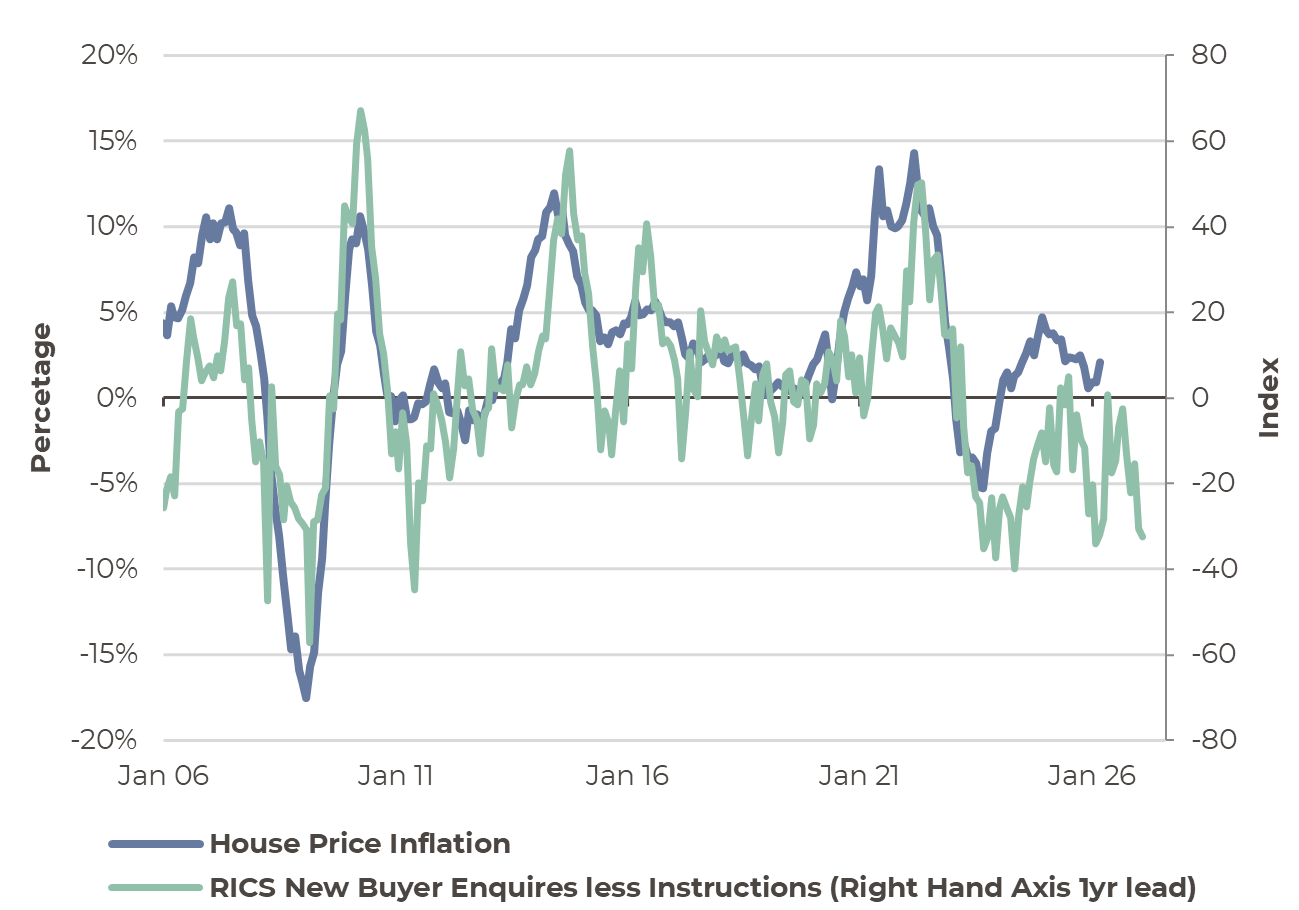

Interest rates and the UK housing market

Bond markets have yet to make the same round trip as equities. Bond yields remain higher than they were at the end of February. In the UK, 2-year gilt yields are 0.79% higher than they were before the start of the war, albeit 0.30% lower than at the peak in mid-March. However, the two year yield influences mortgage rates, and higher mortgage rates in the UK have already cooled the UK housing market.

The Royal Institute of Chartered Surveyors (RICS) survey their membership each month to produce an insight into the housing market. The March 2026 RICS UK Residential Market Survey results show that the macro-related fallout linked to the conflict in the Middle East is taking its toll on both current activity and forward-looking sentiment. With intensifying inflationary pressures pushing borrowing costs higher, buyer demand has weakened, while near-term expectations have turned significantly more cautious over the month. At the headline level, the new buyer enquiries net balance slipped to the weakest return for the survey’s measure of buyer demand (in net balance terms) since August 2023, with most parts of the UK seeing a noticeable deterioration over the past couple of months.

On the back of this, the volume of agreed sales has also been adversely affected. The aggregate net balance was the softest reading since the summer of 2023. Looking ahead, near term sales expectations turned significantly more pessimistic, with the latest net balance dropping to below zero, indicating that respondents now anticipate a further contraction in sales activity over the coming months.

UK housing market: The RICS survey suggests a softening in the housing market and fall in house prices in the coming year

Source: Bloomberg, Artorius

Trump’s tax refunds pay for oil?

The US housing market is seeing a similar dip as higher mortgage interest rates impact activity. A recent survey shows that US consumer confidence has reached an all-time low. With this data it is easy to be drawn to pessimistic conclusions around the US consumer.

However, there is a bright spot. The US consumer is benefitting from tax refunds (due to President Trump’s One Big Beautiful Act) that will compensate for the higher oil prices.

Data from the US Inland Revenue Service (IRS) shows that that the total amount in tax refunds has risen by 14.5% in overall US Dollar terms and that the average amount has risen by 11% compared to the same time in 2025. These US Dollars are having an impact in driving US consumer spending but don’t appear to be reflected in the depressed consumer sentiment.

This is crucial because it may offset the impact of higher oil prices (particularly through higher gasoline (petrol) prices) on US consumers. While the duration of the conflict is highly uncertain – as is the impact on oil prices – if higher gasoline prices are sustained for a prolonged period all households will be impacted, but lower-income families are most exposed. According to Bank of America data, US household monthly gasoline spending for low-income households was equivalent to around 8-10% of their total card spending throughout most of the past eight years, roughly twice that of those with higher incomes. The tax refunds could offset nearly 5 months of higher gasoline price for low-income households and over 10 months for high incomes.

Recent history has been good

Every quarter, US companies provide an update on their profits and prospects. The Q1 reporting season started recently, and over the next few weeks we will get a corporate’s eye view on the outlook and how the war is impacting spending and investment intentions. For the moment, analysts have not seen fit to change the outlook for profits in 2026 and 2027. The upbeat view held at the start of 2026 remains undimmed.

Conclusion

Peace is good. And peace is being priced back into markets. The de-escalation of the military conflict into an uneasy ceasefire has seen equity markets recover all the losses triggered by the US-Israeli attacks on Iran.

The oil market appears to be pricing a fall back to $80 per barrel in coming months. The downward slope of the oil price curve is both unusual and is pricing in a resolution to the conflict. However, it is notable that the natural gas price curve is not downward sloping suggesting that the there is less optimism about the path of natural gas prices than oil prices. And natural gas matters for the likes of the UK, as this is a key determinant of the energy price paid by UK households and industry. This is something that the government will be nervous about in coming months.

Oil prices remain higher than they were before the conflict started and bond yields reflect the likelihood of higher inflation. Higher bond yields have resulted in higher mortgage rates and in both the US and the UK the housing market appears to have stalled.

In the US, tax refunds are running 11% higher than in 2025. According to research from Bank of America, the higher level of tax refunds reflects the ‘benefits’ of President Trumps ‘One Big Beautiful Act’ and will more than compensate for the impact of higher oil prices for at least six months for the average US household. This may shelter the US from the impact of high oil prices on US consumer spending. Other countries may not be so sheltered.

*Any feedback provided can be anonymous

Important Information

Artorius provides this document in good faith and for information purposes only. All expressions of opinion reflect the judgment of Artorius at 17th April 2026 and are subject to change, without notice. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete; we do not accept any liability for any errors or omissions, nor for any actions taken based on its content.

The value of an investment and the income from it could go down as well as up. The return at the end of the investment period is not guaranteed and you may get back less than you originally invested. Past performance is not a reliable indicator of future results.

Nothing in this document is intended to be, or should be construed as, regulated advice. Reliance should not be placed on the information contained within this document when taking individual investment or strategic decisions.

Any advisory services we provide will be subject to a formal Engagement Letter signed by both parties. Any Investment Management services we provide will be subject to a formal Investment Management Agreement, which will include an agreed mandate.

Artorius Wealth Management Limited is authorised and regulated by the Financial Conduct Authority. Artorius is a trading name of Artorius Wealth Management Limited.

FP20260417001